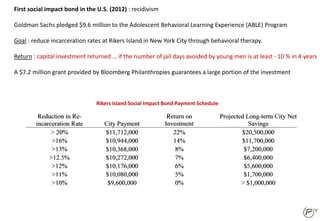

Download as PDF, PPTX

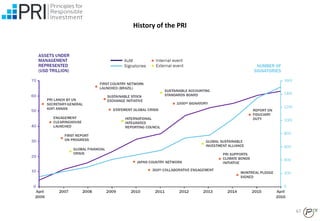

![38

Handicap of SRI

3) Fiduciary duty

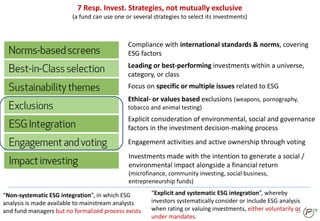

• A report from the law firm Freshfields Bruckhaus Deringer in 2005 for the asset

management stream of UNEPFI concluded :

« Conventional investment analysis focuses on value, in the sens of financial performance [...]

the links between ESG factors and financial performance are increasingly being recognised.

On that basis, integrating ESG considerations into an investment analysis so as to more

reliably predict financial performance is clearly permissible and is arguably required in all

jurisdictions ».](https://image.slidesharecdn.com/sri1-xavierheude-140330023918-phpapp02/85/Responsible-Investing-part-I-what-does-really-make-a-difference-38-320.jpg)

Le document aborde l'investissement responsable et l'impact des critères environnementaux, sociaux et de gouvernance (ESG) sur les décisions d'investissement. Il souligne l'intérêt croissant pour les investissements durables, notamment parmi les femmes, les entrepreneurs et la jeune génération, tout en notant un manque de critères clairs pour définir les pratiques durables. En outre, il évoque les efforts de normalisation et l'appel à l'intégration des ESG dans l'analyse financière afin de mieux évaluer les performances des entreprises et de respecter les normes de responsabilité sociale.