Download to read offline

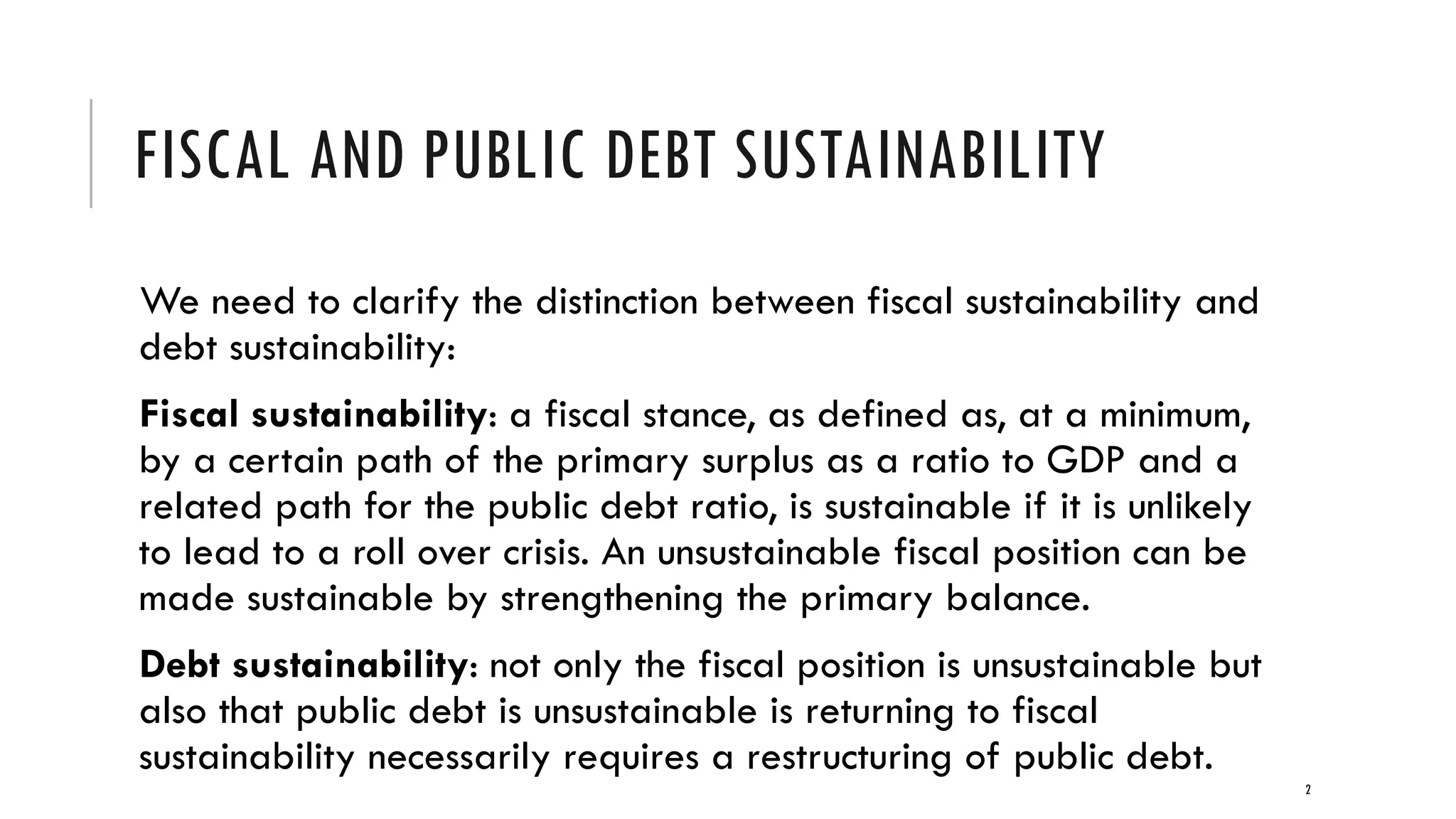

1) The document discusses the distinction between fiscal sustainability and debt sustainability. Fiscal sustainability refers to a fiscal stance that is unlikely to lead to a roll over crisis, while debt sustainability means public debt itself is unsustainable even after returning to fiscal sustainability, requiring debt restructuring. 2) It compares the relative costs of adjusting the primary balance orthodoxly versus restructuring debt. Adjusting the primary balance risks larger output costs from demand effects, while debt restructuring risks a default tax, wealth loss for domestic debt holders, and uncertainty about the sufficiency of restructuring and return to markets. 3) Restructuring debt also risks reputational costs that depend on the amount of net present value loss imposed on debt