Download as PDF, PPTX

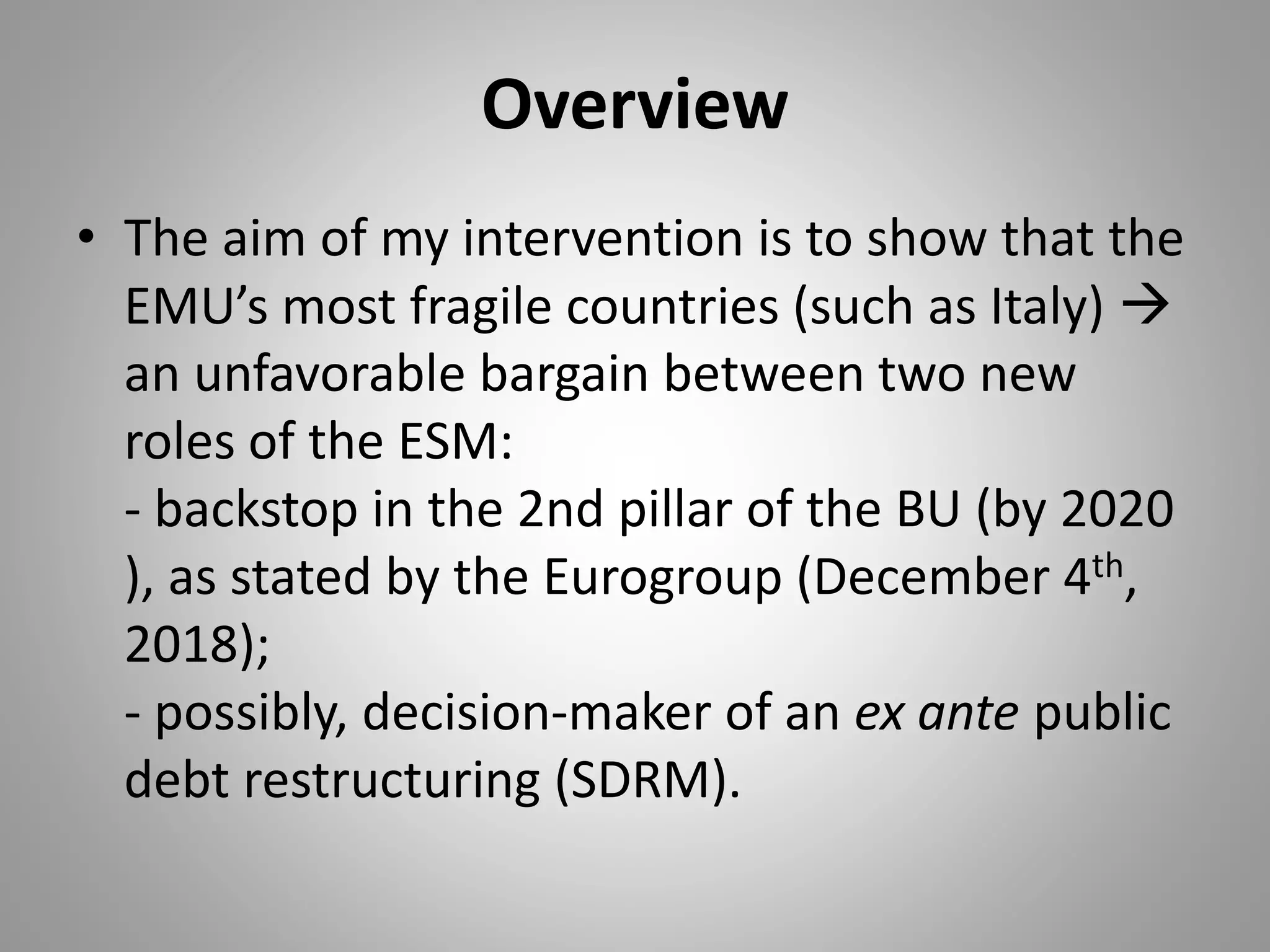

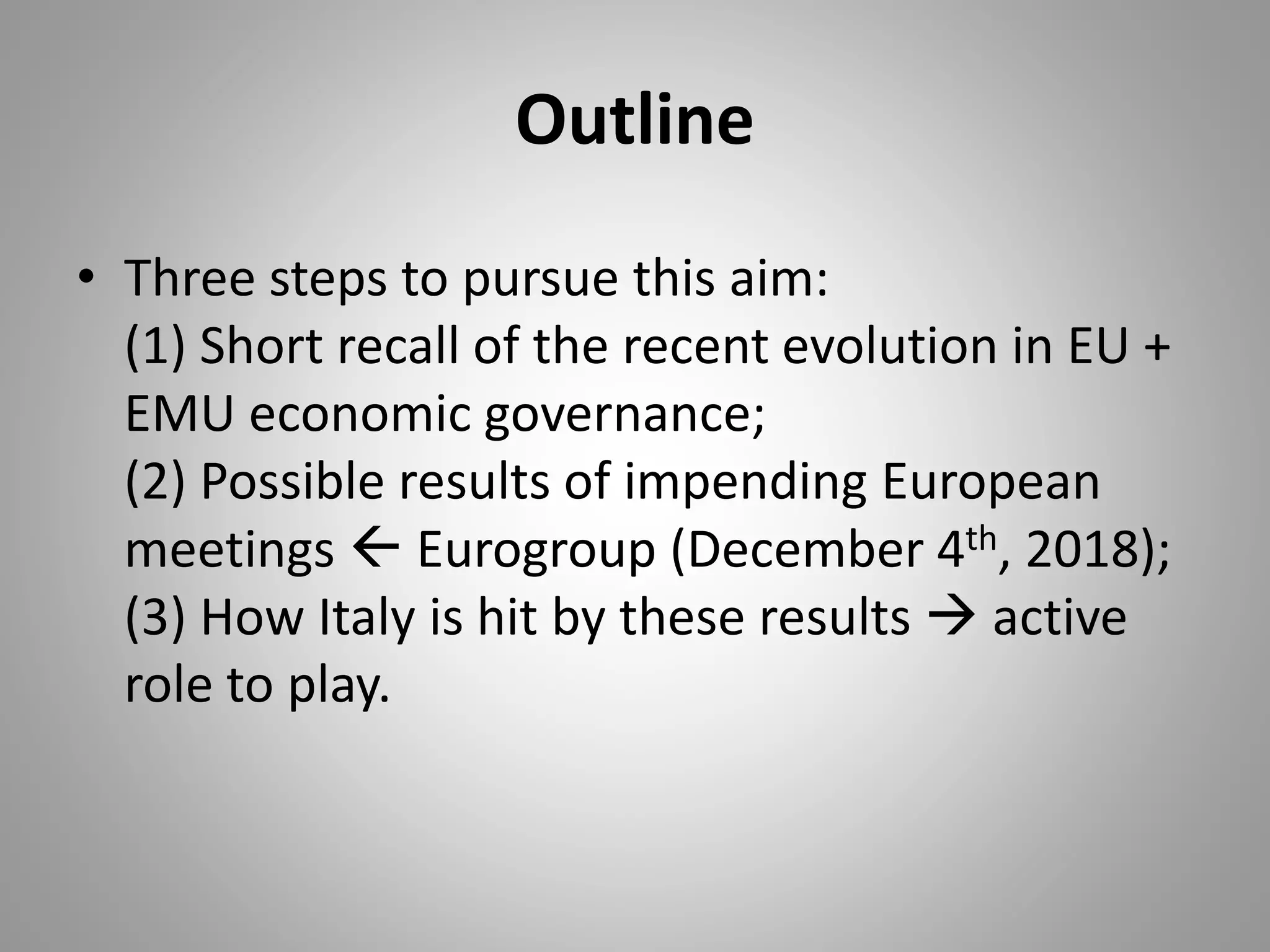

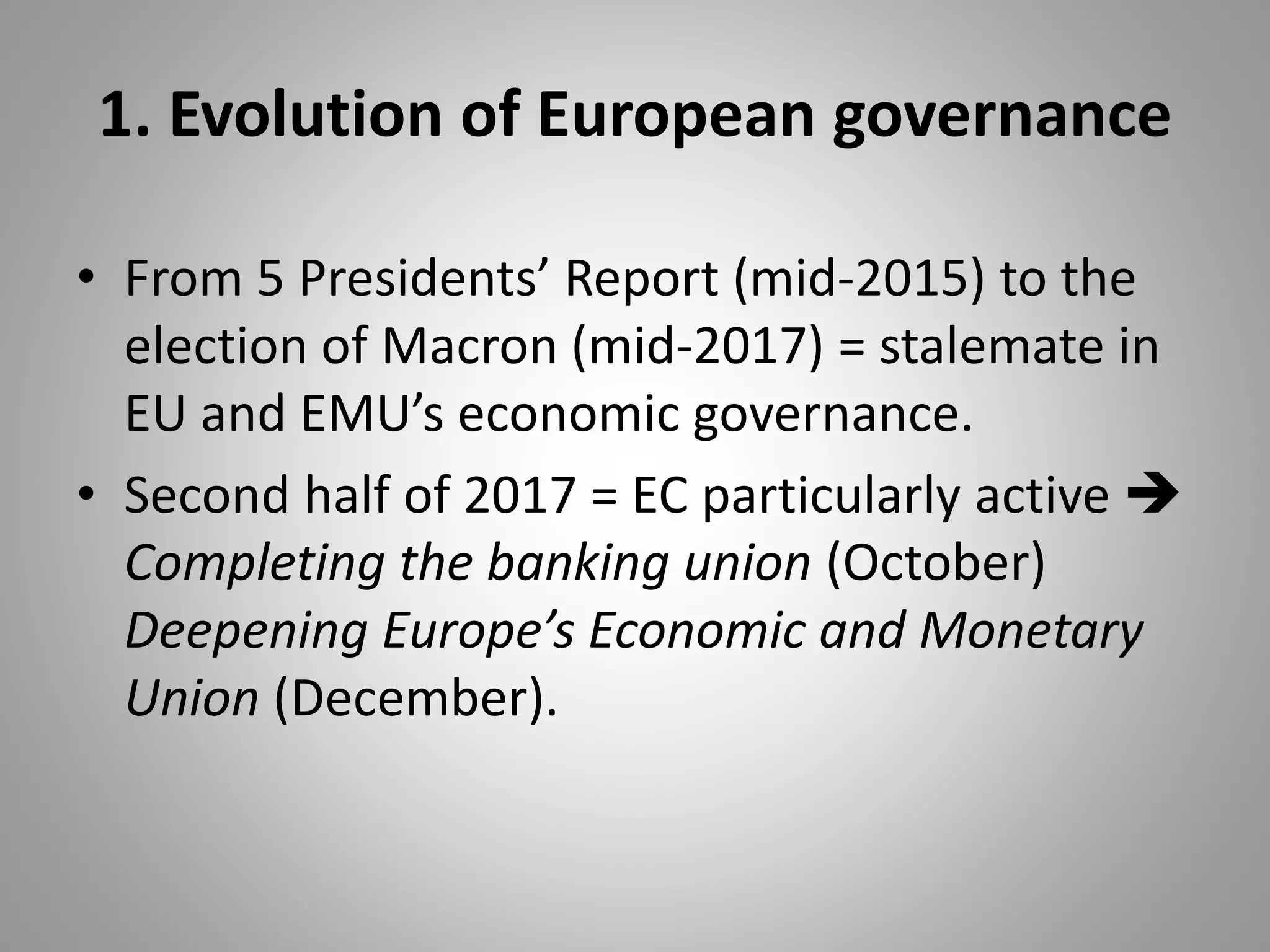

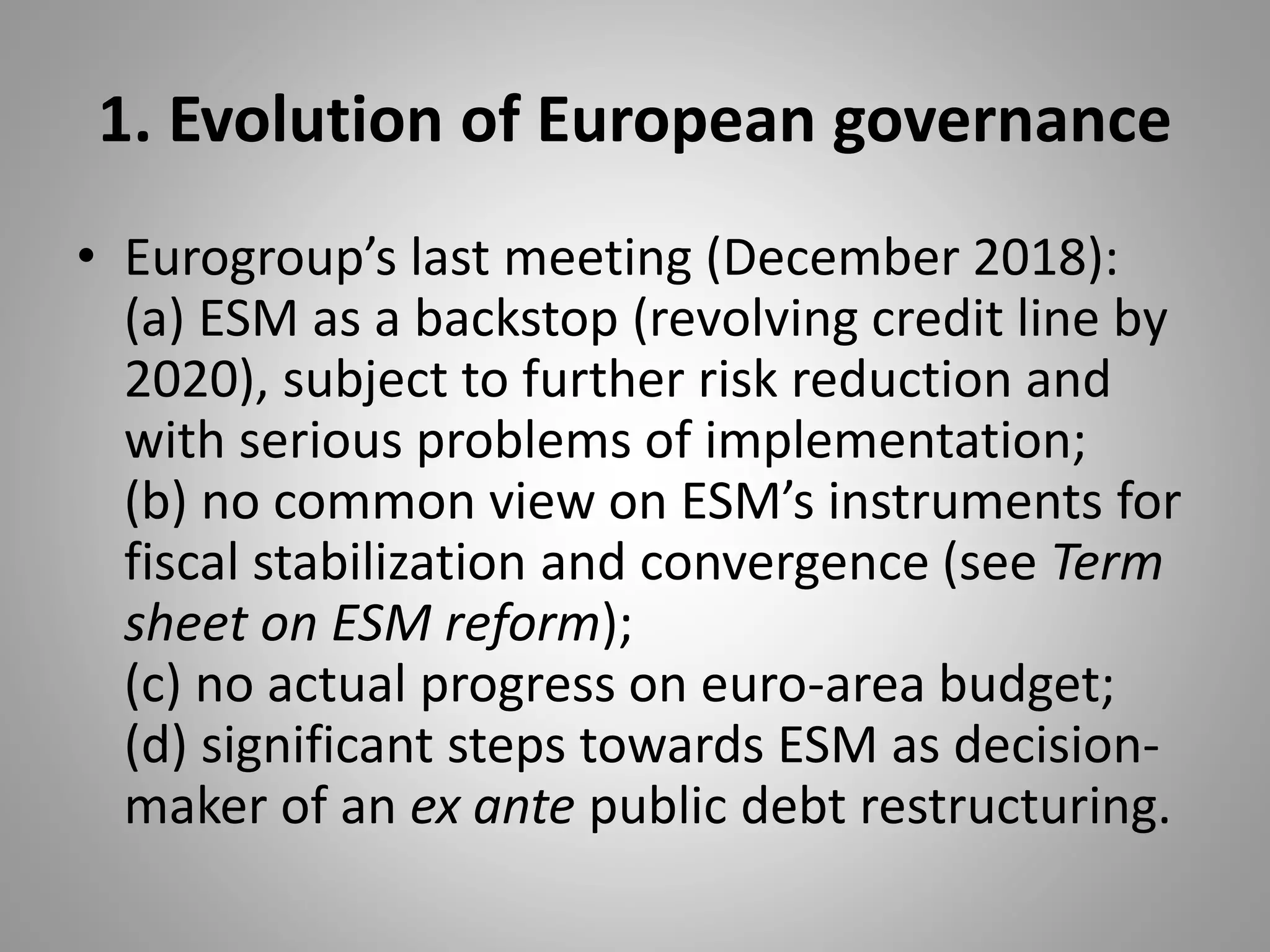

The document discusses the challenges and developments in managing sovereign debt crises within the European Monetary Union (EMU), particularly focusing on Italy's situation. It outlines recent changes in EU economic governance, the role of the European Stability Mechanism (ESM), and the implications of ex ante versus ex post debt restructuring. The author recommends that Italy should comply with European rules, maintaining its reputation while advocating for ex post debt restructuring to avoid macroeconomic instability.