What is aBudget?

A budget is a financial plan that outlines expected income and expenses over a

specific period, typically a month. It serves as a guide for managing financial

resources effectively and achieving personal financial goals. Budgets are

essential in personal finance as they help individuals monitor their spending,

ensure they live within their means, and prepare for both anticipated and

unforeseen expenses. Understanding the basics of budgeting is crucial for

establishing a strong financial foundation.

5.

Components of aBudget

Income

Income includes all sources of money coming in, such as

salary, wages, dividends, and any other financial

benefits.

Expenses

Expenses are costs to generate revenue and maintain

operations. They include fixed costs like rent and

variable costs like utilities. Managing expenses is crucial

for financial health.

Savings

Savings is the portion of income set aside for future use,

emergencies, or specific financial goals.

Financial Goals

These are objectives that guide budgeting, such as

saving for a house or retirement.

Importance of

Financial Goals

Settingfinancial goals is a cornerstone of effective

budgeting and financial planning. Financial goals

provide a roadmap for managing money, prioritizing

spending, and saving for the future. They help

individuals focus on what truly matters and make

informed financial decisions that align with their life

aspirations.

8.

SMART Goals

Specific

Goals shouldbe clear and precise, detailing exactly what you

want to achieve. Specificity eliminates ambiguity and provides

direction, making it easier to focus efforts.

Measurable

A goal must be quantifiable so that progress can be tracked.

Measurable goals help to identify milestones and motivate

continued effort.

Achievable

Goals should be realistic and attainable given the available

resources and constraints. This ensures that goals are

challenging yet possible.

Relevant

A goal must align with broader life objectives and values,

ensuring that it is worthwhile and meaningful. Relevance

helps maintain focus on priorities.

Time-bound

Setting a deadline for achieving the goal instills urgency and

helps prioritize tasks, ensuring that efforts are consistently

directed towards the goal.

9.

Examples Of FinancialGoals

Saving for a Vacation

Setting aside a specific amount of money each month to

fund a planned vacation in the near future. This goal can

be achieved by budgeting and reducing discretionary

spending.

Building an Emergency Fund

Accumulating savings to cover 3-6 months of living

expenses for unforeseen circumstances. This involves

prioritizing savings in the budget to ensure financial

security.

Paying off Student Loans

Allocating extra funds towards repaying student loans

faster. This goal requires disciplined budgeting and may

involve cutting back on non-essential expenditures.

Retirement Planning

Contributing regularly to retirement accounts to build a

sufficient nest egg. It involves understanding retirement

needs and adjusting budget allocations accordingly.

Income Tracking Tools

IdentifyIncome Sources

It's essential to recognize all income streams, whether it's salary, freelance work, dividends, or

rental income.

Documentation Methods

Accurate documentation of income is crucial. Utilize pay stubs, invoices, and bank statements

to track and verify income regularly.

Income Track Tools

Leverage digital tools and software that automate income tracking, offering convenience and

accuracy. Tools such as financial management platforms can streamline this process.

12.

Categorizing Expenses

Fixed Expenses

Theseare recurring, predictable costs such as rent,

mortgage, and insurance.

Discretionary Expenses

Non-essential expenses like dining out and luxury items.

Variable Expenses

Costs that fluctuate monthly, like groceries and

entertainment.

Savings and Investments

Allocate funds towards savings and investments.

13.

Tools for Tracking

Inthe modern age, numerous tools are available to help track income and

expenses, making financial management more accessible and efficient.

Some applications are popular for personal finance management, offering

features like budgeting, expense categorization, and income tracking. These

apps often come with user-friendly interfaces and are compatible with

various devices, allowing users to access their financial data anywhere,

anytime.

Budget Formats

01

Envelope System

Acash-based budgeting method where money is divided

into envelopes labeled by category.

02

Spreadsheets

Spreadsheets are versatile tools that offer customization

for personal budgeting.

03

Zero-Based Budgeting

This method requires assigning every dollar a specific

purpose, ensuring that income minus expenses equals zero.

04

Budgeting apps

Some apps offer structured, automated budgeting

solutions.

16.

Balancing Your Budget

Tobalance a budget, keep expenses below income to achieve financial goals.

Prioritize essentials like housing and utilities over non-essentials. Follow the

50/30/20 rule: allocate 50% for needs, 30% for wants, and 20% for savings.

Save monthly for unexpected costs and revise your budget as income or

goals change. Utilize real-time tracking tools.

17.

Personalizing Your Budget

01

Assessingfinancial goals

Start by identifying both short-term and long-term

financial goals. 02

Adapt income to changes

Flexibility is key in budgeting, especially when income

fluctuates.

03

Understanding spending habits

Analyze past spending patterns to understand habits

and identify areas for improvement.

04

Save for emergencies

Ensure a portion of income is directed towards an

emergency fund.

Reviewing Your Budget

Budgetreviews enhance financial stability and align goals. Planners

recommend monthly or quarterly assessments of income and expenses to

improve spending habits. This approach helps adapt to income changes,

prevents overspending, increases savings, and supports long-term

objectives. Budgeting apps provide real-time insights for trend analysis and

adjustments.

20.

Managing Unexpected Expenses

Buildingan Emergency Fund

Establish a dedicated savings account to cover

unexpected costs like medical bills or car repairs.

Insurance Coverage

Ensure adequate insurance coverage for health,

property, and other liabilities.

Expense Prioritization

Identify essential expenses and prioritize them in your

budget.

Contingency Planning

Develop a plan to reallocate funds in case of

emergencies.

21.

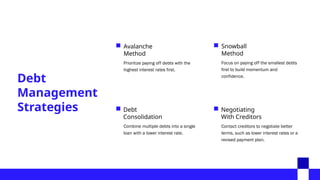

Debt

Management

Strategies

Avalanche

Method

Prioritize paying offdebts with the

highest interest rates first.

Snowball

Method

Focus on paying off the smallest debts

first to build momentum and

confidence.

Debt

Consolidation

Combine multiple debts into a single

loan with a lower interest rate.

Negotiating

With Creditors

Contact creditors to negotiate better

terms, such as lower interest rates or a

revised payment plan.

![Comparison_microscope_poster[1] ranjeet.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/comparisonmicroscopeposter1ranjeet-250404204545-4bb88d2f-thumbnail.jpg?width=640&height=640&fit=bounds)

![SecurityBoat_Service_Pitch_Deck[24158].pdf](https://cdn.slidesharecdn.com/ss_thumbnails/securityboatservicepitchdeck24158-260121113056-452683e3-thumbnail.jpg?width=640&height=640&fit=bounds)