Download as PDF, PPTX

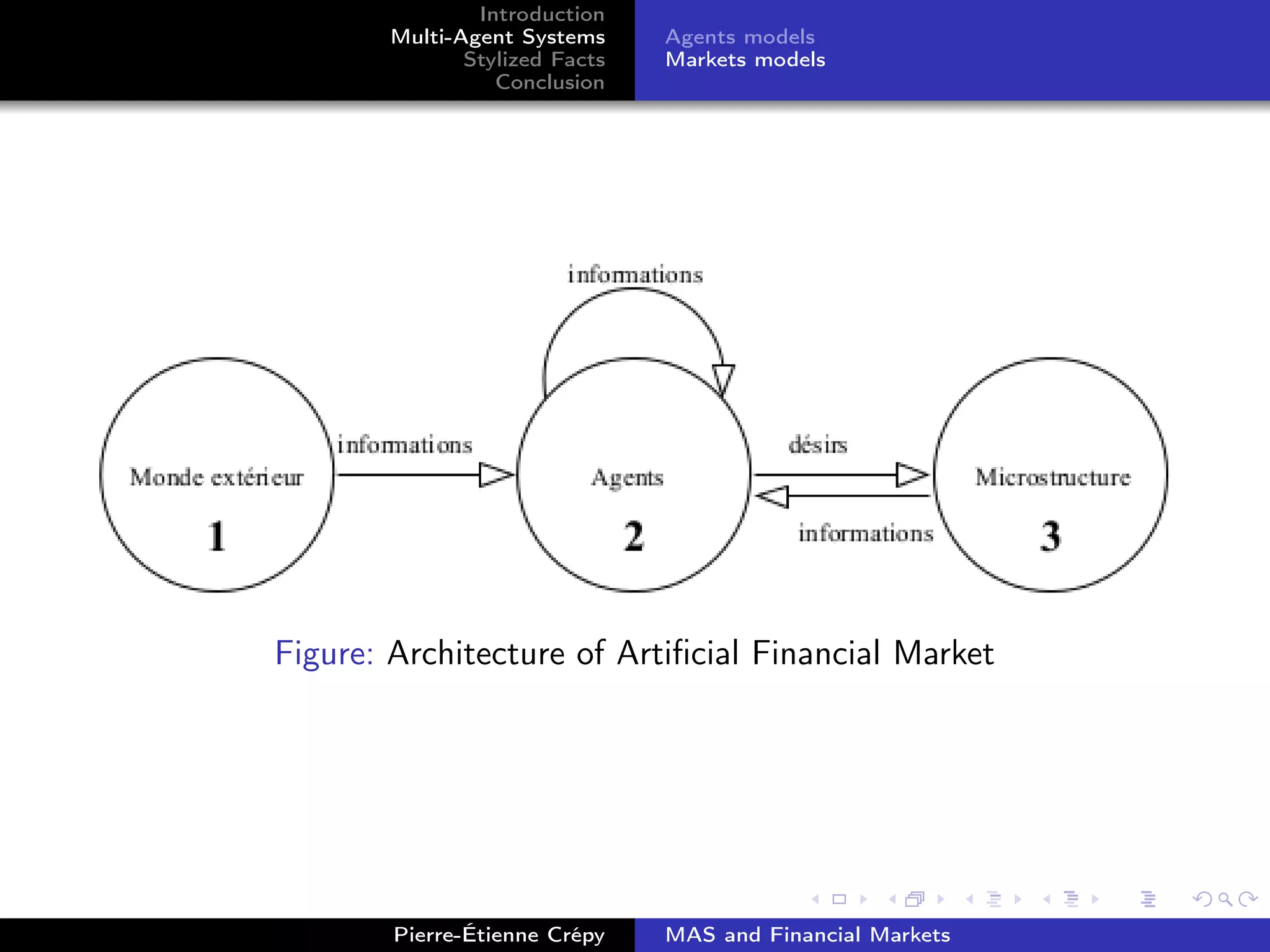

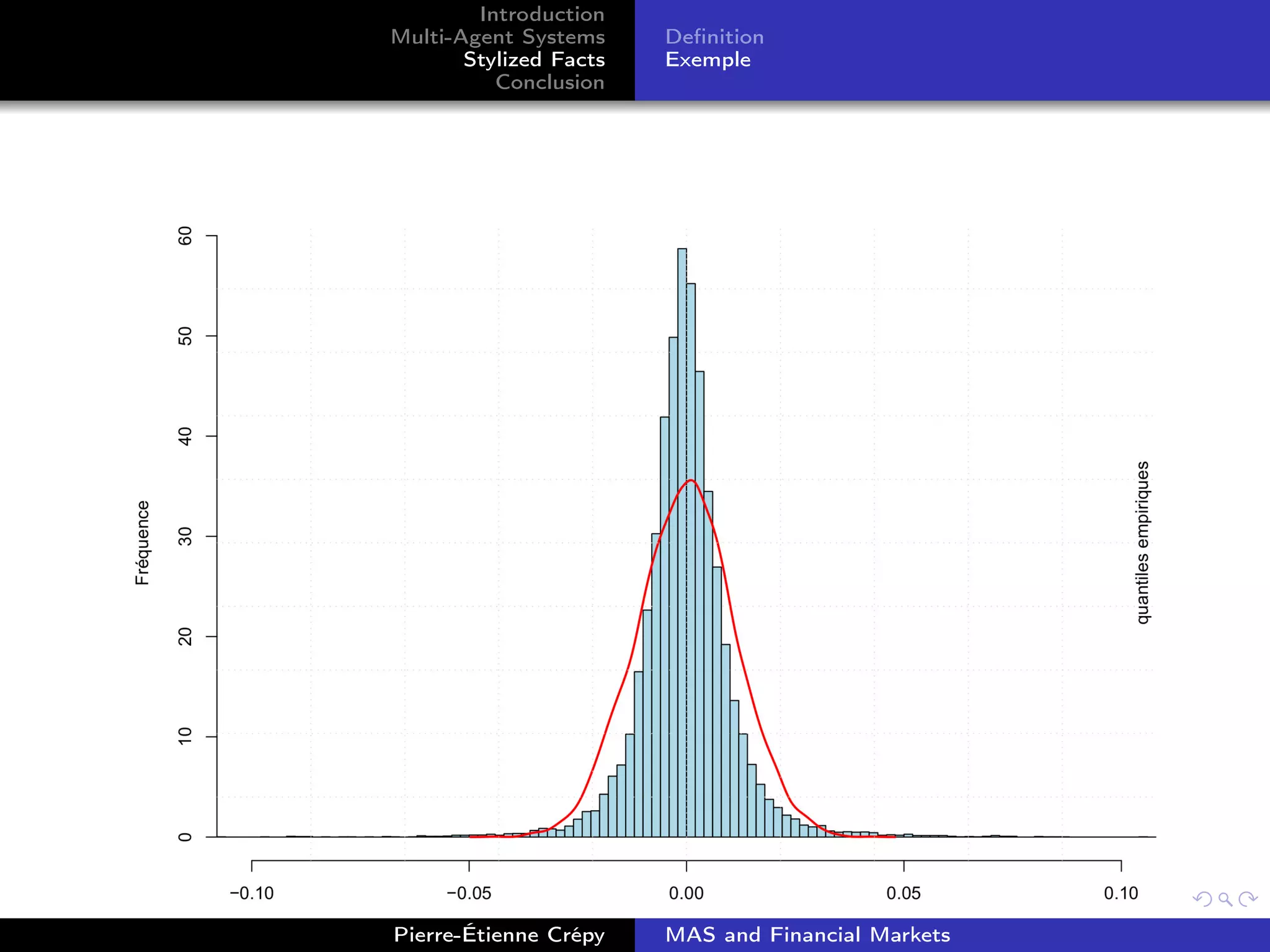

This document discusses using multi-agent systems to model financial markets. It introduces financial markets and exchanges as well as different types of agent-based models that have been used, including zero-intelligence traders and cognitive or social agents. It also discusses stylized facts that are observable in real markets and how agent-based models can help explain these phenomena through massive simulations that account for market microstructure and the interactions between agents and information. The conclusion suggests that while microstructure is important for reproducing stylized facts, other factors are also likely at play.