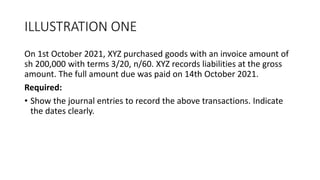

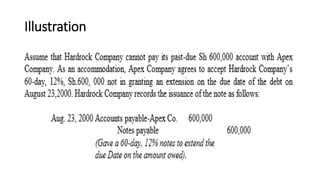

Short term liabilities are obligations that are expected to be paid within one year or the normal operating cycle. They include accounts payable, notes payable, accrued expenses, and contingent liabilities that are probable and can be reasonably estimated. Current liabilities arise from past transactions and are obligations of the company. Examples provided show accounting entries for accounts payable and interest bearing notes. Contingent liabilities may require accrual, disclosure, or no reporting depending on the probability and ability to estimate the potential loss. Product warranties and guarantees are also considered contingent liabilities.