Download to read offline

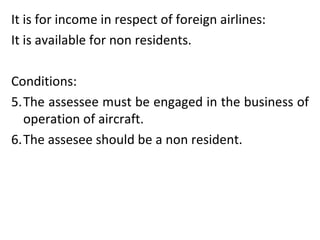

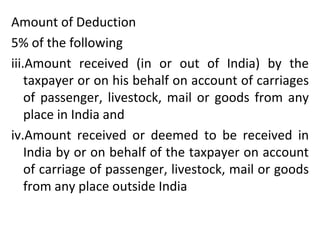

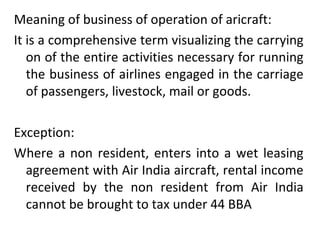

Section 44 BBA provides a 5% deduction for income received by non-resident airlines from carriage of passengers, livestock, mail or goods originating from or traveling to India. To qualify, the non-resident must be engaged in the business of operating aircraft. However, rental income received under a wet leasing agreement with an Indian airline like Air India is exempt from tax under this section.