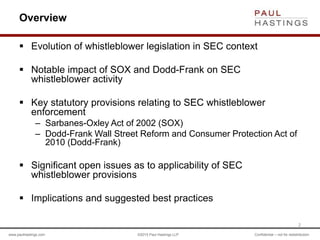

This document summarizes a presentation on SEC whistleblower rules given by attorneys from Paul Hastings LLP. It discusses the evolution of whistleblower legislation including provisions in the False Claims Act, Sarbanes-Oxley Act, and Dodd-Frank Act. Key points include increased incentives for whistleblowers like monetary awards leading to more tips to the SEC. Open legal issues remain around the extraterritorial application of rules and whether internal reporting is protected. Companies are advised to foster compliance cultures and protect whistleblowers to mitigate risks.