Recommended

More Related Content

What's hot

What's hot (19)

Similar to Savillsresearch briefing-brisbane-cbd-office-q2-2019

Similar to Savillsresearch briefing-brisbane-cbd-office-q2-2019 (20)

Recently uploaded

Recently uploaded (9)

Savillsresearch briefing-brisbane-cbd-office-q2-2019

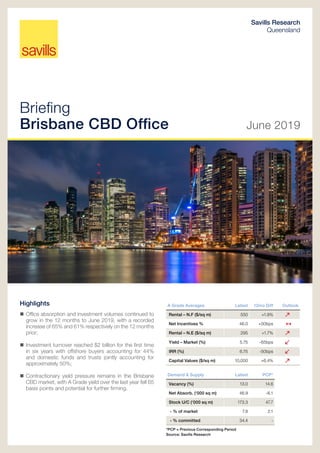

- 1. Briefing Brisbane CBD Office June 2019 Savills Research Queensland Highlights Office absorption and investment volumes continued to grow in the 12 months to June 2019, with a recorded increase of 65% and 61% respectively on the 12 months prior; Investment turnover reached $2 billion for the first time in six years with offshore buyers accounting for 44% and domestic funds and trusts jointly accounting for approximately 50%; Contractionary yield pressure remains in the Brisbane CBD market, with A Grade yield over the last year fell 65 basis points and potential for further firming. A Grade Averages Latest 12mo Diff Outlook Rental – N.F ($/sq m) 550 +1.9% Net Incentives % 46.0 +00bps 1 Rental – N.E ($/sq m) 295 +1.7% Yield – Market (%) 5.75 -65bps IRR (%) 6.75 -50bps Capital Values ($/sq m) 10,000 +6.4% Demand & Supply Latest PCP* Vacancy (%) 13.0 14.6 Net Absorb. (‘000 sq m) 46.9 -6.1 Stock U/C (‘000 sq m) 173.3 47.7 - % of market 7.8 2.1 - % committed 34.4 - *PCP = Previous Corresponding Period Source: Savills Research

- 2. June 2019 savills.com.au/research 2 Savills Research | Briefing Notes – Brisbane CBD Executive Summary Brisbane is increasing its attractiveness transforming into a destination for both domestic and foreign investors on the back of Queensland’s economic growth and multi-billion infrastructure investment. With a notable yield and capital value spread between Brisbane CBD and Sydney and Melbourne CBDs, Brisbane CBD provides an attractive alternative to investors, clearly evidenced by a pickup in investment activity in the annual period with investment turnover exceeding $2 billion for the first time since 2013. Continued improvement in the leasing market and rental growth is expected to see investors re- engage with Brisbane with the search for relative higher yielding assets. However, the effects of the new 2% foreign land tax fee in Queensland on offshore investors, the most active purchaser group in Brisbane CBD for consecutive periods, remain to be seen. Brisbane has recorded the largest drop in office vacancy compared to any other State capital city CBD office market. Demand drivers in Brisbane are much stronger than they were 12 months ago, with lower interest rates, lower AUD, rising net migration and government’s dedicated investment in roads and transport infrastructure likely to provide a material boost to the Queensland economy. Restrained rental growth has seen a trend towards re-centralisation in the CBD, with former fringe tenants relocating to the CBD. PCA Summary Table – Brisbane CBD (as at Dec-18) Premium A Grade Prime Secondary Total AUS CBD Total Stock (‘000) 335.5 936.6 1,272.1 954.9 2,227.0 17,902.6 Total Vacancy (‘000) 34.8 92.6 127.4 161.6 289.0 1,482.7 Vacancy (%) 10.4 (9.6) 9.9 (9.9) 10.0 (9.9) 16.9 (15.6) 13.0 (12.7) 8.3 (9.4) Net Absorption (‘000) 7.4 (16.2) 27.2 (21.7) 34.6 (37.9) 12.3 (-20.5) 46.9 (17.4) 230.7 (181.3) Net Absorption (%) * 2.5 (8.0) 3.3 (3.0) 3.1 (4.1) 1.6 (-2.3) 2.5 (0.9) 1.4 (1.2) Net Additions (‘000) .0 (19.5) .0 (28.1) .0 (47.7) -28.4 (-9.1) -28.4 (38.6) -46.2 (257.6) - Stock Additions (‘000) - - - - - 317.8 - Stock Withdrawals (‘000) 0.0 0.0 0.0 28.4 28.4 364.5 Net Additions (%) 0.0 (9.1) 0.0 (3.6) 0.0 (4.8) -2.9 (-0.9) -1.3 (1.9) -0.3 (1.6) Report Contents Vacancy & Availability 3 Leasing Activity & Demand 4 Sales Activity 6 Supply & Development 8 Rents & Outlook 9 Key Indicators 10 Contacts 11 For our latest national reports, visit savills.com.au/research To join Savills Research mailing list, please email research@savills.com.au Source: PCA / Savills Research (10yr Averages shown in brackets); * As a percentage of occupied stock NB: Secondary Rents shown are for B Grade; All rents equivalent to whole floor mid-rise Research & Consultancy Tracy Tam ttam@savills.com.au Head of Research Research & Consultancy Phil Montgomerie pmontgomerie@savills.com.au

- 3. June 2019 savills.com.au/research 3 Savills Research | Briefing Notes – Brisbane CBD Vacancy Positive levels of net absorption and strengthening tenant demand led to the vacancy rate falling 160 basis points (1.6%) over the second half of 2018, finishing the year at 13.0%, the lowest rate since 2014. Savills Research forecasts ongoing falls in vacancy in Brisbane CBD over 2019, albeit modest, with continued recentralisation and limited upcoming supply this year. The only additional supply in 2019 will be limited to the completion of 300 George Street and Dexus’ 12 Creek Street Annex project. On Savills Research forecasts the vacancy rate should trend downwards over the next 5 years. Full Floor Availability In Savills’ Prime Full Floor Availability Report, the state of the leasing market is assessed in a different manner to most vacancy surveys. The report considers Premium and A grade buildings in the city on a floor-by-floor basis, identifying whole floors competing for tenants - both now and in the future - including those under construction and refurbishment. By Grade By Precinct Total Premium A Grade Financial Uptown Govt. Retail Legal Total Prime Floors (No) 1,081 170 911 426 217 207 90 141 Total Prime NLA (sq m) 1,396,227 260,602 1,135,625 521,199 295,438 274,382 126,251 178,957 Prime Floors Available (No) 165 15 150 58 32 28 6 41 Prime Full Floor Avail. (sq m) 209,346 21,173 188,173 59,818 40,916 44,999 9,003 54,610 Prime Full Floor Avail. (%) 15.0% 8.1% 16.6% 11.5% 13.8% 16.4% 7.1% 30.5% Max Contiguous Floors (No) 29 4 25 13 5 13 3 25 Max Contiguous Area (sq m) 38,986 4,479 34,507 11,069 11,000 22,596 5,100 34,507 Source: Savills Research 0% 5% 10% 15% 20% 25% Prime Secondary Total Historic Vacancy Rate Source: PCA / Savills Research

- 4. June 2019 savills.com.au/research 4 Savills Research | Briefing Notes – Brisbane CBD 50,000 100,000 150,000 200,000 250,000 <= 5,000sqm 5,000sqm - 10,000sqm > 10,000sqm Fin & Ins - 45.9% Govt & Community - 24.2% Mining - 18.6% IT & Comm - 8.1% Prop & Bus Serv - 3.2% Rec Serv - 0.0% W'Sale & Retail - 0.0% Undisclosed - 0.0% (50%) (40%) (30%) (20%) (10%) 0% 10% 20% 30% (150,000) (100,000) (50,000) - 50,000 100,000 150,000 Annual Net Abs. - BRI CBD Prof. Job Ads - QLD 50,000 100,000 150,000 200,000 250,000 <= 5,000sqm 5,000sqm - 10,000sqm > 10,000sqm Fin & Ins - 45.9% Govt & Community - 24.2% Mining - 18.6% IT & Comm - 8.1% Prop & Bus Serv - 3.2% Rec Serv - 0.0% W'Sale & Retail - 0.0% Undisclosed - 0.0% (50%) (40%) (30%) (20%) (10%) 0% 10% 20% 30% (150,000) (100,000) (50,000) - 50,000 100,000 150,000 Annual Net Abs. - BRI CBD Prof. Job Ads - QLD 50,000 100,000 150,000 200,000 250,000 <= 5,000sqm 5,000sqm - 10,000sqm > 10,000sqm Fin & Ins - 45.9% Govt & Community - 24.2% Mining - 18.6% IT & Comm - 8.1% Prop & Bus Serv - 3.2% Rec Serv - 0.0% W'Sale & Retail - 0.0% Undisclosed - 0.0% (50%) (40%) (30%) (20%) (10%) 0% 10% 20% 30% (150,000) (100,000) (50,000) - 50,000 100,000 150,000 Annual Net Abs. - BRI CBD Prof. Job Ads - QLD Source: DOE / Savills Research Leasing Activity & Demand In the 12 months to June 2019, Savills Research identified 135,918 square metres of leasing activity in the Brisbane CBD office market, up 65% on the 12 months prior, and up 4% on the 10-year average. Leasing activity in the ‘Legal’ precinct was the most prominent during this period, accounting for 35% of total leasing activity; the ‘Financial’ precinct followed closely behind accounting for 29% of total leasing activity. In the current annual period, the majority of leases in Brisbane CBD were across Prime Grade buildings, accounting for approximately 41% of recorded leases. This is in line with the continued momentum of the ‘Flight to Quality’ trend which tenants are willing to pay higher prices for better offerings. ‘Direct’ leases accounted for almost half of the office space leased, whereas ‘Pre-commitment’ leases remained prominent with active leasing campaigns on development projects. This is largely as a result of Suncorp’s 39,600 square metre pre-commitment at 80 Ann Street, and Rio Tinto’s relocation from 123 Albert Street to pre-commit to 20,000 square metres at Midtown Centre located at 163 Charlotte Street on a 10-year lease term. Tenants from the ‘Finance & Insurance’ industry remained the most dominant sector, absorbing 46% of total stock. Major leases from this sector include Suncorp (39,600 square metres), Westpac (6,643 square metres) and Gallagher Bassett (2,307 square metres). The ‘Government & Community’ sector remained active, accounting for 24% of all total leasing volumes in the current 12-month period. This was mainly made up of the State Government’s 10,550 square metre commitment at 83-85 George Street, the Department of Veterans Affairs’ 6,414 square metre commitment at 480 Queen Street, Queensland Rail’s 2,000 square metres commitment at 30 Makerston Street and Australia Post’s 4,503 square metre commitment at 259 Queen Street. Leasing Activity by Size (> 1,000 square metres) Source: Savills Research Leasing Activity by Tenant Type (> 1,000 square metres) Source: Savills Research Net Absorption vs. Growth in Professional Job Ads

- 5. June 2019 savills.com.au/research 5 Savills Research | Briefing Notes – Brisbane CBD 0.08% 0.67% 4.78% 6.93% 7.37% 7.52% 8.77% 12.04% ACT NT NSW AUS SA QLD VIC WA Professional job advertisements continued to grow in Queensland, up 7.52% in the 12 months to April 2019. This points to ongoing strength in leasing demand drivers for Brisbane’s CBD office market over the next 6 to 9 months, with business sentiment up for the office sector. According to the latest NAB Commercial Property Index, overall sentiment for the sector was well above its long- term average. Recent Notable Leases (by Area Leased) Tenant Property Date | NLA (sq m) Type | Rent | Term 80 Ann St Suncorp Sep-18 | 39,600 Precommit | 850 (G) | 10 163 Charlotte St Rio Tinto Mar-19 | 20,000 Precommit | 850 (G) | 10 280 Elizabeth St Telstra Jan-19 | 10,600 Leaseback | 300 (N) | 7 123 Eagle St Westpac Jun-18 | 6,643 Direct | 775 (G) | 10 480 Queen St Department of Veterans Affairs Jul-18 | 6,414 Direct | 825 (G) | 10 179 Turbot St Bupa Jul-18 | 6,336 Renewal | 659 (G) | 5 83-85 George St State Gov Oct-18 | 5,319 Direct | 660 (G) | 12 83-85 George St State Gov (AFP) Oct-18 | 5,231 Direct | 660 (G) | 8 259 Queen St Australia Post Feb-19 | 4,503 Direct | 745 (G) | 7 414 George St DHL Express Australia Nov-18 | 3,500 Direct | 600 (G) | 6 180 Ann St Senex Energy Jul-18 | 3,000 Direct | 696 (G) | 7 144 Edward St Gallagher Bassett Dec-18 | 2,307 Direct | 600 (G) | 8 545 Queen St Sonic Healthcare Dec-18 | 2,138 Direct | 600 (G) | 10 30 Makerston St Queensland Rail Dec-18 | 2,000 Direct | 575 (G) | 5 123 Eagle St DWF LLP Jul-18 | 1,603 Direct | 940 (G) | 4 545 Queen St Department of Defence Dec-18 | 1,561 Direct | 625 (G) | 5 Professional Job Advertisement Growth by State (Apr-19) Source: DOE / Savills Research Source: Savills Research

- 6. June 2019 savills.com.au/research 6 Savills Research | Briefing Notes – Brisbane CBD $0m $500m $1,000m $1,500m $2,000m $2,500m $5m - $50m $50m - $100m >$100m 0% 20% 40% 60% 80% 100% Purchasers Vendors Fund Trust Developer Owner Occupier Government Syndicate Foreign Investor Private Investor Other $0m $500m $1,000m $1,500m $2,000m $2,500m $5m - $50m $50m - $100m >$100m 0% 20% 40% 60% 80% 100% Purchasers Vendors Fund Trust Developer Owner Occupier Government Syndicate Foreign Investor Private Investor Other Sales Activity Savills Research recorded approximately $2.06 billion of office sales in the Brisbane CBD over the 12 months to June 2019, up 61% from the 12 months prior and up on the 10 year average of $1.31 billion. With fewer prime grade assets being put on the market for sale, we saw a notable increase in the number of secondary grade buildings transacted ($904 million) in the current annual period, as investors looked to capitalise on the development potential. ‘Foreign Investors’ remained the most dominant purchaser in the year to June 2019, accounting for approximately 44% of all purchaser types. Singaporean investors remained robust in the Brisbane CBD, with notable sales of 280 Elizabeth Street to Firmus Capital ($57 million at an initial passing yield of 5.58%) and 133 Mary Street to ARA Asset Management ($96.5 million corresponding to an equated yield of 5.97%). Foreign investors’ appetite are supported by an Australian environment of low interest rates, and their interest in Brisbane CBD comes as a result of a shift away from the Sydney and Melbourne markets due to record low yields and high capital values in these Southern cities Domestic institutional investors remained active in the market, with ‘Funds’ and ‘Trusts’ jointly accounting for approximately 50% of all purchaser types. Notable transactions include 30 Makerston Street acquired by Sentinel Property Group ($103 million at an equated yield of 7.52%), 201 Charlotte Street acquired by Sydney-based Kyko Group ($126.7 million at an equated yield of 5.90%) and Sydney-based Anton Capital is firming to be the new owner of the contiguous office asset including both 239 George Street and 15 Adelaide Street by paying $226 million to Canadian investor Oxford Properties Group. Reportedly, Oxford Properties Group also offloaded the Australian Government Centre (140 Creek Street, 232 Adelaide & 295 Ann Street) to Ashe Morgan for $430 million. Sales Activity by Price (> $5 million) Source: DOE / Savills Research Vendor & Purchaser Type (> $5 million) Source: Savills Research Brisbane CBD A Grade - Yield Range to 10yr Bond 0.0 2.0 4.0 6.0 8.0 10.0 12.0 10yr Bond Rate Market Yield - Average IRR - Avg Source: Savills Research

- 7. June 2019 savills.com.au/research 7 Savills Research | Briefing Notes – Brisbane CBD - 1.00 2.00 3.00 4.00 5.00 6.00 7.00 8.00 9.00 2,000 4,000 6,000 8,000 10,000 12,000 Capital Value - BRI CBD Market Yield (RHS) Source: Savills Research A Grade market yield in Brisbane CBD, as at June 2019, are typically estimated to range from 5.25% to 5.75%. The average A Grade yield for Brisbane CBD office buildings fell 65 basis points. Average A Grade capital values were recorded at $10,000 per square metre reflecting a growth of 6.4% over the year to June 2019. Investment focus of both domestic and offshore investors will likely move away from the Southern cities to the more affordable Brisbane CBD alternative, as suggested by the significant difference in yields and capital values between Brisbane CBD and Sydney CBD. Other than the pickup of investors’ interest, a positive tenancy outlook and rental growth forecasts will contribute to the rising trend of capital values in Brisbane CBD in 2019. Recent Notable Sales (by Sale Price) Property Price ($m) | Date | NLA Yield | Type | $/sq m 80 Ann St (50%) 418.00 | Jul-18 | 60,000 5.00 | i | 13,933 61 Mary St 275.00 | Nov-18 | 28,741 5.95 | e | 9,568 239 George St & 15 Adelaide St 226.00 | May-19 | 35,671 n.a | n.a | 6,336 201 Charlotte St 126.70 | May-19 | 13,291 5.90 | e | 9,533 288 Edward St 113.42 | Feb-19 | 19,918 6.75 | e | 5,694 343 Albert St / 143 Turbot St 110.00 | Jul-18 | 19,873 6.77 | e | 5,535 30 Makerston St 103.00 | May-19 | 14,640 7.52 | e | 7,036 133 Mary St 96.50 | Mar-19 | 12,987 5.97 | e | 7,431 260 Queen St 95.25 | Jul-18 | 12,934 6.40 | e | 7,364 40 Tank St 93.00 | Aug-18 | 6,218 5.93 | e | 14,957 100 Edward St 64.00 | Jul-18 | 7,122 6.03 | e | 8,986 83-85 George St 60.00 | Oct-18 | 10,550 6.00 | r | 5,687 280 Elizabeth St 57.00 | Jun-19 | 10,600 5.58 | i | 5,377 179 North Quay 52.60 | Dec-18 | 8,525 6.55 | i | 6,170 293 Queen St 52.25 | Oct-18 | 5,257 5.75 | e | 9,939 95 North Quay 46.20 | Aug-18 | 8,416 7.66 | e | 5,490 60 Queen St 41.00 | Sep-18 | 3,144 7.45 | r | 13,041 110 Eagle St 35.25 | Jul-18 | 5,517 6.59 | e | 6,390 Capital Value ($/sq m) vs. Market Yield Source: Savills Research; Yield Types: i = Initial, r = Reported, e = Equated, v = Vacant, dev = development

- 8. June 2019 savills.com.au/research 8 Savills Research | Briefing Notes – Brisbane CBD Supply After a period of low supply in the Brisbane CBD office market across 2017 and 2018, developments due from 2019 will help aid in additional supply. The 48,000 square metre development of 300 George Street and the 8,003 square metre development of Dexus’ 12 Creek Street Annex are currently under construction and are due for completion in 2019. Construction of Midtown Centre has also commenced after Rio Tinto pre-committed close to 48% of the building for 10 years and is expected to be completed by 2021. 80 Ann Street (which is due to be completed in 2022) is also currently under construction, noting Suncorp’s pre-commitment to approximately 66% of the building for 10 years. It is important to note that the adjoining chart reflects developments that are still in the planning phase. Whilst some developments have been given DAs by Brisbane City Council, construction is subject to significant pre- commitments. Net Supply by Year (square metres) (60,000) (40,000) (20,000) - 20,000 40,000 60,000 80,000 100,000 120,000 140,000 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 Historic Net Additions Savills Forecast 15yr Avg Source: Savills Research / PCA The table below details the major upcoming and planned development projects in the Brisbane CBD. Building Address Dev Stage NLA Exp. Comp Precinct Tenants 320 George St DA 10,000 2019 Legal 12 Creek St (The Annex) UC 8,003 2019 Financial 300 George St UC 48,000 2019 Legal 163 Charlotte St (Midtown Centre) UC 42,000 2021 Government Rio Tinto 62 Mary St PS 38,000 2022 Government 80 Ann St UC 75,339 2022 Uptown Suncorp 150 Elizabeth St (Regent Tower) DA 48,000 2023 Retail 360-380 Queen St DA 50,000 2023 Financial 205 North Quay EP 50,000 2023 Legal Development Source: Savills Research; UC = Under Construction, EP = Early Planning, PS = Plans Submitted, PA = Plans Approved, DA = Development Approved

- 9. June 2019 savills.com.au/research 9 Savills Research | Briefing Notes – Brisbane CBD Rents Average A Grade net face rents ranged from $500 and $600 per square metre, with a 1.9% rental growth recorded over the year to June 2019. The upward trend of development activity in Brisbane CBD has been a key reason for stagnant rental growth. A recovery in rental growth is expected throughout 2019 after nearly five years of stagnant growth in Brisbane CBD. Whilst growth in net face rents was not evident in the 12 months to June 2019, the strong demand from both public and private sectors will likely drive up rental rates over the next two years. With the continuing momentum of ‘Flight to Quality’ among new tenants combined with a lack of prime grade options in the CBD will likely push up rental growth on an effective basis and tighten vacancy over the next 2-3 years. Outlook A turnaround in Brisbane CBD is emerging, with an optimistic outlook throughout 2019 and beyond. The market is set to experience a reversion after hitting the bottom of the cycle from a weak economy and falling mining investments over the last 5 years. Savills Research expect a pickup in the State economy supported by a weak Australian dollar driving foreign visitation and tourism spend, firmer commodity prices, significant public infrastructure investment and steady population growth will boost various sectors of the economy and therefore investment sentiment. The Brisbane sales market has witnessed a revived wave of capital enter from both domestic and foreign investors in search of higher yielding assets and relatively more affordable investment alternatives. With a notable spread between Brisbane CBD and Sydney CBD, current market conditions point to more room for tightening in Brisbane CBD. Savills Research anticipates rental rates to edge upwards as vacancy rates drop to the lowest recorded level in five years as a result of a combination of limited new supply and strong tenant demand. Capitalisation rates will be further tightened as domestic and global players seek to take advantage of the yield arbitrage compared to Southern cities. The new land tax changes are likely to negatively impact foreign buyers yet the degree of impact is unknown. Net Effective Rents by Grade ($/sq m) Source: Savills Research Net Face & Net Effective Rents as at Jun-19 ($/sq m) Source: Savills Research - 100 200 300 400 500 600 Premium Grade A Grade B 690 540 430 395 295 200 0% 10% 20% 30% 40% 50% 60% - 100 200 300 400 500 600 700 800 Premium Grade A Grade B Net Face Rent Net Effective Rent Net Incentive % - rhs690 550 430 395 295 200 0% 10% 20% 30% 40% 50% 60% - 100 200 300 400 500 600 700 800 Premium Grade A Grade B Net Face Rent Net Effective Rent Net Incentive % - rhs

- 10. June 2019 savills.com.au/research 10 Savills Research | Briefing Notes – Brisbane CBD Brisbane CBD Key Indicators (Q2-19) Premium A Grade B Grade Low High Low High Low High Rental - Gross Face ($/sq m) 815 920 635 775 545 605 Rental - Net Face ($/sq m) 635 740 500 600 400 460 Incentive Level Net 30% 37% 32% 38% 38% 43% Rental - Net Effective ($/sq m) 360 430 255 330 180 215 Outgoings - Operating ($/sq m) 95 120 85 95 70 85 Outgoings - Statutory ($/sq m) 65 75 60 80 55 80 Outgoings - Total ($/sq m) 160 195 145 175 125 165 Typical Lease Term 7 10 3 7 3 7 Yield - Market (% Net Face Rental) 5.00 5.75 5.25 5.75 6.00 7.50 IRR (%) 6.50 7.00 6.50 7.00 7.00 7.50 Cars Permanent Reserved ($/pcm) 600 850 500 650 450 550 Cars Permanent ($/pcm) 450 650 400 550 300 500 Office Capital Values ($/sq m) 12,250 14,500 8,500 11,500 5,500 8,000 Source: Savills Research NB: All rents equivalent to whole floor mid-rise

- 11. June 2019 savills.com.au/research 11 Savills Research | Briefing Notes – Brisbane CBD Key State Office Contacts Research & Consultancy Tracy Tam +61 (0) 7 3002 8859 ttam@savills.com.au Metro & Regional Sales Gregory Woods +61 (0) 7 3002 8825 gwoods@savills.com.au Office Leasing John McDonald +61 (0) 7 3002 8847 jmcdonald@savills.com.au Project Management Ken Ng +61 (0) 7 3018 6705 kng@savills.com.au Valuations Brett Schultz +61 (0) 7 3002 8855 bschultz@savills.com.au Asset Management Phillip Dunn +61 (0) 7 3002 8831 pdunn@savills.com.au Capital Transactions Peter Chapple +61 (0) 7 3002 8858 pchapple@savills.com.au Commercial Sales Robert Dunne +61 (0) 7 3002 8806 rdunne@savills.com.au Savills is a leading global property service provider listed on the London Stock Exchange. Trusted since 1855, we have extensive experience across the Asia Pacific, with over 50 offices, and in Australia, we have over 800 staff focused on meeting all your property needs. Disclaimer This comunciation has been prepared by Savills (Aust) Pty Ltd’s Research Team (“Savills”) for general information only and is not intended to be relied upon in any way. Information, projections and images Information contained in this communication has been obtained from materials and sources believed to be reliable at the date of publication, however Savills has not taken steps to verify or certify its accuracy or completeness. Opinions, projections and forecasts in this communication depend on the accuracy of any information and assumptions on which they are based, and on prevailing market conditions, for which Savills does not accept responsibility. No representations or warranties of any nature are given, intended or implied by Savills about this communication, any information, opinions and forecasts contained within this communication or the accuracy or enforceability of any material referred to in this communication. Savills (including its employees, officers and agents) any of the employees of Savills referenced in the communication will not be liable, including in negligence, for any direct, indirect, special, incidental or consequential losses or damages arising out of or in any way connected with use of or reliance on anything in this communication. For the avoidance of doubt, Savills (including its employees, officers and agents) will not be liable for any investment decision based in whole or in part on the information or projections contained herein. All images are only for illustrative purposes. Given the above, Savills strongly advises all recipients of this communication to exercise caution and to conduct their own due diligence on the relevance, accuracy, completeness and currency of the information in this communication. This communication does not form part of or constitute an offer or contract. GST Unless otherwise expressly stated, all amounts, prices, values or other sums stated in this document are exclusive of GST. Confidentiality This communication is the confidential information of Savills and is strictly for the intended recipient. This communication must not be disclosed to any other party without the prior written consent of Savills. Copyright This communication is copyright material owned by Savills. Permission to use any part of this document must be sought directly from Savills. The Savills Research & Consultancy team has years of experience, and is supported by our extensive agency, property management and valuation professionals. For national-level consultancy or subscription requirements please contact: Capital Strategy & Research Phil Montgomerie +61 (0) 2 8215 8971 pmontgomerie@savills.com.au