Download to read offline

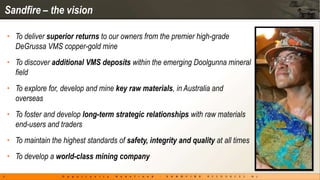

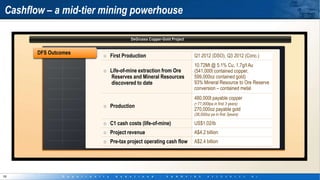

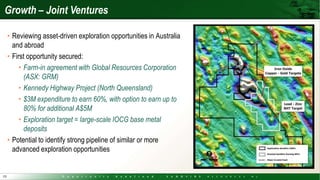

Sandfire Resources has begun mining at its new DeGrussa copper-gold mine in Western Australia, opening a new chapter of growth for the company. Key points: - Mining commenced in February 2012 with the first shipment of development ore. Underground mining will begin in Q3 2012. - DeGrussa is expected to produce on average 77,000 tonnes of payable copper and 36,000 ounces of gold annually for the first three years. - The mine has a projected life of over 7 years and is fully funded. Production will establish Sandfire as a mid-tier mining company and generate significant cash flow. - Exploration potential remains along a 30km prospective corridor, providing

![Silvercrest january 2013 [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/silvercrestjanuary2013compatibilitymode-130123141613-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)