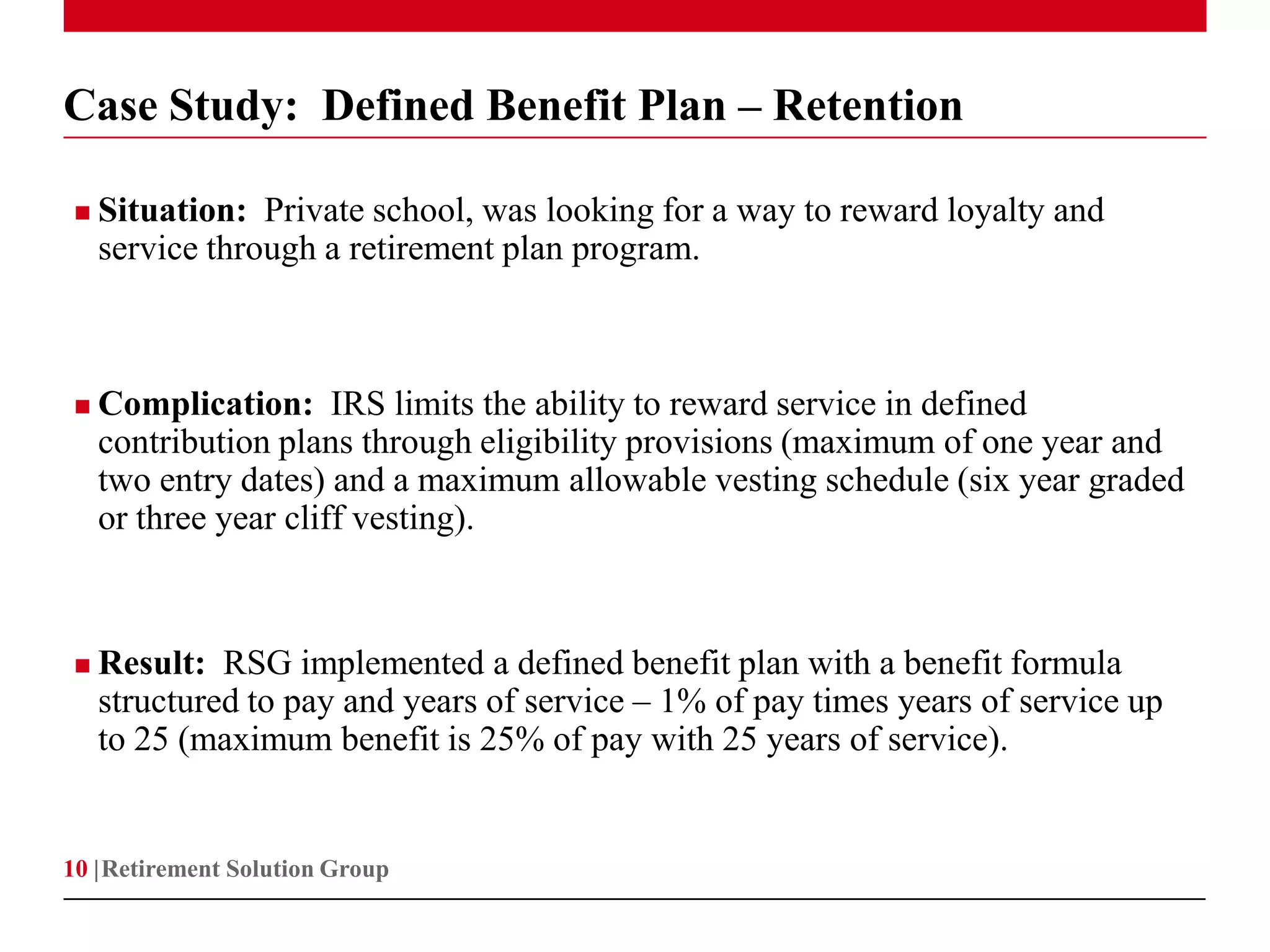

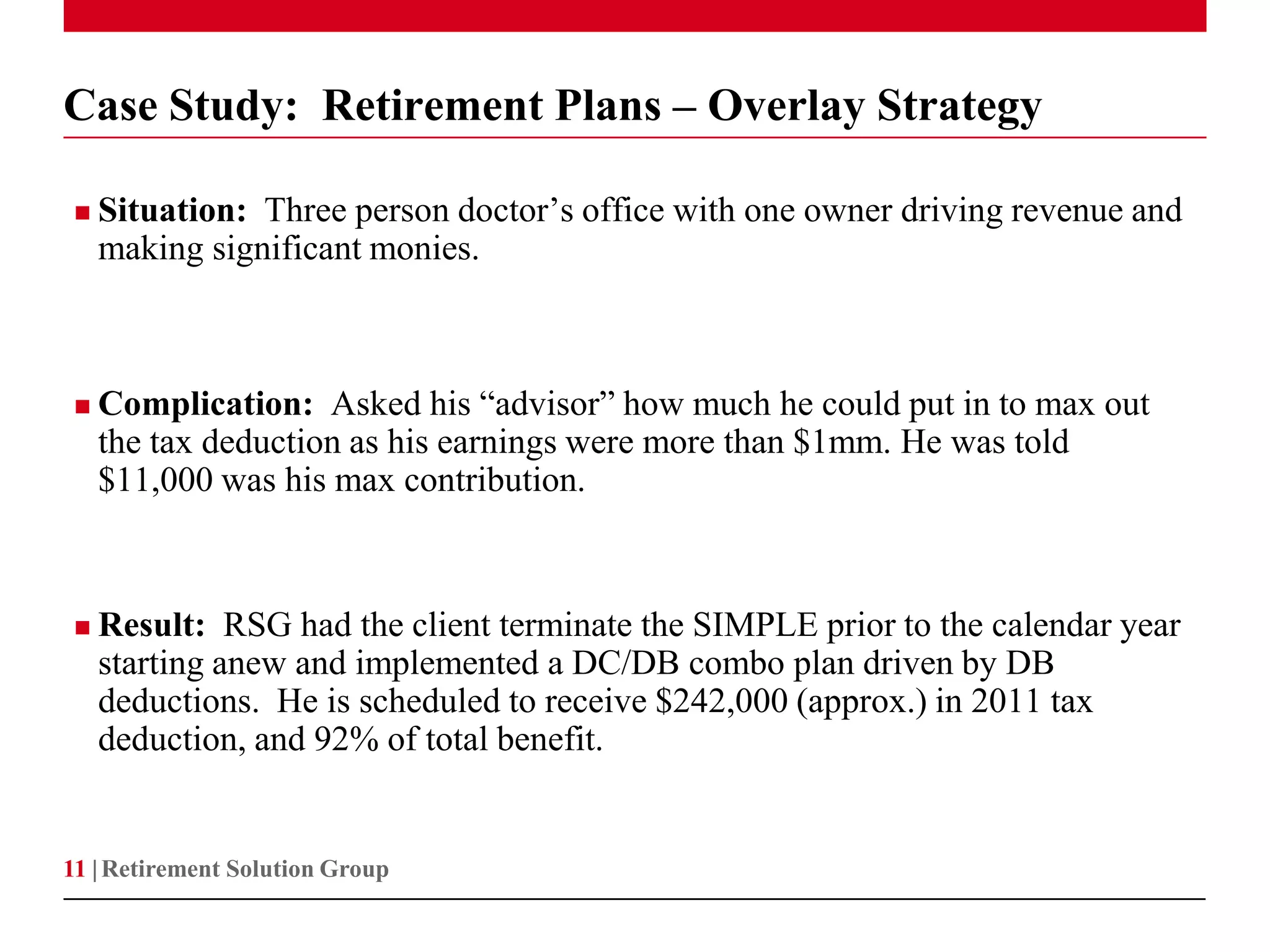

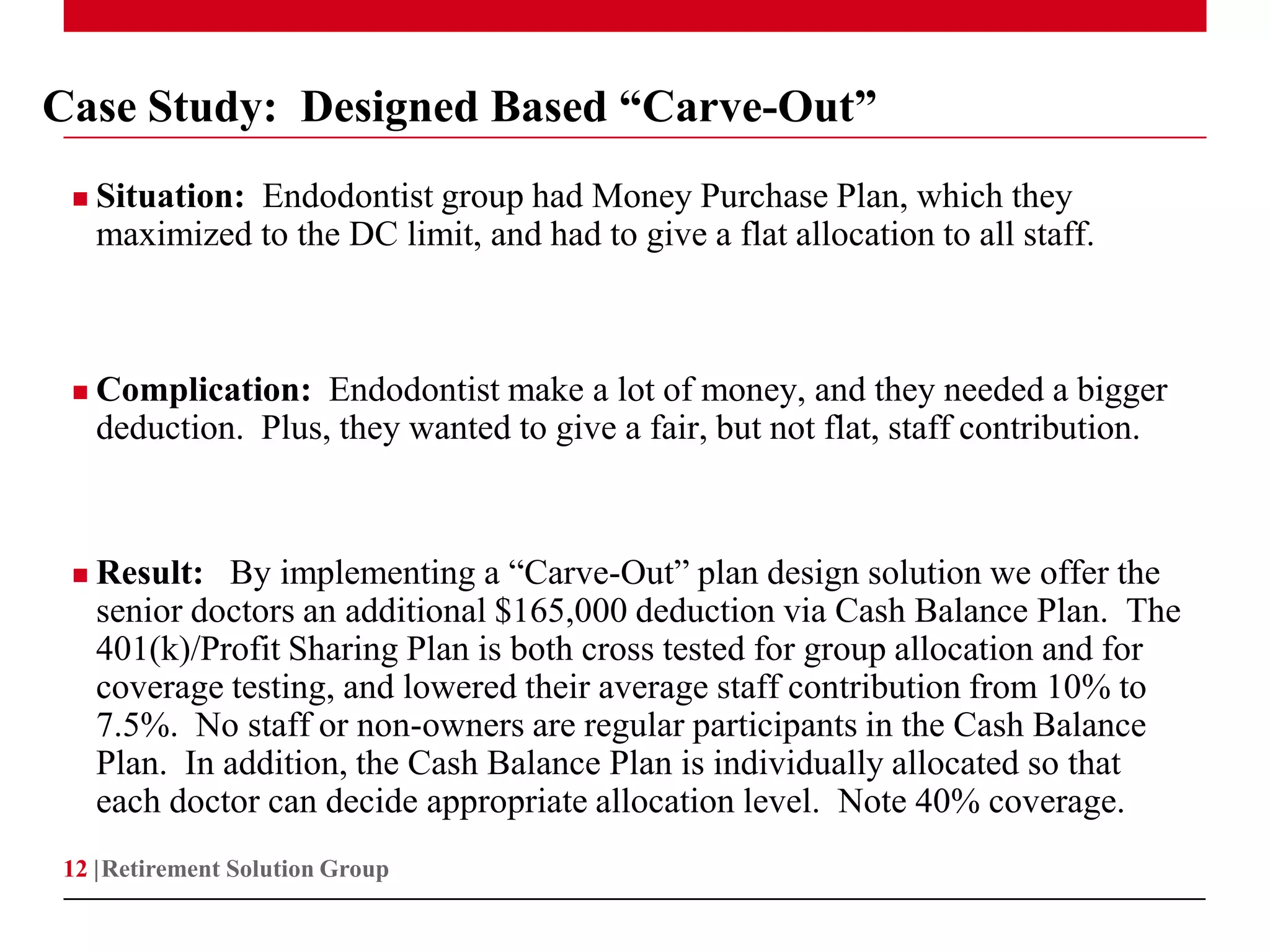

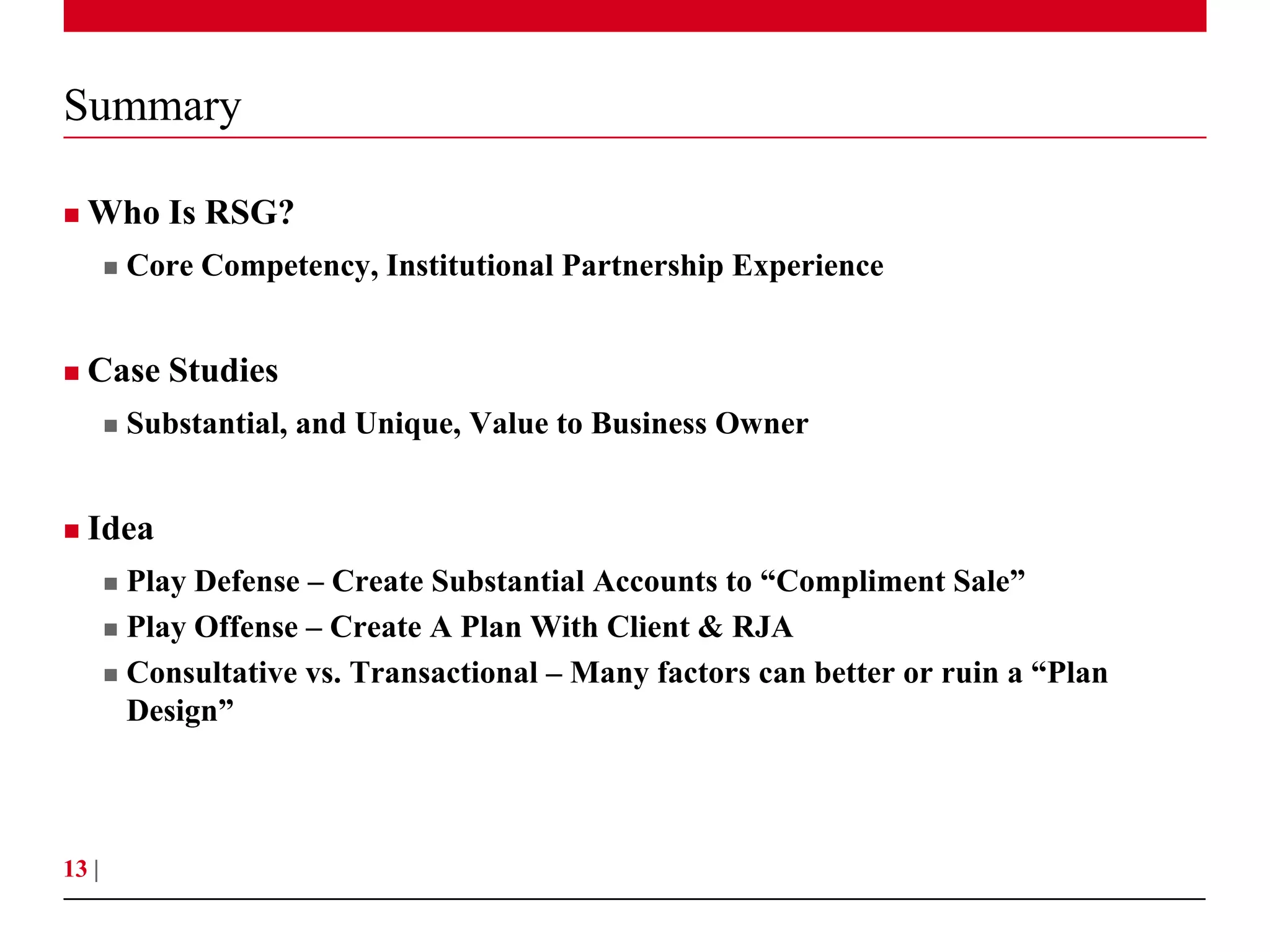

Download to read offline

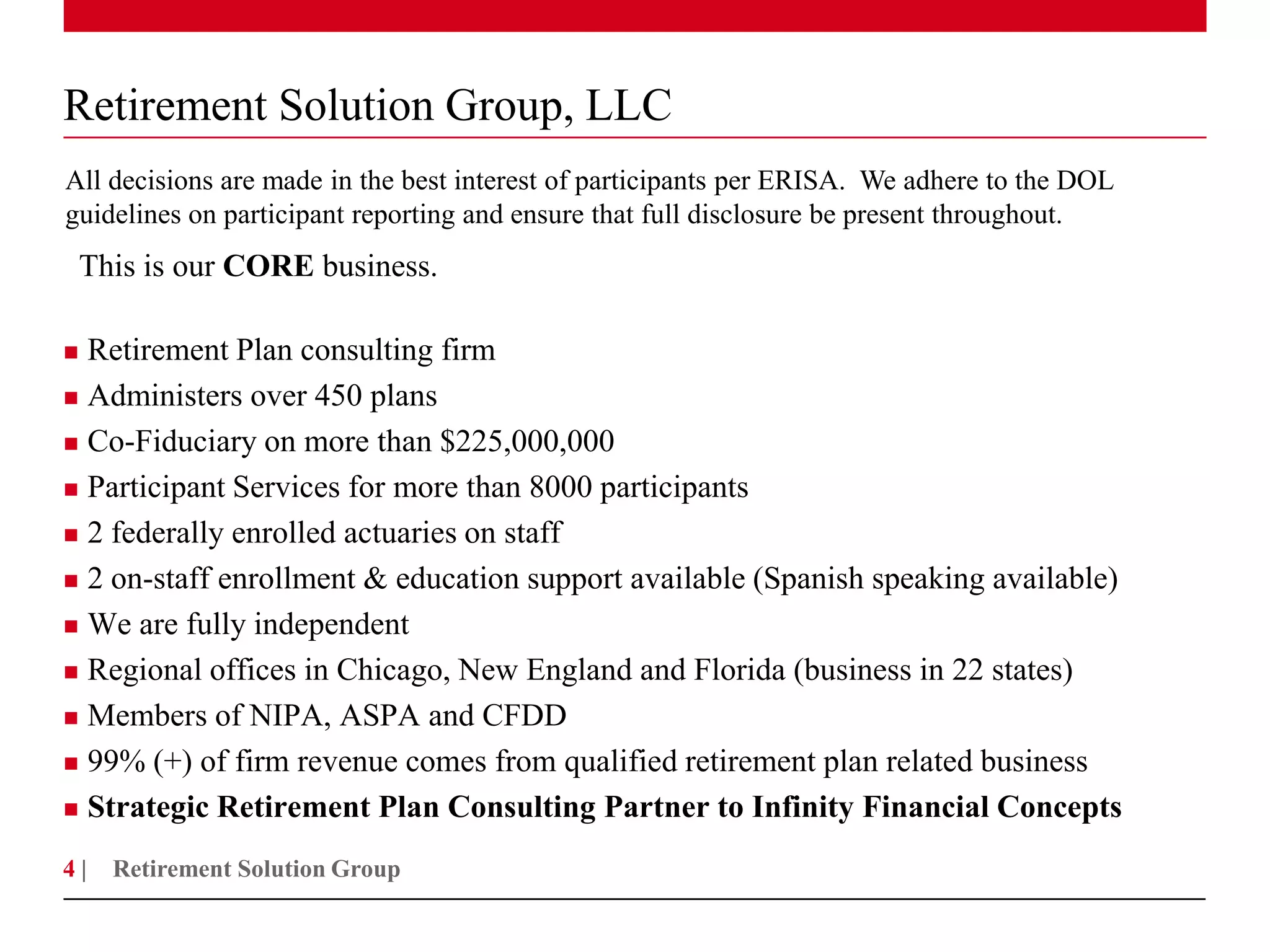

The presentation discusses retirement plan solutions for business owners provided by Retirement Solution Group (RSG). RSG specializes in customized qualified retirement plans that maximize tax benefits for business owners. The presentation outlines RSG's services and credentials and provides case studies of plans they have designed for clients in different industries that significantly increased owners' tax deductions and retirement benefits over traditional plans. It promotes working with RSG to analyze a business owner's situation and design a strategic "transaction plan" to supplement proceeds from selling their business.