Sample 8949 Document BearTax

•

1 like•561 views

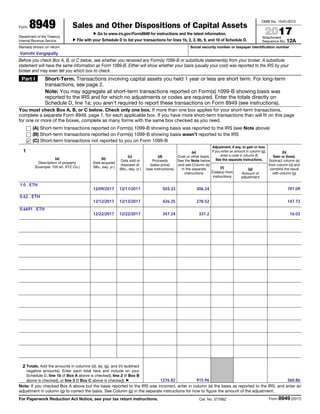

Sample document of 8949 capital gains form auto-generated by BearTax based on your cryptocurrency trades over the period of a given tax year

Report

Share

Report

Share

Download to read offline

Recommended

How to implement general ledger

TATA Group is implementing SAP across functions. As part of the Finance implementation, general ledger must be set up in SAP. This involves defining the length of general ledger accounts, assigning the chart of accounts to the company code "TATA", defining account groups based on requirements, creating retained earnings accounts, and creating general ledger accounts either manually or using reference data. Tolerance groups for transactions must also be defined to control posting limits.

Basic configuration settings for fi asset accounting

This document provides instructions for configuring asset accounting in SAP. It outlines 20 steps for basic setup including: 1) defining charts of depreciation and depreciation areas, 2) assigning charts of depreciation to company codes, 3) creating asset classes and specifying account determination, 4) maintaining depreciation keys, 5) creating asset master records, 6) acquiring and capitalizing assets, 7) settling assets under construction, 8) retiring assets, 9) transferring assets between records, and 10) transferring assets between company codes. Screenshots and transaction codes are provided for each configuration step.

SAP Assets Accounting Configuration

This document outlines the configuration of depreciation rules and account assignments for assets across company codes. It includes definitions for depreciation areas, asset classes, charts of depreciation, and account determination rules. Screen layouts and number ranges are also specified for asset master data and depreciation documents.

1099 c 2008

The document is an IRS form 1099-C for reporting canceled debt to the IRS. It provides instructions for creditors on filing and furnishing the form to report debts of $600 or more that have been canceled or forgiven. It also provides instructions for debtors on what canceled debt needs to be reported as income and the boxes on the form describing the debt canceled. Creditors must file Copy A with the IRS and furnish Copy B to debtors by February 2, 2009.

1099 c 2008

The document provides instructions for Form 1099-C, which is used to report canceled debt to the IRS. It explains that if a financial institution cancels $600 or more of debt, it must file a Form 1099-C with the IRS and provide a copy to the debtor. It provides details on what amounts must be reported as income and exceptions for certain types of canceled or reduced debt. It also describes the boxes on the form and due dates for filing with the IRS.

SCHEDULE E (Form 1040) Department of the Treasury In.docx

SCHEDULE E

(Form 1040)

Department of the Treasury

Internal Revenue Service (99)

Supplemental Income and Loss

(From rental real estate, royalties, partnerships, S corporations, estates, trusts, REMICs, etc.)

▶ Attach to Form 1040, 1040NR, or Form 1041.

▶ Information about Schedule E and its separate instructions is at www.irs.gov/schedulee.

OMB No. 1545-0074

2014

Attachment

Sequence No. 13

Name(s) shown on return Your social security number

Part I Income or Loss From Rental Real Estate and Royalties Note. If you are in the business of renting personal property, use

Schedule C or C-EZ (see instructions). If you are an individual, report farm rental income or loss from Form 4835 on page 2, line 40.

A Did you make any payments in 2014 that would require you to file Form(s) 1099? (see instructions) Yes No

B If “Yes,” did you or will you file required Forms 1099? Yes No

1a Physical address of each property (street, city, state, ZIP code)

A

B

C

1b Type of Property

(from list below)

A

B

C

2 For each rental real estate property listed

above, report the number of fair rental and

personal use days. Check the QJV box

only if you meet the requirements to file as

a qualified joint venture. See instructions.

Fair Rental

Days

Personal Use

Days

QJV

A

B

C

Type of Property:

1 Single Family Residence

2 Multi-Family Residence

3 Vacation/Short-Term Rental

4 Commercial

5 Land

6 Royalties

7 Self-Rental

8 Other (describe)

Income: Properties: A B C

3 Rents received . . . . . . . . . . . . . 3

4 Royalties received . . . . . . . . . . . . 4

Expenses:

5 Advertising . . . . . . . . . . . . . . 5

6 Auto and travel (see instructions) . . . . . . . 6

7 Cleaning and maintenance . . . . . . . . . 7

8 Commissions. . . . . . . . . . . . . . 8

9 Insurance . . . . . . . . . . . . . . . 9

10 Legal and other professional fees . . . . . . . 10

11 Management fees . . . . . . . . . . . . 11

12 Mortgage interest paid to banks, etc. (see instructions) 12

13 Other interest. . . . . . . . . . . . . . 13

14 Repairs. . . . . . . . . . . . . . . . 14

15 Supplies . . . . . . . . . . . . . . . 15

16 Taxes . . . . . . . . . . . . . . . . 16

17 Utilities . . . . . . . . . . . . . . . . 17

18 Depreciation expense or depletion . . . . . . . 18

19 Other (list) ▶ 19

20 Total expenses. Add lines 5 through 19 . . . . . 20

21 Subtract line 20 from line 3 (rents) and/or 4 (royalties). If

result is a (loss), see instructions to find out if you must

file Form 6198 . . . . . . . . . . . . . 21

22 Deductible rental real estate loss after limitation, if any,

on Form 8582 (see instructions) . . . . . . . 22 ( ) ( ) ( )

23a Total of all amounts reported on line 3 for all rental properties . . . . 23a

b Total of all amounts reported on line 4 for all royalty properties . . . . 23b

c Total of all amounts reported on line 12 for all propertie.

Fb08 how to reverse a document in sap t code

To reverse a document in SAP, you use transaction code FB08. You enter the document number, company code, fiscal year, and a reversal reason. The system will generate a reversing document that posts the proper debit and credit amounts to reverse the original document. To reverse a document, access FB08, enter the required fields for the document to reverse, and post the reversing document. The system will confirm the reversal by posting amounts to offset the original document.

How to transition from being a sole proprietor and eliminate your self-employ...

This document provides information about transitioning from being a sole proprietor to an S-corporation to eliminate self-employment taxes. It discusses the risks of being a sole proprietor and advantages of being an S-corp. It illustrates how a hypothetical sole proprietor named George Bailey pays self-employment taxes but could eliminate them by electing S-corp status and paying himself a salary instead of taking distributions. The document aims to educate sole proprietors on this tax savings strategy and provide resources to help with the transition.

Recommended

How to implement general ledger

TATA Group is implementing SAP across functions. As part of the Finance implementation, general ledger must be set up in SAP. This involves defining the length of general ledger accounts, assigning the chart of accounts to the company code "TATA", defining account groups based on requirements, creating retained earnings accounts, and creating general ledger accounts either manually or using reference data. Tolerance groups for transactions must also be defined to control posting limits.

Basic configuration settings for fi asset accounting

This document provides instructions for configuring asset accounting in SAP. It outlines 20 steps for basic setup including: 1) defining charts of depreciation and depreciation areas, 2) assigning charts of depreciation to company codes, 3) creating asset classes and specifying account determination, 4) maintaining depreciation keys, 5) creating asset master records, 6) acquiring and capitalizing assets, 7) settling assets under construction, 8) retiring assets, 9) transferring assets between records, and 10) transferring assets between company codes. Screenshots and transaction codes are provided for each configuration step.

SAP Assets Accounting Configuration

This document outlines the configuration of depreciation rules and account assignments for assets across company codes. It includes definitions for depreciation areas, asset classes, charts of depreciation, and account determination rules. Screen layouts and number ranges are also specified for asset master data and depreciation documents.

1099 c 2008

The document is an IRS form 1099-C for reporting canceled debt to the IRS. It provides instructions for creditors on filing and furnishing the form to report debts of $600 or more that have been canceled or forgiven. It also provides instructions for debtors on what canceled debt needs to be reported as income and the boxes on the form describing the debt canceled. Creditors must file Copy A with the IRS and furnish Copy B to debtors by February 2, 2009.

1099 c 2008

The document provides instructions for Form 1099-C, which is used to report canceled debt to the IRS. It explains that if a financial institution cancels $600 or more of debt, it must file a Form 1099-C with the IRS and provide a copy to the debtor. It provides details on what amounts must be reported as income and exceptions for certain types of canceled or reduced debt. It also describes the boxes on the form and due dates for filing with the IRS.

SCHEDULE E (Form 1040) Department of the Treasury In.docx

SCHEDULE E

(Form 1040)

Department of the Treasury

Internal Revenue Service (99)

Supplemental Income and Loss

(From rental real estate, royalties, partnerships, S corporations, estates, trusts, REMICs, etc.)

▶ Attach to Form 1040, 1040NR, or Form 1041.

▶ Information about Schedule E and its separate instructions is at www.irs.gov/schedulee.

OMB No. 1545-0074

2014

Attachment

Sequence No. 13

Name(s) shown on return Your social security number

Part I Income or Loss From Rental Real Estate and Royalties Note. If you are in the business of renting personal property, use

Schedule C or C-EZ (see instructions). If you are an individual, report farm rental income or loss from Form 4835 on page 2, line 40.

A Did you make any payments in 2014 that would require you to file Form(s) 1099? (see instructions) Yes No

B If “Yes,” did you or will you file required Forms 1099? Yes No

1a Physical address of each property (street, city, state, ZIP code)

A

B

C

1b Type of Property

(from list below)

A

B

C

2 For each rental real estate property listed

above, report the number of fair rental and

personal use days. Check the QJV box

only if you meet the requirements to file as

a qualified joint venture. See instructions.

Fair Rental

Days

Personal Use

Days

QJV

A

B

C

Type of Property:

1 Single Family Residence

2 Multi-Family Residence

3 Vacation/Short-Term Rental

4 Commercial

5 Land

6 Royalties

7 Self-Rental

8 Other (describe)

Income: Properties: A B C

3 Rents received . . . . . . . . . . . . . 3

4 Royalties received . . . . . . . . . . . . 4

Expenses:

5 Advertising . . . . . . . . . . . . . . 5

6 Auto and travel (see instructions) . . . . . . . 6

7 Cleaning and maintenance . . . . . . . . . 7

8 Commissions. . . . . . . . . . . . . . 8

9 Insurance . . . . . . . . . . . . . . . 9

10 Legal and other professional fees . . . . . . . 10

11 Management fees . . . . . . . . . . . . 11

12 Mortgage interest paid to banks, etc. (see instructions) 12

13 Other interest. . . . . . . . . . . . . . 13

14 Repairs. . . . . . . . . . . . . . . . 14

15 Supplies . . . . . . . . . . . . . . . 15

16 Taxes . . . . . . . . . . . . . . . . 16

17 Utilities . . . . . . . . . . . . . . . . 17

18 Depreciation expense or depletion . . . . . . . 18

19 Other (list) ▶ 19

20 Total expenses. Add lines 5 through 19 . . . . . 20

21 Subtract line 20 from line 3 (rents) and/or 4 (royalties). If

result is a (loss), see instructions to find out if you must

file Form 6198 . . . . . . . . . . . . . 21

22 Deductible rental real estate loss after limitation, if any,

on Form 8582 (see instructions) . . . . . . . 22 ( ) ( ) ( )

23a Total of all amounts reported on line 3 for all rental properties . . . . 23a

b Total of all amounts reported on line 4 for all royalty properties . . . . 23b

c Total of all amounts reported on line 12 for all propertie.

Fb08 how to reverse a document in sap t code

To reverse a document in SAP, you use transaction code FB08. You enter the document number, company code, fiscal year, and a reversal reason. The system will generate a reversing document that posts the proper debit and credit amounts to reverse the original document. To reverse a document, access FB08, enter the required fields for the document to reverse, and post the reversing document. The system will confirm the reversal by posting amounts to offset the original document.

How to transition from being a sole proprietor and eliminate your self-employ...

This document provides information about transitioning from being a sole proprietor to an S-corporation to eliminate self-employment taxes. It discusses the risks of being a sole proprietor and advantages of being an S-corp. It illustrates how a hypothetical sole proprietor named George Bailey pays self-employment taxes but could eliminate them by electing S-corp status and paying himself a salary instead of taking distributions. The document aims to educate sole proprietors on this tax savings strategy and provide resources to help with the transition.

Form 1040Form 1040 Department of the Treasury Internal Revenue Ser.docx

Form 1040Form 1040 Department of the Treasury Internal Revenue Service2013U.S. Individual Tax FormOMB No.1545-0074IRS Use Only--Do not write or staple in this spaceFor the year Jan.1--Dec. 31,2013, or any other tax year beginning,2013,,20See Separate InstructionsYour first name and initialLast nameSocial Security NumberIf a joint return, spouses first name and initialLast nameSpouse Social Security NumberHome address( number and street). If you have a P.O. Box, see instructionsMake Sure that the SSN(s) above and on line 6c are correct.City, town, or post office, state, and zip code. If you have a foreign address, also complete spaces below (see instructions).Presidential Election CampaignCheck here if you, or your spouse if filing jointly,Foreign country nameForeign province/state/countryForeign postal codechecking this box below will not change your taxrefund.youspouseFiling Status1. Single4.Head of Household (with qualifying person.) (See instructions.) IfCheck only one box2.. married filing jointlythe qualifying person is a child but not your dependent, enter this3. Married filing separately. Enter spouse's SSN abovechild's name hereand full name here.5. Qualifying Window(er) with dependent childExemptions6a Yourself. If someone can claim you as a dependent, do not check box 6a]Boxes checkedb spouse]on 6a and 6bIf more than fourc. Dependentsdependents, see(1) First nameLast name(2) dependents(3) dependents (4) check if child under age 17No. of childreninstructions and social security numberrelationship to youqualifying for tax credit seeon 6c who:check hereinstructions.lived with youdid not live with youdue to divorce orseparation(see instructions)Dependents on6c not entered aboved. Total number of Exemptions ClaimedAdd numbers on lines aboveIncome7Wages, salaries, tips, etc. Attach Forms (W-2)78aTaxable interest. Attach Schedule B if required8aAttach Form(s)bTax-exempt interest. Do not include on line 8a8bW-2 here. Also9aOrdinary dividends. Attach Schedule B if required9aattach Forms(s) bQualified dividends9bW-2 and 1099-R10Taxable refunds, credits, or offsets state or local income taxes10if tax was withheld.11Alimony received1112Business income or (loss). Attach Schedule C or C-EZ12If you did not 13Capital gain or (loss). Attach Schedule D if required. If not required, check here13get a W-2,14other gains or (losses). Attach Form 479714see instructions15aIRA distributions15ab Taxable amount15b16aPensions and annuities16ab Taxable amount16b17Rental real estate, royalties, partnerships, S corporations, trusts, etc. Attach Schedule E1718Farm income or (loss). Attach Schedule F1819Unemployment compensation1920aSocial security benefits20ab Taxable amount20b21other income. List type and amount2122combine the amounts in the far right column for lines 7 through 21. This is your total incomeThis is your total income.22Adjusted 23Educator expenses23Gross24Certain business expenses of reservists, performing artists, and fee-basis government. Atta ...

Form 8960Department of the Treasury Internal Revenue Serv.docx

Form 8960

Department of the Treasury

Internal Revenue Service (99)

Net Investment Income Tax—

Individuals, Estates, and Trusts

▶ Attach to your tax return.

▶ Information about Form 8960 and its separate instructions is at www.irs.gov/form8960.

OMB No. 1545-2227

2016

Attachment

Sequence No. 72

Name(s) shown on your tax return Your social security number or EIN

Part I Investment Income Section 6013(g) election (see instructions)

Section 6013(h) election (see instructions)

Regulations section 1.1411-10(g) election (see instructions)

1 Taxable interest (see instructions) . . . . . . . . . . . . . . . . . . . . . 1

2 Ordinary dividends (see instructions) . . . . . . . . . . . . . . . . . . . . 2

3 Annuities (see instructions) . . . . . . . . . . . . . . . . . . . . . . . 3

4a Rental real estate, royalties, partnerships, S corporations, trusts,

etc. (see instructions) . . . . . . . . . . . . . . . 4a

b Adjustment for net income or loss derived in the ordinary course of

a non-section 1411 trade or business (see instructions) . . . . 4b

c Combine lines 4a and 4b . . . . . . . . . . . . . . . . . . . . . . . . 4c

5a Net gain or loss from disposition of property (see instructions) . 5a

b Net gain or loss from disposition of property that is not subject to

net investment income tax (see instructions) . . . . . . . 5b

c Adjustment from disposition of partnership interest or S corporation

stock (see instructions) . . . . . . . . . . . . . . 5c

d Combine lines 5a through 5c . . . . . . . . . . . . . . . . . . . . . . 5d

6 Adjustments to investment income for certain CFCs and PFICs (see instructions) . . . . . 6

7 Other modifications to investment income (see instructions) . . . . . . . . . . . . 7

8 Total investment income. Combine lines 1, 2, 3, 4c, 5d, 6, and 7 . . . . . . . . . . . 8

Part II Investment Expenses Allocable to Investment Income and Modifications

9a Investment interest expenses (see instructions) . . . . . . 9a

b State, local, and foreign income tax (see instructions) . . . . 9b

c Miscellaneous investment expenses (see instructions) . . . . 9c

d Add lines 9a, 9b, and 9c . . . . . . . . . . . . . . . . . . . . . . . . 9d

10 Additional modifications (see instructions) . . . . . . . . . . . . . . . . . . 10

11 Total deductions and modifications. Add lines 9d and 10 . . . . . . . . . . . . . 11

Part III Tax Computation

12 Net investment income. Subtract Part II, line 11 from Part I, line 8. Individuals complete lines 13–

17. Estates and trusts complete lines 18a–21. If zero or less, enter -0- . . . . . . . . . 12

Individuals:

13 Modified adjusted gross income (see instructions) . . . . . 13

14 Threshold based on filing status (see instructions) . . . . . 14

15 Subtract line 14 from line 13. If zero or less, enter -0- . . . . 15

16 Enter the smaller of line 12 or line 15 . . . . . . . . . . . . . . . . . . . . 16

17 Net investment income tax for individuals. Multiply line 16 by 3.8% (.038). Enter here and

includ ...

Partnership Business Profits Tax Return

This document provides line-by-line instructions for completing the New Hampshire Department of Revenue Administration Form NH-1065, Partnership Business Profits Tax Return. It explains how to report income, deductions, additions, apportionment, credits, and calculations for determining the partnership's business profits tax liability. Key items include reporting income and deductions from the federal Form 1065, adding back certain taxes and expenses, deducting a net operating loss or interest income, apportioning income between in-state and out-of-state, and claiming available tax credits.

Form 1118 (Rev. December 2020)Department of the Treasury

Form 1118

(Rev. December 2020)

Department of the Treasury

Internal Revenue Service

Foreign Tax Credit—Corporations

▶ Attach to the corporation’s tax return.

▶ Go to www.irs.gov/Form1118 for instructions and the latest information.

For calendar year 20 , or other tax year beginning , 20 , and ending , 20

OMB No. 1545-0123

Attachment

Sequence No. 118

Name of corporation Employer identification number

Use a separate Form 1118 for each applicable category of income (see instructions).

a Separate Category (Enter code—see instructions.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ▶

b If code 901j is entered on line a, enter the country code for the sanctioned country (see instructions) . . . . . . . . . . . . . . ▶

c If one of the RBT codes is entered on line a, enter the country code for the treaty country (see instructions) . . . . . . . . . . . . ▶

Schedule A Income or (Loss) Before Adjustments (Report all amounts in U.S. dollars. See Specific Instructions.)

1. EIN or Reference ID

Number

(see instructions)*

2. Foreign Country or

U.S. Possession

(enter two-letter code—use

a separate line for each)

(see instructions)

Gross Income or (Loss) From Sources Outside the United States

3. Inclusions Under Sections 951(a)(1) and 951A

(see instructions)

4. Dividends

(see instructions) 5. Interest

(a) Exclude Gross-Up (b) Gross-Up (section 78) (a) Exclude Gross-Up (b) Gross-Up (section 78)

A

B

C

Totals (add lines A through C) . . . . . . . ▶

6. Gross Rents, Royalties,

and License Fees

7. Sales

8. Gross Income From

Performance of Services

9. Section 986(c) Gain 10. Section 987 Gain 11. Section 988 Gain

12. Other

(attach schedule)

A

B

C

Totals

13. Total

(add columns 3(a)

through 12)

14. Allocable Deductions

(a) Dividends

Received Deduction

(see instructions)

(b) Deduction Allowed Under

Section 250(a)(1)(A)—Foreign

Derived Intangible Income

(c) Deduction Allowed Under

Section 250(a)(1)(B)—Global

Intangible Low-Taxed Income

Rental, Royalty, and Licensing Expenses

(d) Depreciation, Depletion,

and Amortization

(e) Other Allocable

Expenses

(f) Expenses Allocable

to Sales Income

A

B

C

Totals

14. Allocable Deductions (continued)

(g) Expenses Allocable

to Gross Income From

Performance of Services

(h) Other Allocable

Deductions (attach schedule)

(see instructions)

(i) Total Allocable Deductions

(add columns 14(a)

through 14(h))

15. Apportioned

Share of Deductions

(enter amount from

applicable line of Schedule H,

Part II, column (d))

16. Net Operating

Loss Deduction

17. Total Deductions

(add columns 14(i)

through 16)

18. Total Income or (Loss)

Before Adjustments

(subtract column 17

from column 13)

A

B

C

Totals

* For section 863(b) income, NOLs, income from RICs, high-taxed income, section 965, section 951A, and reattribution of income by reason of disregarded payments, use a s ...

Schedule R Non-Corporate Gross Business Profits Reconciliation

This document is a form from the New Hampshire Department of Revenue Administration for reconciling a business's federal income calculations to New Hampshire's standards. It contains instructions for reconciling differences in depreciation deductions and asset sales prices due to changes in the Internal Revenue Code. The form has business owners adjust their federal income by adding back depreciation deductions and losses not allowed in NH and subtracting allowable deductions to determine their adjusted gross business profits for NH tax purposes.

Gl test without answers

This document provides a 60 question mock test on SAP FI (Financial Accounting) concepts. The questions cover a range of topics including basic settings, master data, document control, posting control, clearing, cash journal, and special GL transactions. Correct answers are awarded points ranging from 1 to 0.125 based on the number of true/false options in the question. An overall percentage score can be calculated by multiplying the total points by 1.66.

The 6-page US income tax form for non residents that boxing champ Manny Pacqu...

Certain cash contributions for Haiti relief made between January 11, 2010 and March 1, 2010 can be deducted on the taxpayer's 2009 tax return rather than their 2010 return. The contributions must have been made to qualified relief organizations to aid victims of the January 12, 2010 earthquake in Haiti. Acceptable forms of contributions include cash, checks, credit cards, debit cards, and cell phone contributions. The taxpayer must itemize deductions to claim this charitable deduction.

Bookmakers' return - general betting duty by Keyconsulting UK

This document is a betting duty return form for a bookmaker to report betting transactions and calculate duty owed for a specific accounting period. It includes instructions for bookmakers to report the aggregate amounts paid out as winnings, net stake receipts, any carried forward losses from previous periods, and to calculate the duty due. It provides the deadline to submit the completed form and payment to HMRC, and payment options including electronically or by cheque.

Schedules A, B and C

This document appears to be part of a New Jersey state tax return form (NJ-1040).

Schedule A allows the taxpayer to claim a credit for income taxes paid to other jurisdictions on the same income being taxed by New Jersey. The taxpayer must provide the name of the other jurisdiction and the amount of income taxed.

Schedule B requires the taxpayer to report any capital gains or losses from the sale of property. Information about the type of property sold, date acquired and sold, sale price, and gain/loss must be included.

Schedule C requires reporting of any rental income or losses, as well as income from royalties, patents, and copyrights as was reported on the federal tax return.

Vendor downpayment process mapping with EHP4 enhanced functionality

Vendor downpayment process mapping with EHP4 enhanced functionalitySubhrajyoti (Subhra) Bhattacharjee

The document outlines the steps to configure and process vendor down payments in SAP. It includes setting up required G/L accounts and configuration, creating a purchase order with a down payment, generating the down payment request, posting the down payment, clearing the down payment against an invoice receipt, and the related financial postings.2013 Form 990

The document is a letter from Guillermo Soria of Soria Inc. to NOWCastSA regarding their 2013 Form 990 tax return. It states that Soria Inc. has electronically filed NOWCastSA's 2013 Form 990 return for the tax year ending December 31, 2013. It thanks NOWCastSA for the opportunity to serve them and offers to answer any questions about the return. There is no fee charged for the tax preparation services.

Guide to File GSTR 9C

The document provides guidance on filing Form GSTR 9C for reconciliation of annual financial statements with annual returns. It explains the various parts of the form including basic details, reconciliation of gross and taxable turnover, input tax credit, auditor recommendations, and certification. Key points covered are reconciling turnover, taxes paid, input tax credit between financials and returns, reasons for differences, and certifications required by the auditor. The document provides line items to be captured in each part along with explanatory notes to aid completion of the form.

Form 1065-B-U.S. Return of Income for Electing Large Partnerships

This 3 sentence summary provides an overview of the key information from the document:

The document is an IRS Form 1065 for the year 2008 that provides tax information for an electing large partnership, including the partnership's principal business activity, total assets, income and deductions, resulting tax amount, and a declaration that the form is complete and accurate to the best of the knowledge of the person signing. The form includes sections to report the partnership's income from passive loss limitation activities, payments made including tax amounts and refunds, and signatures for the person preparing the form.

15-Cost Basis-0039_Cost Basis Brochure Revisions 12.15

The document discusses changes to Forms 1099 due to fixed income cost basis legislation. Key points:

1) New regulations require brokers to report additional tax information to the IRS for covered fixed income securities, like bond premiums and market discounts. This led to changes in how information is reported on Forms 1099-INT, 1099-OID, and 1099-B.

2) Form 1099-INT now consolidates more types of interest income and includes lines to break down bond premium amounts by security type. Form 1099-OID now has separate forms for each tax lot. Form 1099-B includes market discount amounts.

3) For noncovered securities, brokers report cost basis information

Tax Form Changes for 2015

The IRS makes small changes to many of their tax forms every year. The changes may just entail a box here or a line there, but all kinds of speculation - and wagering - precede the release of the changes. Here are the forms that have changed.

Spread betting return by Keyconsulting UK

This document is a betting duty return form that must be completed and submitted to HMRC along with any payment owed no later than 15 days after the end of the accounting period. The form requires information about spread bets placed and winnings paid out to calculate the duty owed. It includes notes to guide completion of the form and boxes for financial details, losses carried over, duty calculation, and a total amount due.

B-0301This chapter introduces important concepts in income measure.docx

B-0301This chapter introduces important concepts in income measurement. Accountants oftentimes discuss these concepts using accounting "jargon" or "terminology. Effective business communication requires that all parties attach the same meaning to the words that are used to express concepts. Match the accounting terms in the list on the left to the accounting concept described in the list on the right.(1)Depreciation(a)The basic conditions require that an exchange has occurred and the earnings process is complete.(2)Calendar Year(b)An asset reflecting advance payment for something that will be consumed over the future.(3)Revenue Recognition(c)An entry usually prepared coincident with the end of an accounting period to update the accounting for prepaids, accruals, and other allocations.(4)Cash Basis(d)An annual reporting period that runs from January 1 through December 31.(5)Prepaids(e)Monies collected from customers for services that have not yet been provided.(6)Unearned Revenue(f)An approach that results in the initial recording of prepaids to an asset account and unearned revenues to a liability account.(7)Balance Sheet Approach(g)The notion that a continuous business process can be divided into time intervals such as years, quarters, or months for reporting purposes.(8)Adjusting Entry(h)A systematic and rational allocation scheme to spread a portion of the total cost of a productive asset to each period of use.(9)Accruals(i)Expenses and revenues that gradually accumulate with the passage of time.(10)Periodicity Assumption(j)A simplified non-GAAP based method to record revenues as received and expenses as paid.

&R&"Myriad Web Pro,Bold"&20B-03.01

B-03.01

Worksheet(1)Depreciation(h)A systematic and rational allocation scheme to spread a portion of the total cost of a productive asset to each period of use.(2)Calendar Year(3)Revenue Recognition(4)Cash Basis(5)Prepaids(6)Unearned Revenue(7)Balance Sheet Approach(8)Adjusting Entry(9)Accruals(10)Periodicity Assumption

&L&"Myriad Web Pro,Bold"&12Name:

Date: Section: &R&"Myriad Web Pro,Bold"&20B-03.01

B-03.01

B-03.02Accounting "failures" occur when reported results are not presented in accordance with generally accepted accounting principles. These failures can produce significant financial losses to investors and creditors. Oftentimes, an accounting failure results from an incorrect application of revenue recognition concepts. Revgression Corporation included each of the following described transactions in revenue during 20X5. Three of these transactions were appropriate, and three were not. Determine which are "ok" and which are "not ok."(1)Goods were sold and shipped in late 20X5, but the product still requires substantial installation and setup services. The price and terms of sale stipulate that seller must satisfactorily complete all installation and setup at the buyer's location.(2)Goods were produced according to a customer purchase order, but had not y ...

New Jersey Gross Income Tax Domestic Production Activities Deduction

This document provides instructions for completing Form 501-GIT to calculate the New Jersey Domestic Production Activities Deduction. It explains that New Jersey has uncoupled from many provisions of IRC Section 199 and outlines what types of qualified production property and activities are eligible for the deduction. The form is used to determine the deduction amount that can be applied against net profits, income, gains, or distributions from various business entities and activities for New Jersey gross income tax purposes.

Comparative study of form 3 cd

1) The document provides a comparative study of the old Form 3CD (Tax Audit Report) and the new revised Form 3CD.

2) Key changes in the new form include additional clauses requiring disclosure of indirect tax registration numbers, section under which audit is conducted, and details of property transfers below stamp valuation.

3) The new form also requires more detailed disclosure of changes in accounting methods, deviations from accounting standards, contributions to employee funds, and inadmissible expenditure under sections 40(a) and 40(b).

297 clearchanne

Clear Channel Communications filed a Form 8-K to revise its 2007 Form 10-K to reclassify certain radio stations from discontinued operations to continuing operations based on a change in plans to sell those stations. The reclassification impacts selected financial data, management's discussion and analysis, financial statements, and related exhibits for all periods presented in the 2007 Form 10-K. Specifically, it reclassifies the assets, results of operations and cash flows of 145 radio stations that were previously classified as discontinued operations. This reclassification has no impact on the company's previously reported net income.

Cryptocurrency Taxes Explained [Updated 2020]!

Our team at BearTax has put together this presentation to help traders and investors understand the basics of accounting and taxation of cryptocurrency. For more questions & discussions, join our telegram group https://t.me/beartax and visit out website https://bear.tax

Feel free to share around. Link us if you make a copy of it in your presentation.

Human's Guide to Cryptocurrency Taxes

To calculate cryptocurrency taxes, you must first consolidate all trades from exchanges into one place and match sell transactions with buy transactions using the first-in first-out method to determine gains or losses. You must also link any wallets for mining transactions or generated coins sold during the tax year, and properly account for any transfers between exchanges. Once gains and losses are determined, the details must be added to the necessary tax forms.

More Related Content

Similar to Sample 8949 Document BearTax

Form 1040Form 1040 Department of the Treasury Internal Revenue Ser.docx

Form 1040Form 1040 Department of the Treasury Internal Revenue Service2013U.S. Individual Tax FormOMB No.1545-0074IRS Use Only--Do not write or staple in this spaceFor the year Jan.1--Dec. 31,2013, or any other tax year beginning,2013,,20See Separate InstructionsYour first name and initialLast nameSocial Security NumberIf a joint return, spouses first name and initialLast nameSpouse Social Security NumberHome address( number and street). If you have a P.O. Box, see instructionsMake Sure that the SSN(s) above and on line 6c are correct.City, town, or post office, state, and zip code. If you have a foreign address, also complete spaces below (see instructions).Presidential Election CampaignCheck here if you, or your spouse if filing jointly,Foreign country nameForeign province/state/countryForeign postal codechecking this box below will not change your taxrefund.youspouseFiling Status1. Single4.Head of Household (with qualifying person.) (See instructions.) IfCheck only one box2.. married filing jointlythe qualifying person is a child but not your dependent, enter this3. Married filing separately. Enter spouse's SSN abovechild's name hereand full name here.5. Qualifying Window(er) with dependent childExemptions6a Yourself. If someone can claim you as a dependent, do not check box 6a]Boxes checkedb spouse]on 6a and 6bIf more than fourc. Dependentsdependents, see(1) First nameLast name(2) dependents(3) dependents (4) check if child under age 17No. of childreninstructions and social security numberrelationship to youqualifying for tax credit seeon 6c who:check hereinstructions.lived with youdid not live with youdue to divorce orseparation(see instructions)Dependents on6c not entered aboved. Total number of Exemptions ClaimedAdd numbers on lines aboveIncome7Wages, salaries, tips, etc. Attach Forms (W-2)78aTaxable interest. Attach Schedule B if required8aAttach Form(s)bTax-exempt interest. Do not include on line 8a8bW-2 here. Also9aOrdinary dividends. Attach Schedule B if required9aattach Forms(s) bQualified dividends9bW-2 and 1099-R10Taxable refunds, credits, or offsets state or local income taxes10if tax was withheld.11Alimony received1112Business income or (loss). Attach Schedule C or C-EZ12If you did not 13Capital gain or (loss). Attach Schedule D if required. If not required, check here13get a W-2,14other gains or (losses). Attach Form 479714see instructions15aIRA distributions15ab Taxable amount15b16aPensions and annuities16ab Taxable amount16b17Rental real estate, royalties, partnerships, S corporations, trusts, etc. Attach Schedule E1718Farm income or (loss). Attach Schedule F1819Unemployment compensation1920aSocial security benefits20ab Taxable amount20b21other income. List type and amount2122combine the amounts in the far right column for lines 7 through 21. This is your total incomeThis is your total income.22Adjusted 23Educator expenses23Gross24Certain business expenses of reservists, performing artists, and fee-basis government. Atta ...

Form 8960Department of the Treasury Internal Revenue Serv.docx

Form 8960

Department of the Treasury

Internal Revenue Service (99)

Net Investment Income Tax—

Individuals, Estates, and Trusts

▶ Attach to your tax return.

▶ Information about Form 8960 and its separate instructions is at www.irs.gov/form8960.

OMB No. 1545-2227

2016

Attachment

Sequence No. 72

Name(s) shown on your tax return Your social security number or EIN

Part I Investment Income Section 6013(g) election (see instructions)

Section 6013(h) election (see instructions)

Regulations section 1.1411-10(g) election (see instructions)

1 Taxable interest (see instructions) . . . . . . . . . . . . . . . . . . . . . 1

2 Ordinary dividends (see instructions) . . . . . . . . . . . . . . . . . . . . 2

3 Annuities (see instructions) . . . . . . . . . . . . . . . . . . . . . . . 3

4a Rental real estate, royalties, partnerships, S corporations, trusts,

etc. (see instructions) . . . . . . . . . . . . . . . 4a

b Adjustment for net income or loss derived in the ordinary course of

a non-section 1411 trade or business (see instructions) . . . . 4b

c Combine lines 4a and 4b . . . . . . . . . . . . . . . . . . . . . . . . 4c

5a Net gain or loss from disposition of property (see instructions) . 5a

b Net gain or loss from disposition of property that is not subject to

net investment income tax (see instructions) . . . . . . . 5b

c Adjustment from disposition of partnership interest or S corporation

stock (see instructions) . . . . . . . . . . . . . . 5c

d Combine lines 5a through 5c . . . . . . . . . . . . . . . . . . . . . . 5d

6 Adjustments to investment income for certain CFCs and PFICs (see instructions) . . . . . 6

7 Other modifications to investment income (see instructions) . . . . . . . . . . . . 7

8 Total investment income. Combine lines 1, 2, 3, 4c, 5d, 6, and 7 . . . . . . . . . . . 8

Part II Investment Expenses Allocable to Investment Income and Modifications

9a Investment interest expenses (see instructions) . . . . . . 9a

b State, local, and foreign income tax (see instructions) . . . . 9b

c Miscellaneous investment expenses (see instructions) . . . . 9c

d Add lines 9a, 9b, and 9c . . . . . . . . . . . . . . . . . . . . . . . . 9d

10 Additional modifications (see instructions) . . . . . . . . . . . . . . . . . . 10

11 Total deductions and modifications. Add lines 9d and 10 . . . . . . . . . . . . . 11

Part III Tax Computation

12 Net investment income. Subtract Part II, line 11 from Part I, line 8. Individuals complete lines 13–

17. Estates and trusts complete lines 18a–21. If zero or less, enter -0- . . . . . . . . . 12

Individuals:

13 Modified adjusted gross income (see instructions) . . . . . 13

14 Threshold based on filing status (see instructions) . . . . . 14

15 Subtract line 14 from line 13. If zero or less, enter -0- . . . . 15

16 Enter the smaller of line 12 or line 15 . . . . . . . . . . . . . . . . . . . . 16

17 Net investment income tax for individuals. Multiply line 16 by 3.8% (.038). Enter here and

includ ...

Partnership Business Profits Tax Return

This document provides line-by-line instructions for completing the New Hampshire Department of Revenue Administration Form NH-1065, Partnership Business Profits Tax Return. It explains how to report income, deductions, additions, apportionment, credits, and calculations for determining the partnership's business profits tax liability. Key items include reporting income and deductions from the federal Form 1065, adding back certain taxes and expenses, deducting a net operating loss or interest income, apportioning income between in-state and out-of-state, and claiming available tax credits.

Form 1118 (Rev. December 2020)Department of the Treasury

Form 1118

(Rev. December 2020)

Department of the Treasury

Internal Revenue Service

Foreign Tax Credit—Corporations

▶ Attach to the corporation’s tax return.

▶ Go to www.irs.gov/Form1118 for instructions and the latest information.

For calendar year 20 , or other tax year beginning , 20 , and ending , 20

OMB No. 1545-0123

Attachment

Sequence No. 118

Name of corporation Employer identification number

Use a separate Form 1118 for each applicable category of income (see instructions).

a Separate Category (Enter code—see instructions.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ▶

b If code 901j is entered on line a, enter the country code for the sanctioned country (see instructions) . . . . . . . . . . . . . . ▶

c If one of the RBT codes is entered on line a, enter the country code for the treaty country (see instructions) . . . . . . . . . . . . ▶

Schedule A Income or (Loss) Before Adjustments (Report all amounts in U.S. dollars. See Specific Instructions.)

1. EIN or Reference ID

Number

(see instructions)*

2. Foreign Country or

U.S. Possession

(enter two-letter code—use

a separate line for each)

(see instructions)

Gross Income or (Loss) From Sources Outside the United States

3. Inclusions Under Sections 951(a)(1) and 951A

(see instructions)

4. Dividends

(see instructions) 5. Interest

(a) Exclude Gross-Up (b) Gross-Up (section 78) (a) Exclude Gross-Up (b) Gross-Up (section 78)

A

B

C

Totals (add lines A through C) . . . . . . . ▶

6. Gross Rents, Royalties,

and License Fees

7. Sales

8. Gross Income From

Performance of Services

9. Section 986(c) Gain 10. Section 987 Gain 11. Section 988 Gain

12. Other

(attach schedule)

A

B

C

Totals

13. Total

(add columns 3(a)

through 12)

14. Allocable Deductions

(a) Dividends

Received Deduction

(see instructions)

(b) Deduction Allowed Under

Section 250(a)(1)(A)—Foreign

Derived Intangible Income

(c) Deduction Allowed Under

Section 250(a)(1)(B)—Global

Intangible Low-Taxed Income

Rental, Royalty, and Licensing Expenses

(d) Depreciation, Depletion,

and Amortization

(e) Other Allocable

Expenses

(f) Expenses Allocable

to Sales Income

A

B

C

Totals

14. Allocable Deductions (continued)

(g) Expenses Allocable

to Gross Income From

Performance of Services

(h) Other Allocable

Deductions (attach schedule)

(see instructions)

(i) Total Allocable Deductions

(add columns 14(a)

through 14(h))

15. Apportioned

Share of Deductions

(enter amount from

applicable line of Schedule H,

Part II, column (d))

16. Net Operating

Loss Deduction

17. Total Deductions

(add columns 14(i)

through 16)

18. Total Income or (Loss)

Before Adjustments

(subtract column 17

from column 13)

A

B

C

Totals

* For section 863(b) income, NOLs, income from RICs, high-taxed income, section 965, section 951A, and reattribution of income by reason of disregarded payments, use a s ...

Schedule R Non-Corporate Gross Business Profits Reconciliation

This document is a form from the New Hampshire Department of Revenue Administration for reconciling a business's federal income calculations to New Hampshire's standards. It contains instructions for reconciling differences in depreciation deductions and asset sales prices due to changes in the Internal Revenue Code. The form has business owners adjust their federal income by adding back depreciation deductions and losses not allowed in NH and subtracting allowable deductions to determine their adjusted gross business profits for NH tax purposes.

Gl test without answers

This document provides a 60 question mock test on SAP FI (Financial Accounting) concepts. The questions cover a range of topics including basic settings, master data, document control, posting control, clearing, cash journal, and special GL transactions. Correct answers are awarded points ranging from 1 to 0.125 based on the number of true/false options in the question. An overall percentage score can be calculated by multiplying the total points by 1.66.

The 6-page US income tax form for non residents that boxing champ Manny Pacqu...

Certain cash contributions for Haiti relief made between January 11, 2010 and March 1, 2010 can be deducted on the taxpayer's 2009 tax return rather than their 2010 return. The contributions must have been made to qualified relief organizations to aid victims of the January 12, 2010 earthquake in Haiti. Acceptable forms of contributions include cash, checks, credit cards, debit cards, and cell phone contributions. The taxpayer must itemize deductions to claim this charitable deduction.

Bookmakers' return - general betting duty by Keyconsulting UK

This document is a betting duty return form for a bookmaker to report betting transactions and calculate duty owed for a specific accounting period. It includes instructions for bookmakers to report the aggregate amounts paid out as winnings, net stake receipts, any carried forward losses from previous periods, and to calculate the duty due. It provides the deadline to submit the completed form and payment to HMRC, and payment options including electronically or by cheque.

Schedules A, B and C

This document appears to be part of a New Jersey state tax return form (NJ-1040).

Schedule A allows the taxpayer to claim a credit for income taxes paid to other jurisdictions on the same income being taxed by New Jersey. The taxpayer must provide the name of the other jurisdiction and the amount of income taxed.

Schedule B requires the taxpayer to report any capital gains or losses from the sale of property. Information about the type of property sold, date acquired and sold, sale price, and gain/loss must be included.

Schedule C requires reporting of any rental income or losses, as well as income from royalties, patents, and copyrights as was reported on the federal tax return.

Vendor downpayment process mapping with EHP4 enhanced functionality

Vendor downpayment process mapping with EHP4 enhanced functionalitySubhrajyoti (Subhra) Bhattacharjee

The document outlines the steps to configure and process vendor down payments in SAP. It includes setting up required G/L accounts and configuration, creating a purchase order with a down payment, generating the down payment request, posting the down payment, clearing the down payment against an invoice receipt, and the related financial postings.2013 Form 990

The document is a letter from Guillermo Soria of Soria Inc. to NOWCastSA regarding their 2013 Form 990 tax return. It states that Soria Inc. has electronically filed NOWCastSA's 2013 Form 990 return for the tax year ending December 31, 2013. It thanks NOWCastSA for the opportunity to serve them and offers to answer any questions about the return. There is no fee charged for the tax preparation services.

Guide to File GSTR 9C

The document provides guidance on filing Form GSTR 9C for reconciliation of annual financial statements with annual returns. It explains the various parts of the form including basic details, reconciliation of gross and taxable turnover, input tax credit, auditor recommendations, and certification. Key points covered are reconciling turnover, taxes paid, input tax credit between financials and returns, reasons for differences, and certifications required by the auditor. The document provides line items to be captured in each part along with explanatory notes to aid completion of the form.

Form 1065-B-U.S. Return of Income for Electing Large Partnerships

This 3 sentence summary provides an overview of the key information from the document:

The document is an IRS Form 1065 for the year 2008 that provides tax information for an electing large partnership, including the partnership's principal business activity, total assets, income and deductions, resulting tax amount, and a declaration that the form is complete and accurate to the best of the knowledge of the person signing. The form includes sections to report the partnership's income from passive loss limitation activities, payments made including tax amounts and refunds, and signatures for the person preparing the form.

15-Cost Basis-0039_Cost Basis Brochure Revisions 12.15

The document discusses changes to Forms 1099 due to fixed income cost basis legislation. Key points:

1) New regulations require brokers to report additional tax information to the IRS for covered fixed income securities, like bond premiums and market discounts. This led to changes in how information is reported on Forms 1099-INT, 1099-OID, and 1099-B.

2) Form 1099-INT now consolidates more types of interest income and includes lines to break down bond premium amounts by security type. Form 1099-OID now has separate forms for each tax lot. Form 1099-B includes market discount amounts.

3) For noncovered securities, brokers report cost basis information

Tax Form Changes for 2015

The IRS makes small changes to many of their tax forms every year. The changes may just entail a box here or a line there, but all kinds of speculation - and wagering - precede the release of the changes. Here are the forms that have changed.

Spread betting return by Keyconsulting UK

This document is a betting duty return form that must be completed and submitted to HMRC along with any payment owed no later than 15 days after the end of the accounting period. The form requires information about spread bets placed and winnings paid out to calculate the duty owed. It includes notes to guide completion of the form and boxes for financial details, losses carried over, duty calculation, and a total amount due.

B-0301This chapter introduces important concepts in income measure.docx

B-0301This chapter introduces important concepts in income measurement. Accountants oftentimes discuss these concepts using accounting "jargon" or "terminology. Effective business communication requires that all parties attach the same meaning to the words that are used to express concepts. Match the accounting terms in the list on the left to the accounting concept described in the list on the right.(1)Depreciation(a)The basic conditions require that an exchange has occurred and the earnings process is complete.(2)Calendar Year(b)An asset reflecting advance payment for something that will be consumed over the future.(3)Revenue Recognition(c)An entry usually prepared coincident with the end of an accounting period to update the accounting for prepaids, accruals, and other allocations.(4)Cash Basis(d)An annual reporting period that runs from January 1 through December 31.(5)Prepaids(e)Monies collected from customers for services that have not yet been provided.(6)Unearned Revenue(f)An approach that results in the initial recording of prepaids to an asset account and unearned revenues to a liability account.(7)Balance Sheet Approach(g)The notion that a continuous business process can be divided into time intervals such as years, quarters, or months for reporting purposes.(8)Adjusting Entry(h)A systematic and rational allocation scheme to spread a portion of the total cost of a productive asset to each period of use.(9)Accruals(i)Expenses and revenues that gradually accumulate with the passage of time.(10)Periodicity Assumption(j)A simplified non-GAAP based method to record revenues as received and expenses as paid.

&R&"Myriad Web Pro,Bold"&20B-03.01

B-03.01

Worksheet(1)Depreciation(h)A systematic and rational allocation scheme to spread a portion of the total cost of a productive asset to each period of use.(2)Calendar Year(3)Revenue Recognition(4)Cash Basis(5)Prepaids(6)Unearned Revenue(7)Balance Sheet Approach(8)Adjusting Entry(9)Accruals(10)Periodicity Assumption

&L&"Myriad Web Pro,Bold"&12Name:

Date: Section: &R&"Myriad Web Pro,Bold"&20B-03.01

B-03.01

B-03.02Accounting "failures" occur when reported results are not presented in accordance with generally accepted accounting principles. These failures can produce significant financial losses to investors and creditors. Oftentimes, an accounting failure results from an incorrect application of revenue recognition concepts. Revgression Corporation included each of the following described transactions in revenue during 20X5. Three of these transactions were appropriate, and three were not. Determine which are "ok" and which are "not ok."(1)Goods were sold and shipped in late 20X5, but the product still requires substantial installation and setup services. The price and terms of sale stipulate that seller must satisfactorily complete all installation and setup at the buyer's location.(2)Goods were produced according to a customer purchase order, but had not y ...

New Jersey Gross Income Tax Domestic Production Activities Deduction

This document provides instructions for completing Form 501-GIT to calculate the New Jersey Domestic Production Activities Deduction. It explains that New Jersey has uncoupled from many provisions of IRC Section 199 and outlines what types of qualified production property and activities are eligible for the deduction. The form is used to determine the deduction amount that can be applied against net profits, income, gains, or distributions from various business entities and activities for New Jersey gross income tax purposes.

Comparative study of form 3 cd

1) The document provides a comparative study of the old Form 3CD (Tax Audit Report) and the new revised Form 3CD.

2) Key changes in the new form include additional clauses requiring disclosure of indirect tax registration numbers, section under which audit is conducted, and details of property transfers below stamp valuation.

3) The new form also requires more detailed disclosure of changes in accounting methods, deviations from accounting standards, contributions to employee funds, and inadmissible expenditure under sections 40(a) and 40(b).

297 clearchanne

Clear Channel Communications filed a Form 8-K to revise its 2007 Form 10-K to reclassify certain radio stations from discontinued operations to continuing operations based on a change in plans to sell those stations. The reclassification impacts selected financial data, management's discussion and analysis, financial statements, and related exhibits for all periods presented in the 2007 Form 10-K. Specifically, it reclassifies the assets, results of operations and cash flows of 145 radio stations that were previously classified as discontinued operations. This reclassification has no impact on the company's previously reported net income.

Similar to Sample 8949 Document BearTax (20)

Form 1040Form 1040 Department of the Treasury Internal Revenue Ser.docx

Form 1040Form 1040 Department of the Treasury Internal Revenue Ser.docx

Form 8960Department of the Treasury Internal Revenue Serv.docx

Form 8960Department of the Treasury Internal Revenue Serv.docx

Form 1118 (Rev. December 2020)Department of the Treasury

Form 1118 (Rev. December 2020)Department of the Treasury

Schedule R Non-Corporate Gross Business Profits Reconciliation

Schedule R Non-Corporate Gross Business Profits Reconciliation

The 6-page US income tax form for non residents that boxing champ Manny Pacqu...

The 6-page US income tax form for non residents that boxing champ Manny Pacqu...

Bookmakers' return - general betting duty by Keyconsulting UK

Bookmakers' return - general betting duty by Keyconsulting UK

Vendor downpayment process mapping with EHP4 enhanced functionality

Vendor downpayment process mapping with EHP4 enhanced functionality

Form 1065-B-U.S. Return of Income for Electing Large Partnerships

Form 1065-B-U.S. Return of Income for Electing Large Partnerships

15-Cost Basis-0039_Cost Basis Brochure Revisions 12.15

15-Cost Basis-0039_Cost Basis Brochure Revisions 12.15

B-0301This chapter introduces important concepts in income measure.docx

B-0301This chapter introduces important concepts in income measure.docx

New Jersey Gross Income Tax Domestic Production Activities Deduction

New Jersey Gross Income Tax Domestic Production Activities Deduction

More from Vamshi Vangapally

Cryptocurrency Taxes Explained [Updated 2020]!

Our team at BearTax has put together this presentation to help traders and investors understand the basics of accounting and taxation of cryptocurrency. For more questions & discussions, join our telegram group https://t.me/beartax and visit out website https://bear.tax

Feel free to share around. Link us if you make a copy of it in your presentation.

Human's Guide to Cryptocurrency Taxes

To calculate cryptocurrency taxes, you must first consolidate all trades from exchanges into one place and match sell transactions with buy transactions using the first-in first-out method to determine gains or losses. You must also link any wallets for mining transactions or generated coins sold during the tax year, and properly account for any transfers between exchanges. Once gains and losses are determined, the details must be added to the necessary tax forms.

Break My Trip

This is a concept app which will help you find a route between two given locations. Specialty of this app is to break your itinerary into different modes of transportation to meet your budget and time constraints. You can do connected flights, connected flight n train or bus in between. Time and cost would be tradeoffs here. Check out the presentation to know more

Introduction to Mobile Business Intelligence

Mobile business intelligence (BI) is emerging as a trend where dashboards and reports are deployed onto mobile devices like smartphones and tablets. Traditional BI involved desktop access, but mobile BI allows for handheld and location-aware access on mobile devices. It is targeted for use cases like paperless reporting and store managers accessing dynamic data and dashboards via built-in GPS on mobile devices.

Twitter Search

This document provides information about a new user friendly Chrome extension called TwittSearch that allows searching through tweets. It has a brief description section and notes there is a contact provided to reach the developer to discuss the extension further.

No sql databases

This document provides an overview of NoSQL databases. It discusses how NoSQL databases were developed to handle the massive amounts of data and requests on the internet. It describes the different types of NoSQL databases and how they are useful for web applications and situations that don't require strict ACID properties. The document also covers some of the tradeoffs of NoSQL databases compared to relational databases and some of the challenges in using NoSQL databases.

Auto Categorization of twitter Users

The document proposes a solution to automatically categorize a Twitter user's friends based on the content of their tweets. It involves retrieving tweets from each friend, extracting relevant words, and calculating a score for how likely each friend belongs to different categories like Technology, News, Music, or Science based on the probability of the extracted words occurring in tweets from that category. The friend would then be categorized into the list with the highest score.

Networks in their surrounding contexts

Simplified slides of content in chapter 4 titled "Networks in their surrounding contexts" related to information networks.

More from Vamshi Vangapally (8)

Recently uploaded

How our Rebranding Succeeds in Instilling trust in Every Agri Citizen

Ninjacart recently rebranded to emphasize its mission of improving the lives of agri citizens, including farmers, traders, and retailers. The rebranding introduced affiliated brands NinjaMandi, NinjaGlobal, NinjaKirana, and NinjaKisan, expanding Ninjacart's offerings to credit and commerce. A new brand film honors the contributions of agri citizens, fostering pride and trust among customers. The updated logo symbolizes Ninjacart's commitment to unity and growth in the agri value chain. This transformation highlights Ninjacart’s evolution from a fulfilment-centric business to a comprehensive marketplace platform, aiming to build #BetterLives for all agri citizens.

Verified Call Girls Mumbai || +919920725232 || Quick Booking at Affordable Price

Verified Call Girls Mumbai || +919920725232 || Quick Booking at Affordable Price

How are Lilac French Bulldogs Beauty Charming the World and Capturing Hearts ...

After being the most listed dog breed in the United States for 31

years in a row, the Labrador Retriever has dropped to second place

in the American Kennel Club's annual survey of the country's most

popular canines. The French Bulldog is the new top dog in the

United States as of 2022. The stylish puppy has ascended the

rankings in rapid time despite having health concerns and limited

color choices.

Find herbal colors, organic colors, and non-toxic gulal wholesale supplier.pdf

Herbal colors, organic colors, and non-toxic gulal offer safer and more environmentally friendly alternatives to synthetic dyes. They are made from natural, organic, and non-toxic materials, making them gentle on the skin and less harmful to the environment. These colors are especially popular during cultural and religious festivals, in cosmetics, and in organic products.

Digital promotion service|Rohini digital marketing consultant|Coimbatore

ROHINI DIGITAL MARKETING CONSULTANT

Myself Rohini, a digital marketing consultant located in Coimbatore. I offer digital marketing promotion for your business requirements through digital marketing services (likely SEO, SEM,etc.) Since 2020 with best Quality and affordable price. Join with us to promote your business in assured in lead generation.

DIGITAL MARKETING

Digital marketing makes technologies and trends forced companies to change their marketing strategies and rethink their budget. Email become a popular marketing tool in the early days of digital marketing. In digital marketing according to your need products can be promote. The goal of digital marketing is to reach and engage with target audience, built brand awareness,lead generation etc.

IMPORTANT OF DIGITAL MARKETING

•Brand awareness is the most significant especially for newly establish business.

•Cost -effectiveness one of the most prominent advantage of digital marketing

•Digital marketing make people to know your business easy.

It promote your business in assured in lead generation..

ROHINI

MARKETING SERVICES:

•Search Engine Optimization.

•Search Engine Marketing.

•Social Media Optimization

•Social Media Marketing

•Campaigns(Sms,Email, Whatsapp Etc..)

BENEFITS OF ROHINI DIGITAL MARKETING CONSULTANT.

It allows you to track day to day campaign performances.

To promote business with fresh and innovative ideas.

To reach and engage with target audience..

•To promote service with affordable price.

With regards,

Rohini ,

Digital Marketer,

Coimbatore,

rohinidm94@gmail.com

The Impact of Team Sports on Social Skills Development.pdf

Explore how team sports contribute to social skills development and why they are an essential part of growing up.

9861615390 Satta Dpboss Sattamatka matka

9861615390 Satta Dpboss Sattamatka matkasattamatka dpboss matka satta Matka , Kalyan, Sattamatka, boss, dpboss, satta

9861615390 Satta Matka | Satta Matka Results | Kalyan Matka Tips | Free Matka Results | SattaMatka | Satta Matka Tips | Satta Matka Guessing | Satta Matka Number | Satta Matka 143 | Online All Satta Matka Result | Satta Matka Guessing | Satta Matka Chart | Satta Matka King | Satta Matka Trick | Satta Matka Tips | Satta Matka Number | Satta Matka Software | Matka Chart | Matka Result | Satta Matka Guessing | Kalyan Matka | Kalyan Matka Tips | Matka Result | Satta Matka Result | Satta Matka Tips | Satta Matka | Matka Tips | Satta King | Satta Game | Satta Result | Matka Result | Satta Matka Result | Satta Matka | Kalyan Matka | Kalyan Matka Tips | Matka Result | Satta Matka Result | Satta Matka Tips | Satta Matka | Matka Tips | Satta King | Satta Game | Satta Result | Matka Result | Satta Matka Result | Satta Matka | Kalyan Matka | Kalyan Matka Tips | Matka Result | Satta Matka Result | Satta Matka Tips | Satta Matka | Matka Tips | Satta King | Satta Game | Satta Result | Matka Result | Satta Matka Result | Satta Matka | Kalyan Matka | Kalyan Matka Tips | Matka Result | Satta Matka Result | Satta Matka Tips | Satta Matka | Matka Tips | Satta King | Satta Game | Satta Result | Matka Result | Satta Matka Result | Satta Matka | Kalyan Matka | Kalyan Matka Tips | Matka Result | Satta Matka Result | Satta Matka Tips | Satta Matka | Matka Tips | Satta King | Satta Game | Satta Result | Matka Result | Satta Matka Result | Satta Matka | Kalyan Matka | Kalyan Matka Tips | Matka Result | Satta Matka Result | Satta Matka Tips | Satta Matka | Matka Tips | Satta King | Satta Game | Satta Result | Matka Result | Satta Matka Result | Satta Matka | Kalyan Matka | Kalyan Matka Tips | Matka Result | Satta Matka Result | Satta Matka Tips | Satta Matka | Matka Tips | Satta King | Satta Game | Satta Result | Matka Result | Satta Matka Result | Satta Matka | Kalyan Matka | Kalyan Matka Tips | Matka Result | Satta Matka Result | Satta Matka Tips | Satta Matka | Matka Tips | Satta King | Satta Game | Satta Result | Matka Result | Satta Matka Result | Satta Matka | Kalyan Matka | Kalyan Matka Tips | Matka Result | Satta Matka Result | Satta Matka Tips | Satta Matka | Matka Tips | Satta King | Satta Game | Satta Result | Matka Result | Satta Matka Result | Satta Matka | Kalyan Matka | Kalyan Matka Tips | Matka Result | Satta Matka Result | Satta Matka Tips | Satta Matka | Matka Tips | Satta King | Satta Game | Satta Result | Matka Result | Satta Matka Result | Satta Matka | Kalyan Matka | Kalyan Matka Tips | Matka Result | Satta Matka Result | Satta Matka Tips | Satta Matka | Matka Tips | Satta King | Satta Game | Satta Result | Matka Result | Satta Matka Result | Satta Matka | Kalyan Matka | Kalyan Matka Tips | Matka Result | Satta Matka Result | Satta Matka Tips | Satta Matka | Matka Tips | Satta King | Satta Game | Satta Result | Matka Result | Satta Matka Result | Satta Matka | Kalyan Matka | Kalyan Matka Tips | Matka Result | Satta Matka Result | Satta Matka Tips Satta Matka Dpboss Kalyan Game Sattamatk

#MAIN MATKA #kalyantoday #matkaboss #matka420 #indiaMatka

#sattamattamatka143 #sattamatka

#indianMatka #kalyanchart #kalyanmatka

#kalyanjodichart #matkaguessing

#indianmatka #matkafixjodi

#KalyanJodiChart #KalyanPanelChart

#call-❾❸❹❽❺❾❼❾❾🅞︎

Findlay Evans Waterproofing with AIW - Article November 2017

Findlay Evans Waterproofing with AIW - Article November 2017MELBOURNE Commercial Waterproofers - Findlay-Evans Waterproofing

Advancing Waterproofing Expertise with AIW

Waterproofing Melbourne and beyond, the Australian Institute of Waterproofing (AIW) is proud to introduce an innovative commercial waterproofing course. Developed in collaboration with the Master Builders Association Vic, this course, led by Andrew Golle, is tailored for project managers overseeing balcony waterproofing, roof waterproofing, and concrete repair. Paul Evans emphasizes the critical nature of these roles in preventing costly post-construction issues. Private sessions for building supervisors are now available, addressing common mistakes due to poor applications and cost-cutting measures.

The course covers essential topics, including product selection, surface preparation, and the importance of basement waterproofing. Paul Evans highlights the recurring problems seen in the industry, where inadequate training and oversight lead to significant issues, from retaining wall waterproofing to lift pit waterproofing.

In response to these challenges, the AIW is developing a "Below Ground Waterproofing Standard" specific to Australia, inspired by UK standards. Paul Evans calls for industry-wide collaboration to ensure the standard encompasses diverse methods and materials, ultimately enhancing the quality and longevity of waterproofing work.

By equipping supervisors and builders with the right knowledge, AIW aims to improve the overall standard of waterproofing practices, reducing the risk of failures and the subsequent mental and financial stress on homeowners. This proactive approach is crucial for the sustainability and reliability of waterproofing in construction projects across Australia.Top Call Girls in Mumbai || +919920725232 || Quick Booking at Affordable Price

Top Call Girls in Mumbai || +919920725232 || Quick Booking at Affordable Price

sim owner details | +923099554040 | sim owner details pakistan

Whatsapp Number: +923099554040

sim owner details

sim owner details pakistan

nadra sim owner details

sim owner details by number

sim owner details online

sim owner details apk

sim owner details app

sim owner details online check pakistan

pak sim data sim owner details

zong sim owner details

check sim owner details

how to check sim owner details in pakistan

find sim owner details in pakistan

mobile sim owner details

how to check sim owner details

sim card owner details

sim card owner details online

sim owner details with name and address

track sim card owner details online

jio sim owner details

sim owner details software

check sim card owner details

find sim owner details

how to check airtel sim owner details

how to check sim card owner details

how to find a sim owner details

how to find sim owner details

how to know sim card owner details

how to know sim owner details

idea sim card owner details online

sim card owner details app

sim card owner details software

sim owner name details

ufone sim owner details

00923456435194 sim owner detail

ap to know the sim owners details

check sim number owner details

find out details of owner of sim card

finding sim registration owner details

full details of sim card owner pakistan

how to check my sim owner details

how to check owner detail through sim

how to check owner details of a sim

how to check owner details of jaz sim

how to check sim owner details who tease people

how to check sim owner name and detail warid

how to chek owner details of sim

how to find a sim owner details pakista

how to find a sim owner details pakistan

how to find sim card owner details in pakistan

how to get details of others sim owner in pakistan

how to trace a sim owner details pakistan

idea sim card owner details

iran sim details of owner

iran sim details of owner website

mobile phone number details sim owner name address

mobile phone number details sim owner name address location

online sim owner details.pakistan

pakistan prepaid sim owner details

pakistan sim owner details

phone number details sim owner name address location

search sim card owner and details using apk

sim card owner details app for pakistan

sim detail check online owner

sim details online by number owner name

sim number all details with owner name

sim number all details with owner name id card

sim owner call details online

sim owner details by contact number

sim owner details online with name and address

sim owner name full details

The Late Samuel Sekyere Safo-Ankoma Funeral Booklet

The Late Samuel Sekyere Safo-Ankoma Funeral Program.

High Tech Central Air Services. | HVAC Services New York

High Tech Central Air Services , specialize in all forms of commercial HVAC projects. We install, repair, and maintain commercial HVAC systems of any type. provides heating and air conditioning services within New York City, Manhattan, Queens, Brooklyn, Bronx, Staten Island, Long Island, New Jersey, Connecticut. Our PTAC services are second to none. If you are interested in any of our PTAC services, please give us a call to schedule an appointment. The number to call is (917) 310-0014. https://www.hightechcentralair.com #hvac #plumbing #airconditioning #cooling #hvaclife #plumber #heatingandcooling #hvacservice #furnace #ac #hvactechnician #boiler #hvactech #plumbinglife #heatingengineer #airconditioner #construction #maintenance #plumbers #hvacinstall #hvacrepair #home #service #boilers #refrigeration #heatingsystem #hvacr #gas #contractor #newyork

一比一原版(sfu毕业证书)西蒙菲莎大学毕业证如何办理

原版一模一样【微信:741003700 】【(sfu毕业证书)西蒙菲莎大学毕业证成绩单】【微信:741003700 】学位证,留信认证(真实可查,永久存档)原件一模一样纸张工艺/offer、雅思、外壳等材料/诚信可靠,可直接看成品样本,帮您解决无法毕业带来的各种难题!外壳,原版制作,诚信可靠,可直接看成品样本。行业标杆!精益求精,诚心合作,真诚制作!多年品质 ,按需精细制作,24小时接单,全套进口原装设备。十五年致力于帮助留学生解决难题,包您满意。

本公司拥有海外各大学样板无数,能完美还原。

1:1完美还原海外各大学毕业材料上的工艺:水印,阴影底纹,钢印LOGO烫金烫银,LOGO烫金烫银复合重叠。文字图案浮雕、激光镭射、紫外荧光、温感、复印防伪等防伪工艺。材料咨询办理、认证咨询办理请加学历顾问Q/微741003700

【主营项目】

一.毕业证【q微741003700】成绩单、使馆认证、教育部认证、雅思托福成绩单、学生卡等!

二.真实使馆公证(即留学回国人员证明,不成功不收费)

三.真实教育部学历学位认证(教育部存档!教育部留服网站永久可查)

四.办理各国各大学文凭(一对一专业服务,可全程监控跟踪进度)

如果您处于以下几种情况:

◇在校期间,因各种原因未能顺利毕业……拿不到官方毕业证【q/微741003700】

◇面对父母的压力,希望尽快拿到;

◇不清楚认证流程以及材料该如何准备;

◇回国时间很长,忘记办理;

◇回国马上就要找工作,办给用人单位看;

◇企事业单位必须要求办理的

◇需要报考公务员、购买免税车、落转户口

◇申请留学生创业基金

留信网认证的作用:

1:该专业认证可证明留学生真实身份

2:同时对留学生所学专业登记给予评定

3:国家专业人才认证中心颁发入库证书

4:这个认证书并且可以归档倒地方

5:凡事获得留信网入网的信息将会逐步更新到个人身份内,将在公安局网内查询个人身份证信息后,同步读取人才网入库信息

6:个人职称评审加20分

7:个人信誉贷款加10分

8:在国家人才网主办的国家网络招聘大会中纳入资料,供国家高端企业选择人才

办理(sfu毕业证书)西蒙菲莎大学毕业证【微信:741003700 】外观非常简单,由纸质材料制成,上面印有校徽、校名、毕业生姓名、专业等信息。

办理(sfu毕业证书)西蒙菲莎大学毕业证【微信:741003700 】格式相对统一,各专业都有相应的模板。通常包括以下部分:

校徽:象征着学校的荣誉和传承。

校名:学校英文全称

授予学位:本部分将注明获得的具体学位名称。

毕业生姓名:这是最重要的信息之一,标志着该证书是由特定人员获得的。