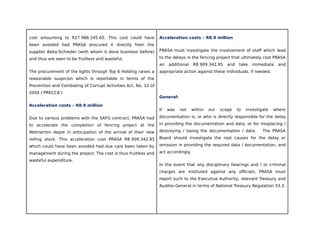

The document summarizes an investigation into a contract awarded by PRASA to SA Fence and Gate (SAFG). It finds that:

1) PRASA officials Chris Mbatha and Matshidiso Mosholi failed to comply with regulations in awarding the contract and subsequent deviations, resulting in irregular expenditure.

2) SAFG was paid R295 million, or 91% of the total contract value, despite completing only an estimated 46% of the work.

3) Payments made in relation to the irregular contract and deviations must be reported to the National Treasury.

Disciplinary action is recommended against officials involved in the non-compliance and unauthorized payments.

![Day 1 Leadership and Change Management Tunisia Hmam[1].ppt](https://cdn.slidesharecdn.com/ss_thumbnails/day1leadershipandchangemanagementtunisiahmam1-230527150908-672f35d2-thumbnail.jpg?width=640&height=640&fit=bounds)