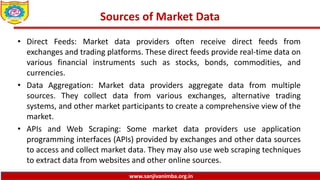

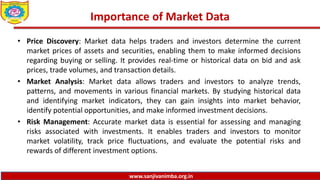

Investment banks rely on market data providers for timely, accurate financial information and data to support decision-making. Major providers include Bloomberg, Refinitiv, and FactSet. They collect, process, and distribute real-time market quotes, historical price movements, trading volumes, economic indicators, news, and other data used by investment professionals for research, analysis, and informed investing decisions. Access to high-quality market data from reliable sources is crucial for investment banks' trading, risk management, and overall operations.