Downloaded 17 times

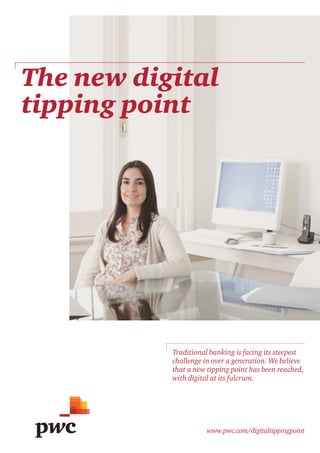

![Customers value new digital offerings

Not only does digital deepen levels of customer engagement,

it also opens up avenues for the monetisation of new services.

In our research, PwC tested the level of interest in a number of

theoretical digital capabilities.

As part of our survey, we tested the Our research indicated that across

willingness of customers to pay for different regions a base price can be

some innovative digital capabilities charged for these digital capabilities,

such as a digital wallet for loyalty cards, in the range of GBP2–10/month for

notifications through social media, each capability. At a time when banks

spending analysis tools, third-party are finding it difficult to sustain

offers and storing documents in a revenue and margin growth, the fact

virtual vault (see Figure 4). that customers appear prepared to

pay for the perceived value of using

In all markets, social media digital services that offer new value

notifications (except China), an to customers, is significant.

electronic wallet for loyalty cards

and financial tools were rated among

the top three from this list.

Figure 4: Appetite for innovative digital services

‘Which of the following would you be willing to pay for, please rank your top 3?’

I can be notified by My bank will store My bank can offer My bank can My bank would

1 Twitter/Facebook

2 loyalty cards and

3 spending analysis

4 offer me relevant

5 store key documents

for a transaction convert points to tools third-party offers in a virtual vault

occurring cash

UK 66.3 64.6 56.1 54.0 57.0

UAE 67.1 67.7 61.2 49.0 56.1

Poland 69.0 61.8 66.7 53.4 47.4

Mexico 73.7 62.8 61.3 46.4 57.2

India 85.1 65.3 58.7 43.6 45.2

Hong Kong 70.5 67.2 58.3 52.6 50.7

France 75.7 64.1 55.4 48.7 63.9

China 74.6 56.1 44.2 46.5

Canada 75.9 62.6 58.5 56.9 54.9

0 50 100 0 50 100 0 50 100 0 50 100 0 50 100

Level of interest [Scored ranking results (rank 1=100, 2=50, 3=25); average 0-100]

Source: PwC Digital Tipping Point Survey 2011

10 PwC The new digital tipping point](https://image.slidesharecdn.com/pwc-new-digital-tipping-point-121206142946-phpapp01/85/Pwc-new-digital-tipping-point-12-320.jpg)

Traditional banking is facing its biggest challenge in over a generation due to factors like increased regulation, public distrust, and new digital competitors. A new tipping point has been reached where digital will play a pivotal role. To create value going forward, banks need to focus on building customer relationships and engagement through digital offerings. Younger customers especially expect banking to be available through mobile and online channels, so banks must enhance their digital capabilities to attract these customers and remain relevant in the future.

![Open banking [Evolution, Risks & Opportunities]](https://cdn.slidesharecdn.com/ss_thumbnails/openbanking-210606160258-thumbnail.jpg?width=640&height=640&fit=bounds)