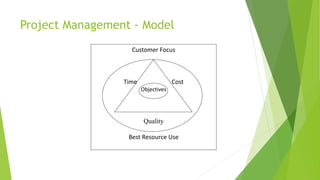

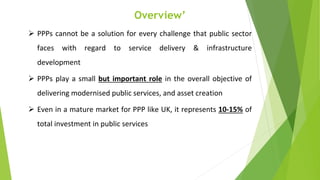

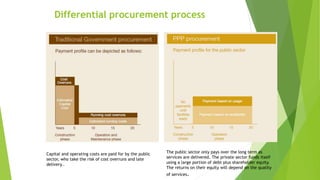

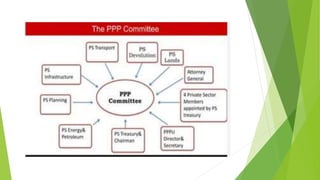

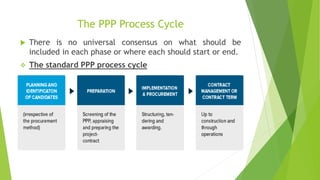

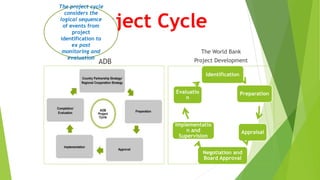

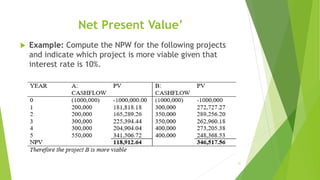

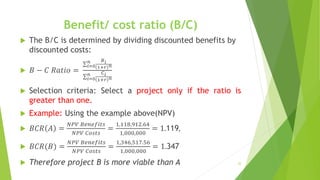

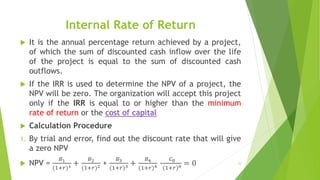

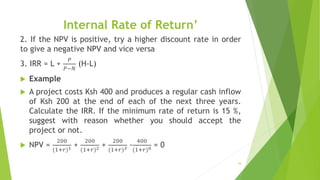

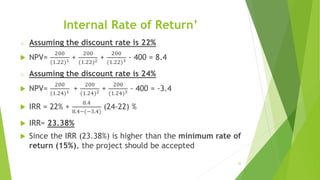

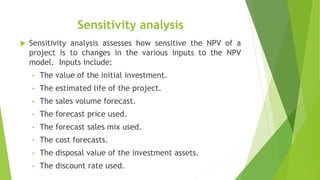

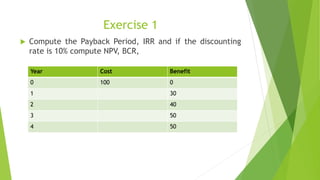

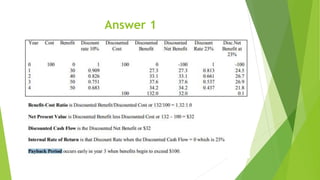

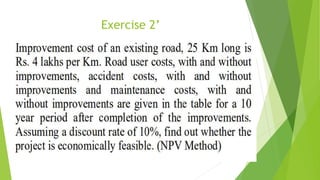

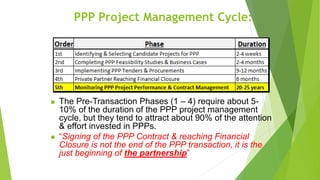

This document provides an overview of project appraisal and risk management for public-private partnerships (PPPs). It discusses the importance of the framework guiding PPP projects from identification through the project lifecycle. Key aspects of project appraisal covered include screening projects for PPP suitability, economic viability analysis, cost-benefit analysis, and risk assessment. The stages of the PPP process and differences between PPP and traditional procurement are also summarized.

![Material Adverse Government Action

1. For the purposes of PPP Contract, “Material Adverse

Government Action” means any act or omission by the

Contracting Authority or any relevant public authority or

event set out in Clause (2) below, which occurs during the

term of this PPP Contract and which

directly causes the Private Partner to be unable to comply

with all or some of its obligations under the PPP Contract

and/or

has a [Material] Adverse Effect] on its [costs or revenues]

[insert defined terms].](https://image.slidesharecdn.com/publicprivatepartnershipmanagement-module-230929040952-37ff8a7a/85/PUBLIC-PRIVATE-PARTNERSHIP-MANAGEMENT-Module-pptx-167-320.jpg)

![Cont…’

2. For the purposes of Clause (1) above any act or

omission shall mean and be limited to the following

circumstances:

i. failure of any relevant public authority to grant to the

Private Partner or renew any permit or approval that is

required for the purposes of the Private Partner’s proper

performance of its obligations and/or enforcement of its

rights under this PPP Contract, in each case

ii. within the required timeframe under [Applicable Law],

except where such failure results from the Private

Partner’s non-compliance with [Applicable Law];](https://image.slidesharecdn.com/publicprivatepartnershipmanagement-module-230929040952-37ff8a7a/85/PUBLIC-PRIVATE-PARTNERSHIP-MANAGEMENT-Module-pptx-168-320.jpg)

![Cont..’

The following standard provisions of the direct agreement

are the most important:

The lender is given a 'cure period' (i.e., extra time to take

action to remedy the Project Company's default in

addition to that given to the Project Company) before the

[project company's] contract is terminated. These cure

periods are limited in length (it is usually sufficient

enough for the lender to take active steps to find a

solution to the problem)](https://image.slidesharecdn.com/publicprivatepartnershipmanagement-module-230929040952-37ff8a7a/85/PUBLIC-PRIVATE-PARTNERSHIP-MANAGEMENT-Module-pptx-175-320.jpg)

![Cont..’

The lender has the right to 'Step-In' to the contract during

the cure period. This means that it can appoint a nominee

to undertake the Project Company's rights in parallel with

the Project Company or substitute the project company.

The lender will [normally] not assume any additional

liability as a result of Step-In or substitution, unless the

lender exercises the step-in right itself.

The Project Company undertakes not to obstruct the

lender’s exercise of [its] Step-In and substitution rights.](https://image.slidesharecdn.com/publicprivatepartnershipmanagement-module-230929040952-37ff8a7a/85/PUBLIC-PRIVATE-PARTNERSHIP-MANAGEMENT-Module-pptx-176-320.jpg)

![Variations of the Step-In Right’

iii. Novation

The final variation of step-in right implies transfer of all

of the project company's rights and obligations to a

substitute entity and removal of the project company

from the project. This type of step-in right may require

consent of "various project participants [e.g. contractors,

sub-contractors, or customers].

when the project company experiences severe difficulties,

the lender instead of keeping the project company liable

for the project can novate the whole project to another

company which is more capable or fulfilling the project.](https://image.slidesharecdn.com/publicprivatepartnershipmanagement-module-230929040952-37ff8a7a/85/PUBLIC-PRIVATE-PARTNERSHIP-MANAGEMENT-Module-pptx-180-320.jpg)