Downloaded 16 times

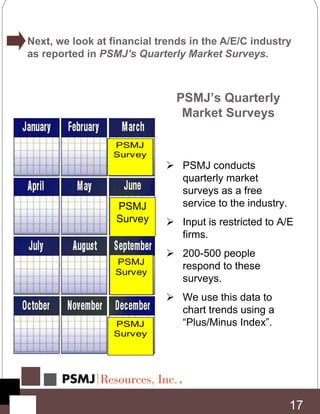

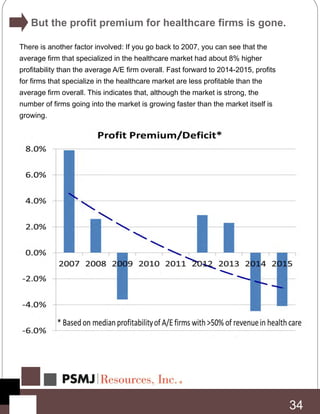

The PSMJ Resources, Inc. report analyzes the architecture, engineering, and construction (A/E/C) markets for 2016, highlighting economic trends, current industry conditions, and forecasts for future market sectors. The report finds that while the overall economy is experiencing growth, challenges exist in labor market tightness and rising overhead costs, with profitability nearing pre-recession levels. Recommendations for A/E/C firms emphasize adapting strategies based on leading indicators and proposal opportunities to capitalize on the industry's optimistic outlook.