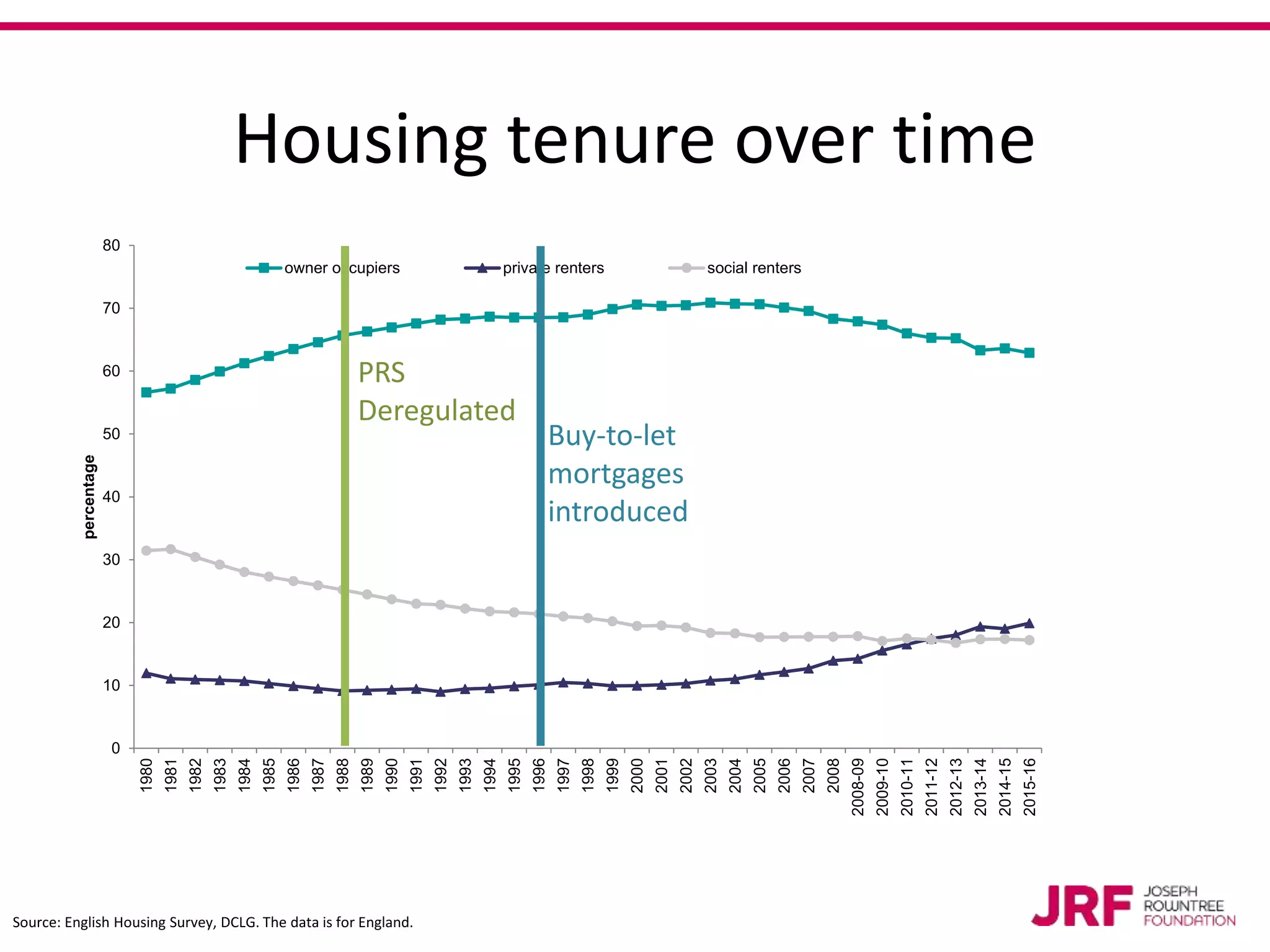

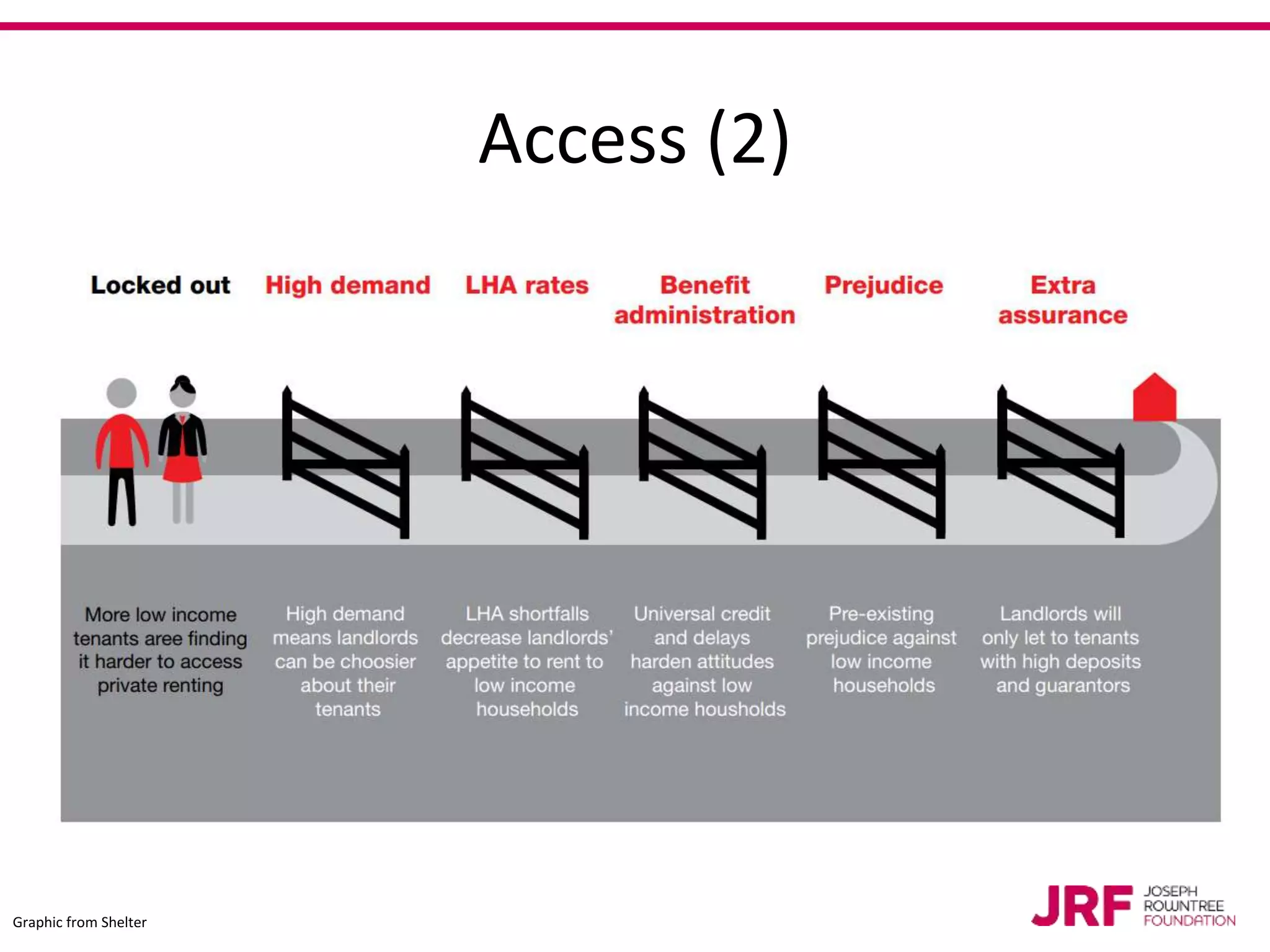

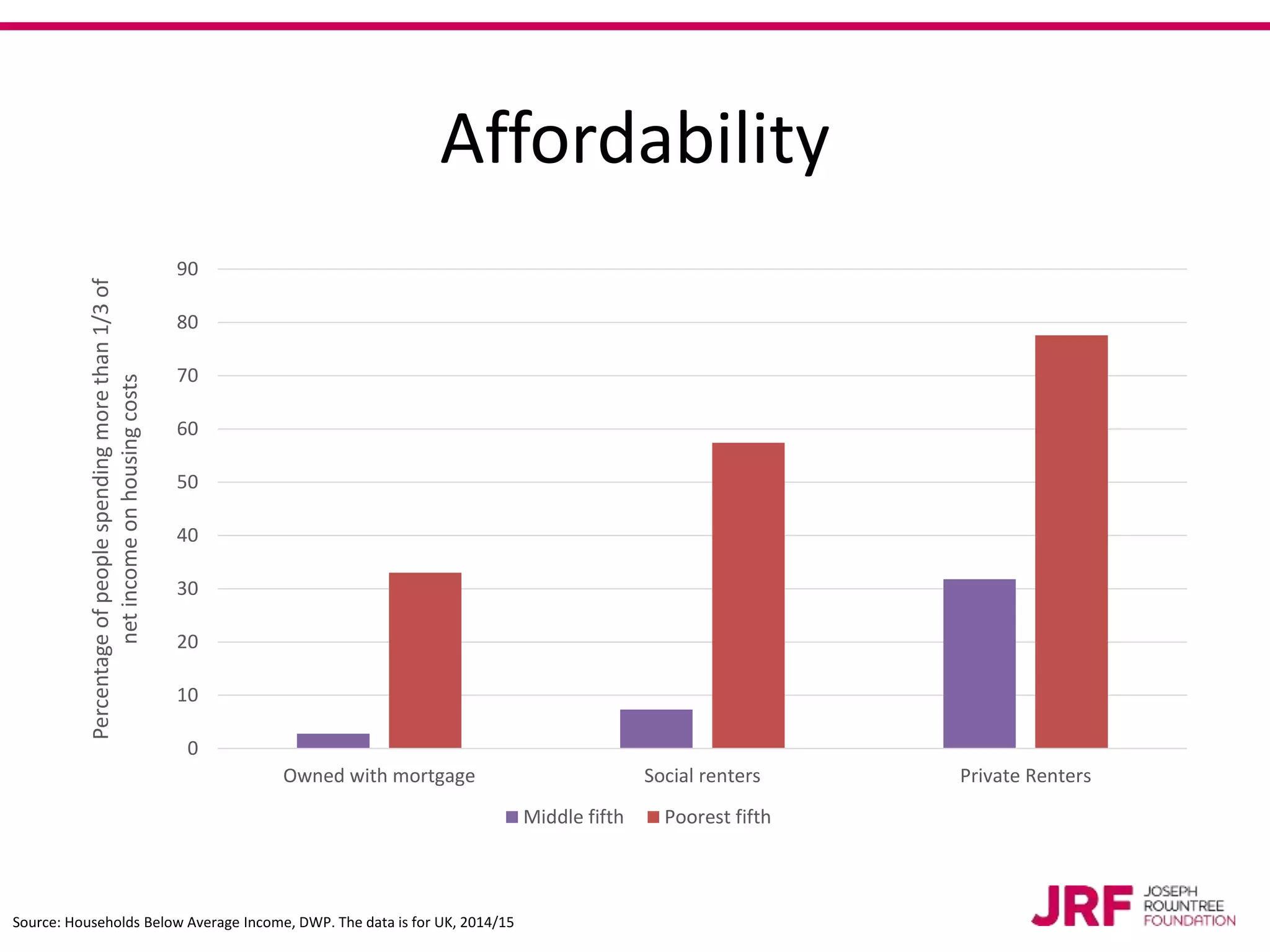

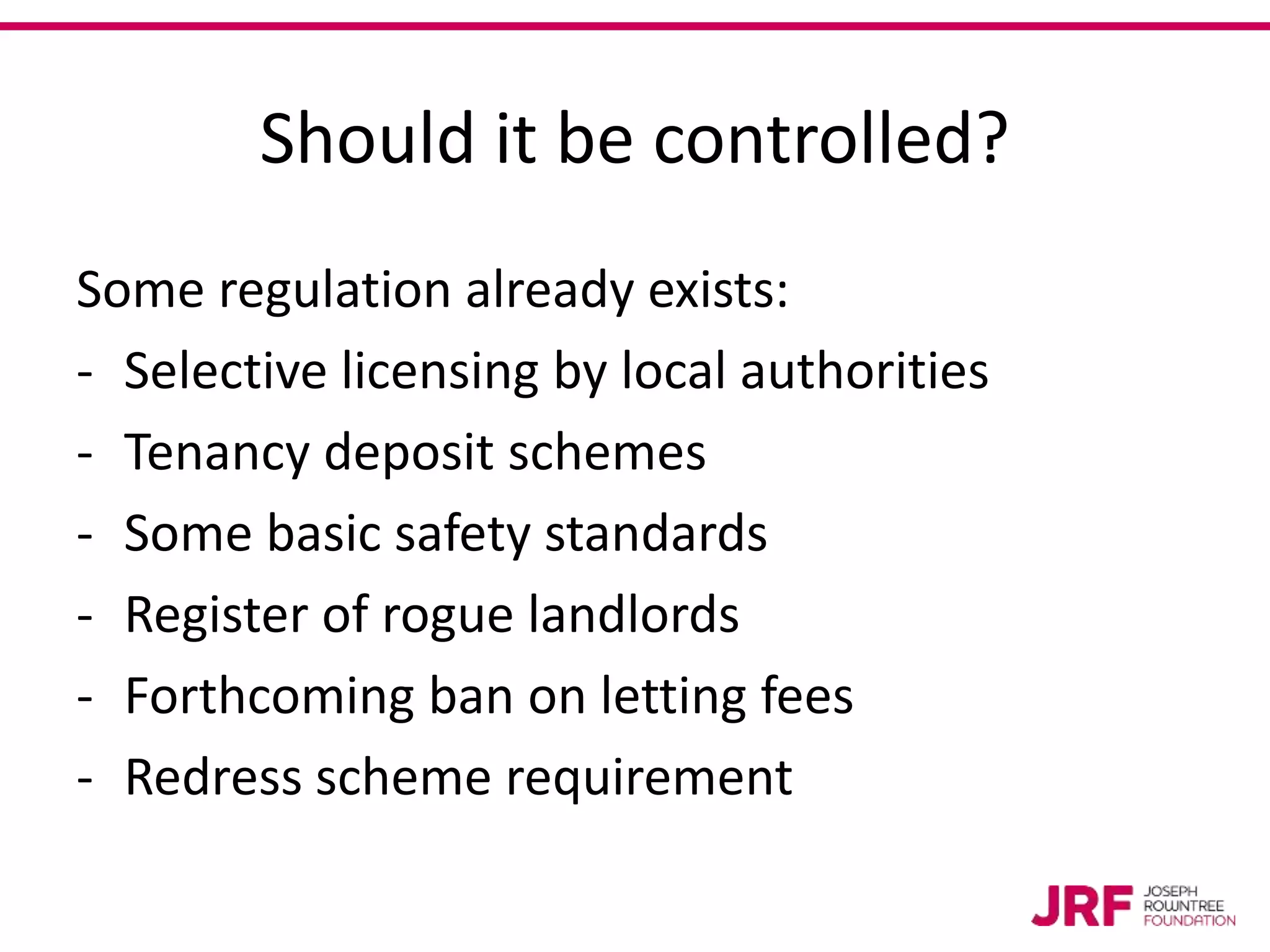

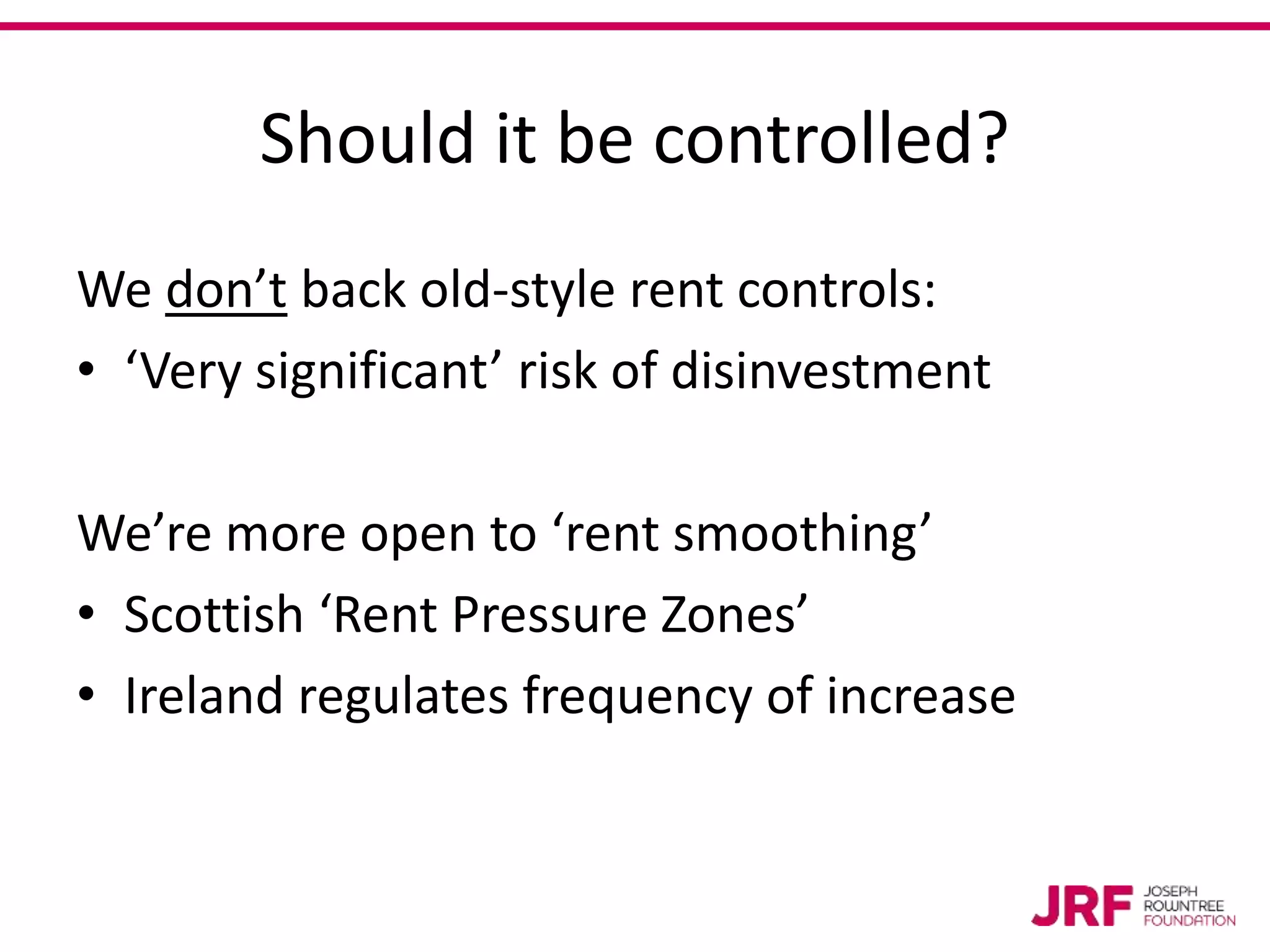

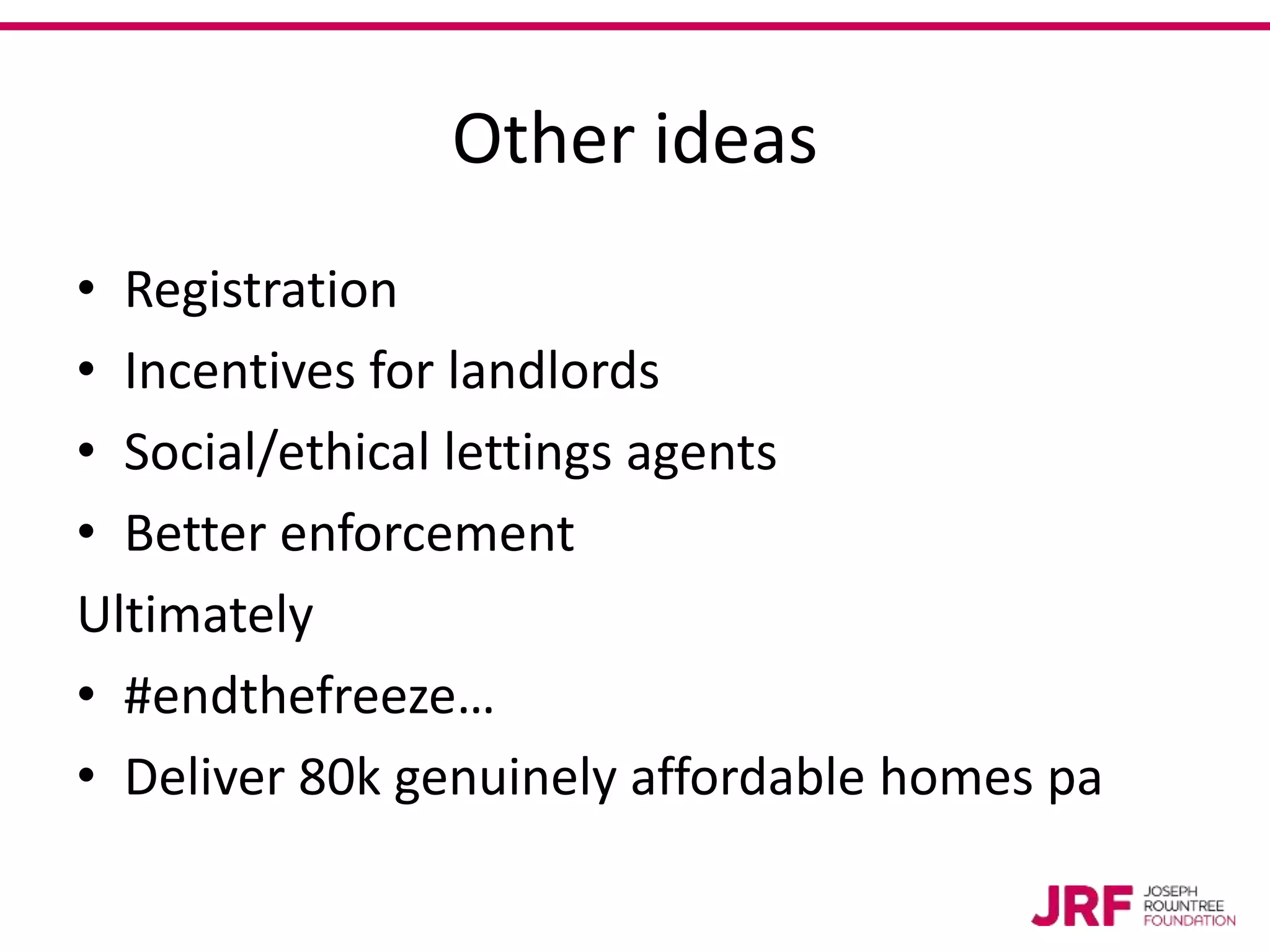

The document discusses the current state of the private rented sector (PRS) in England, highlighting its purposes, effectiveness, and the rationale behind its growth. It examines issues of access, affordability, quality, and stability, and raises questions about the need for further regulation while outlining existing controls. The presentation suggests a preference for regulatory approaches such as rent smoothing and better enforcement rather than traditional rent controls.