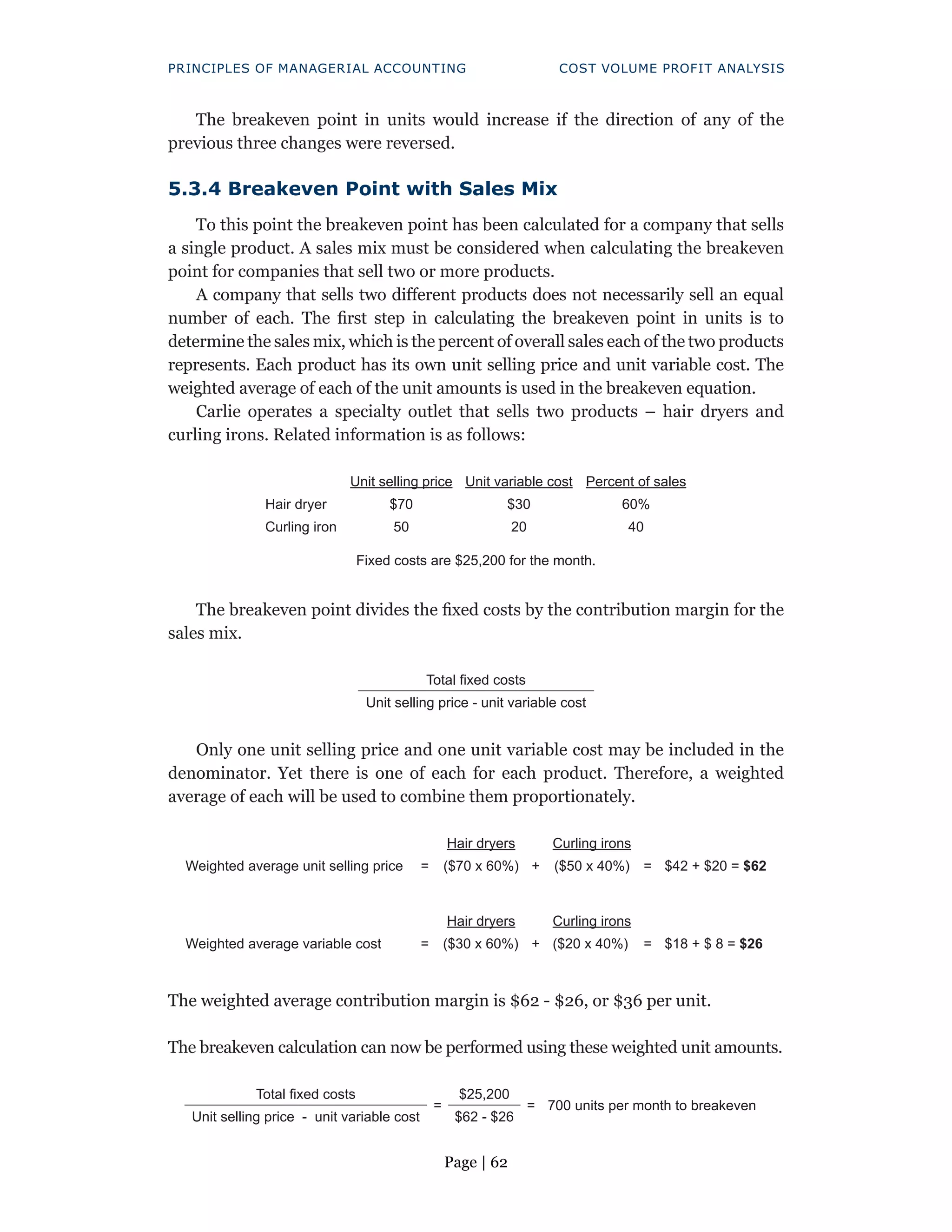

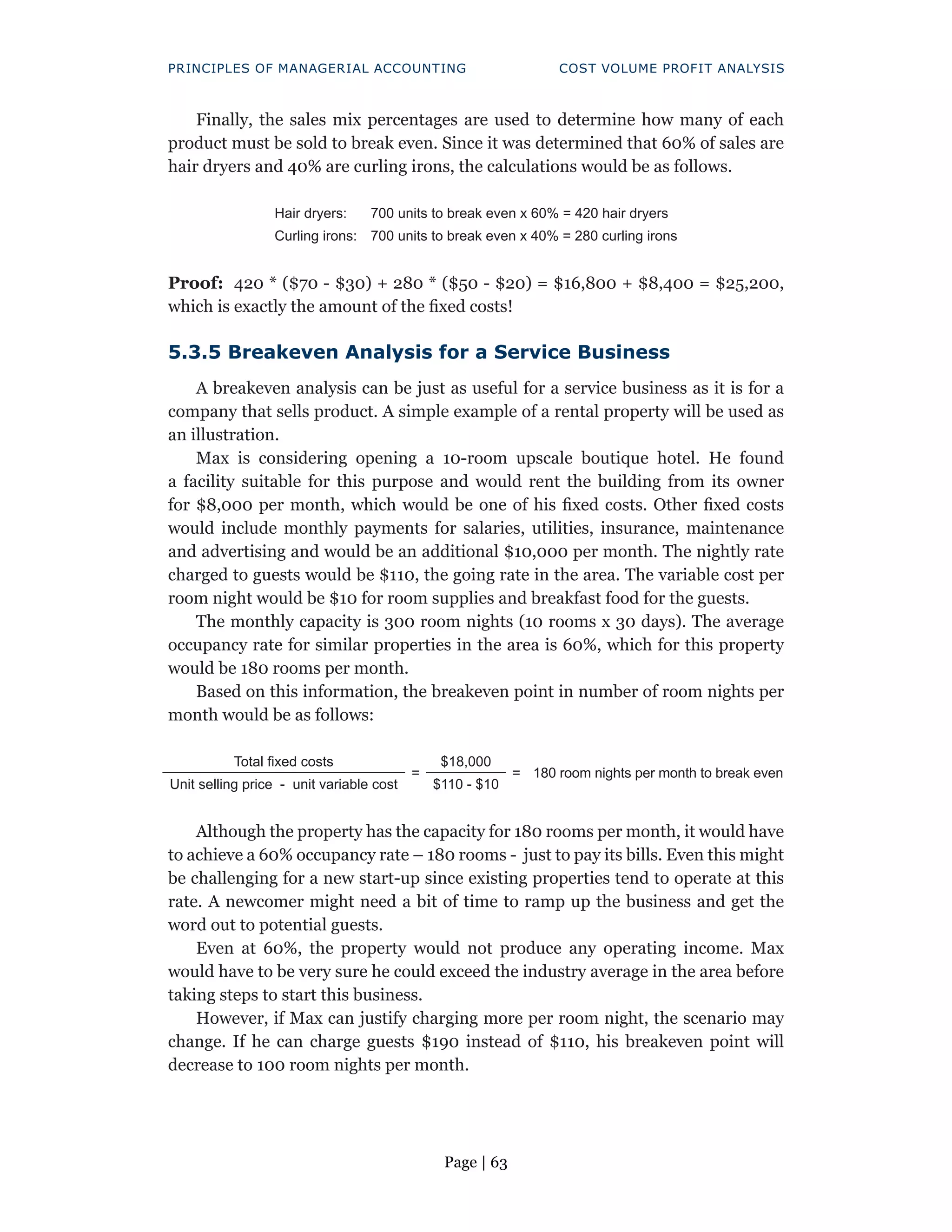

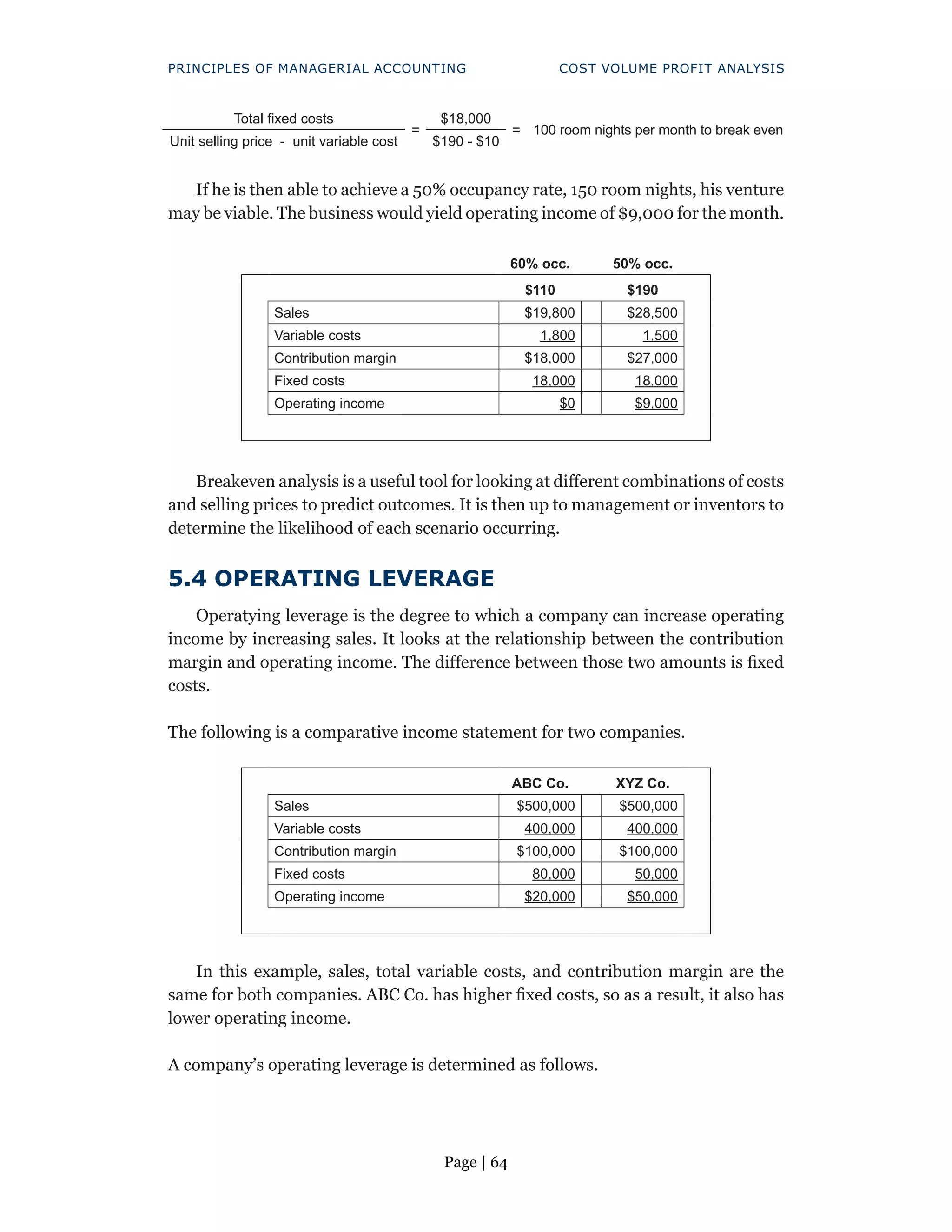

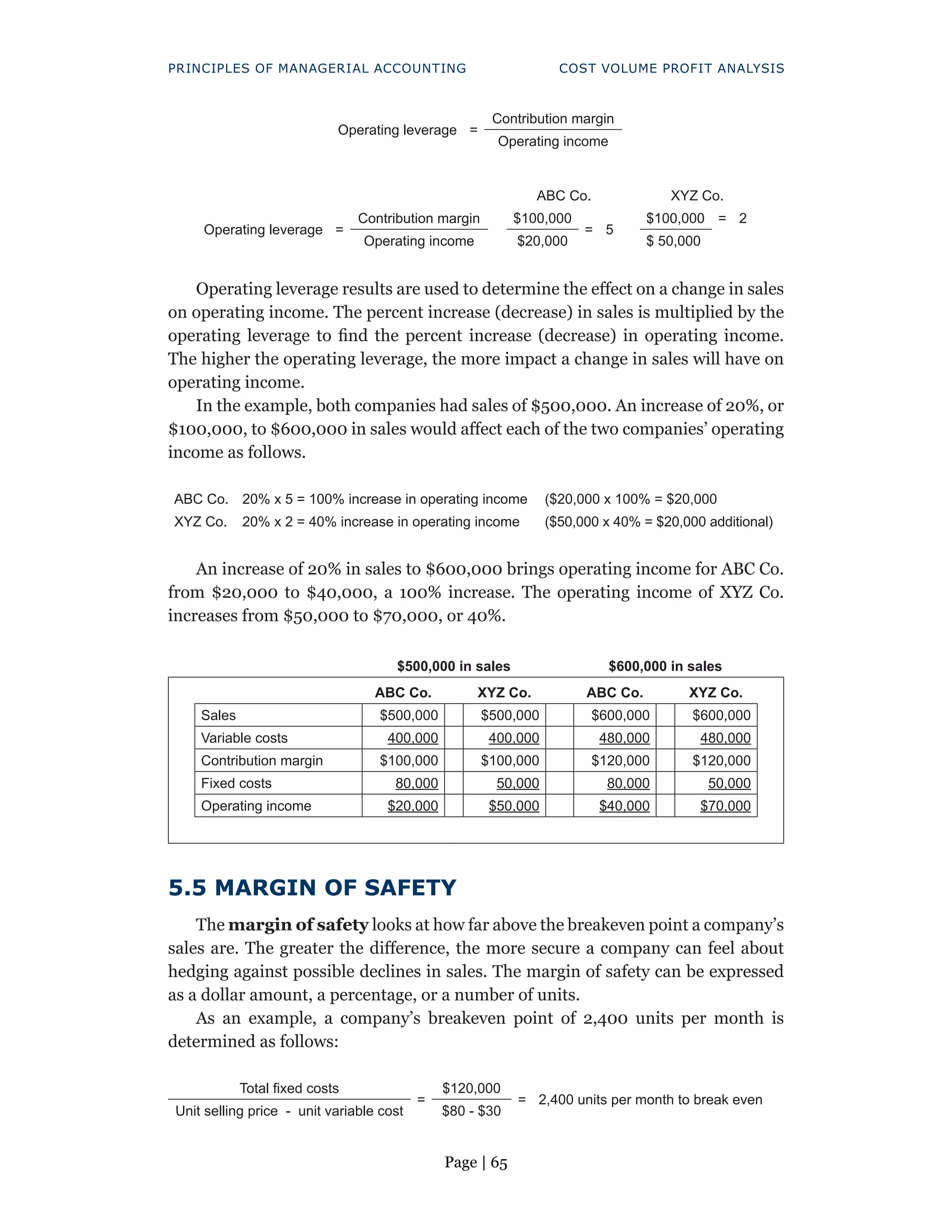

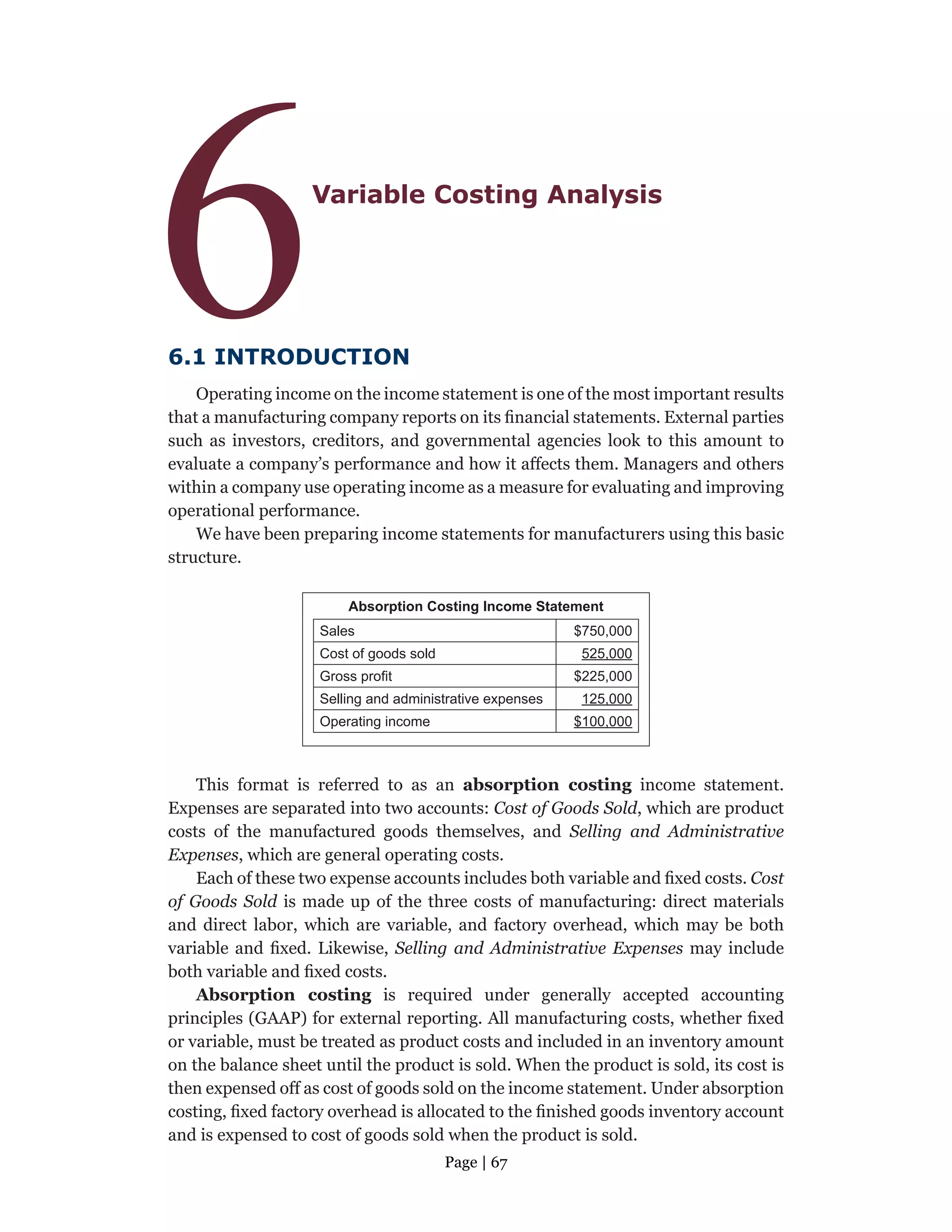

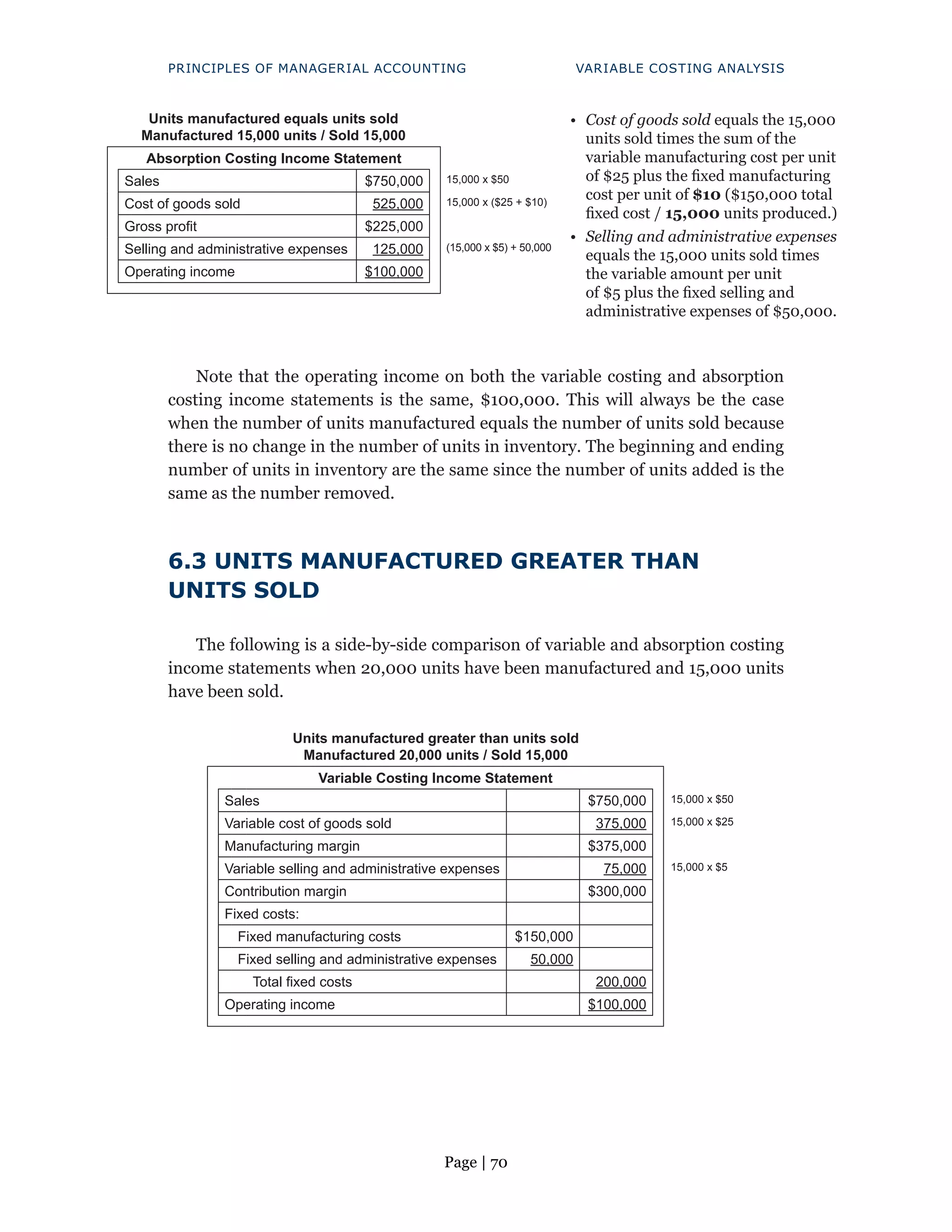

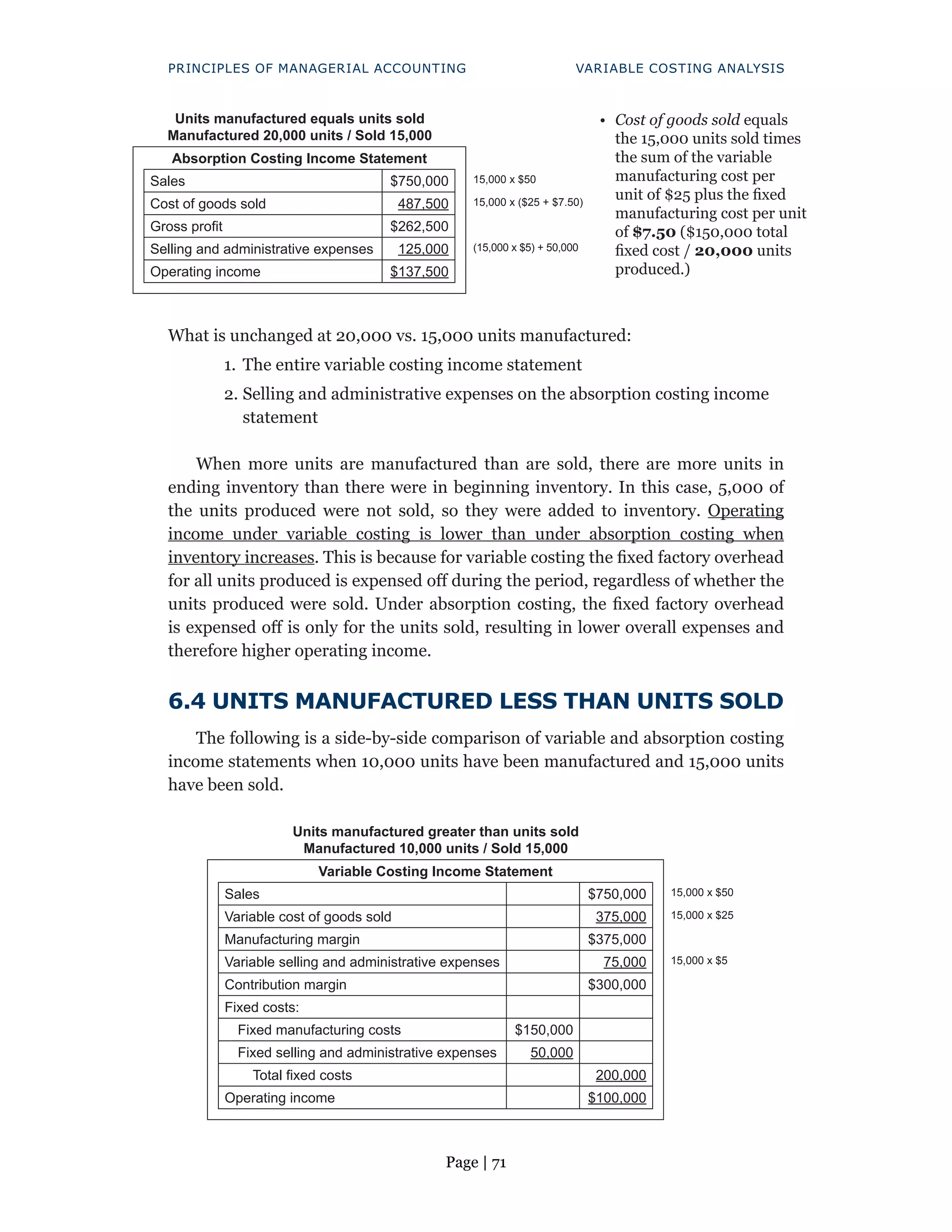

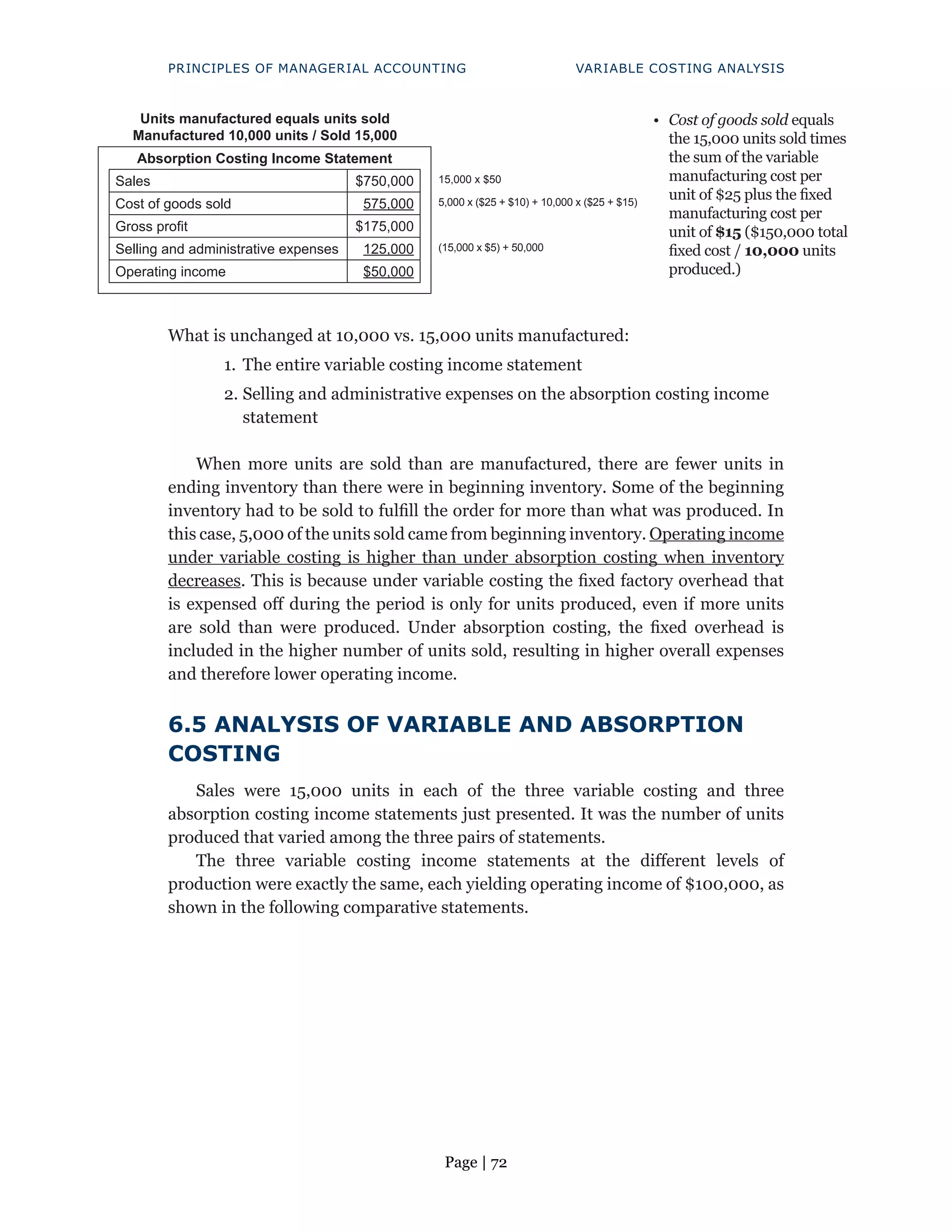

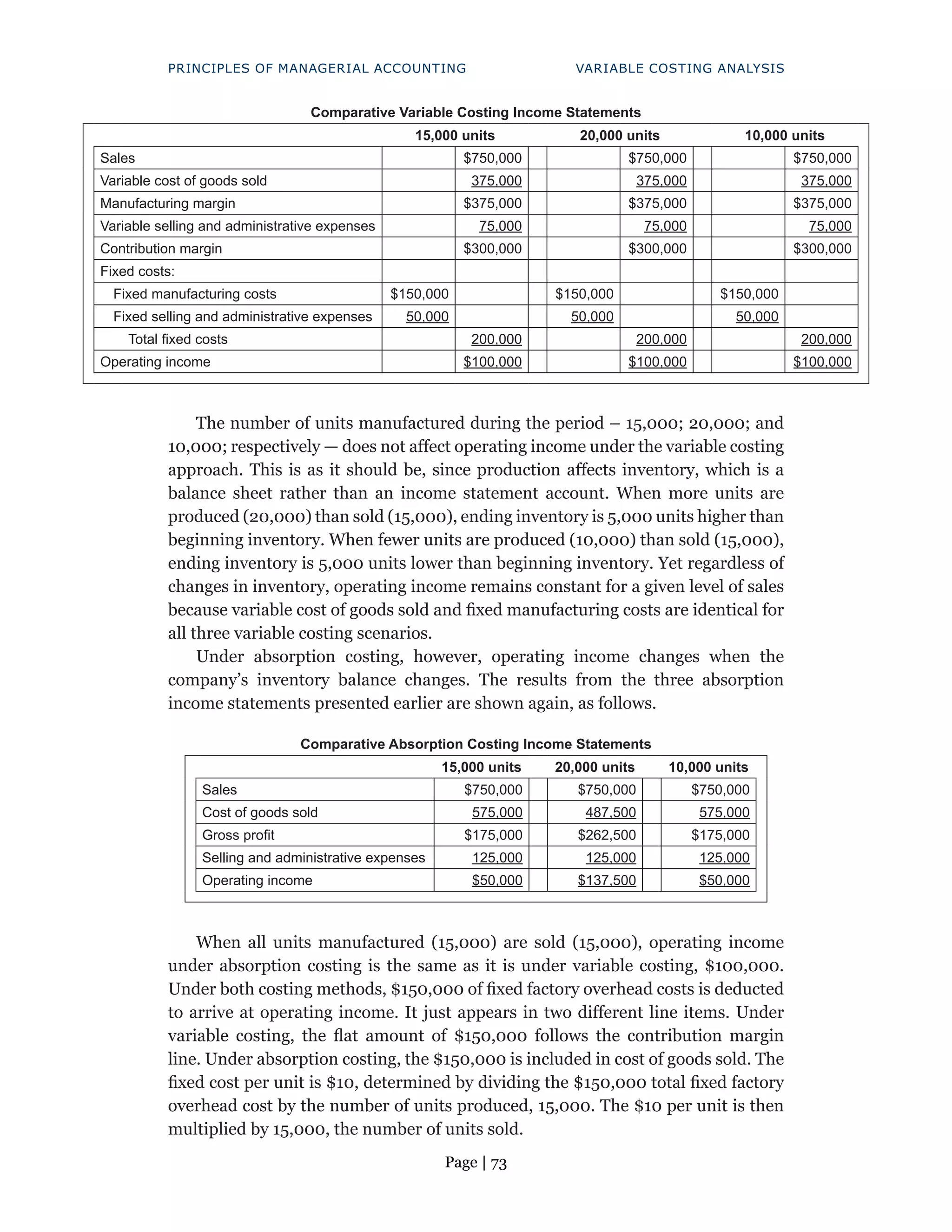

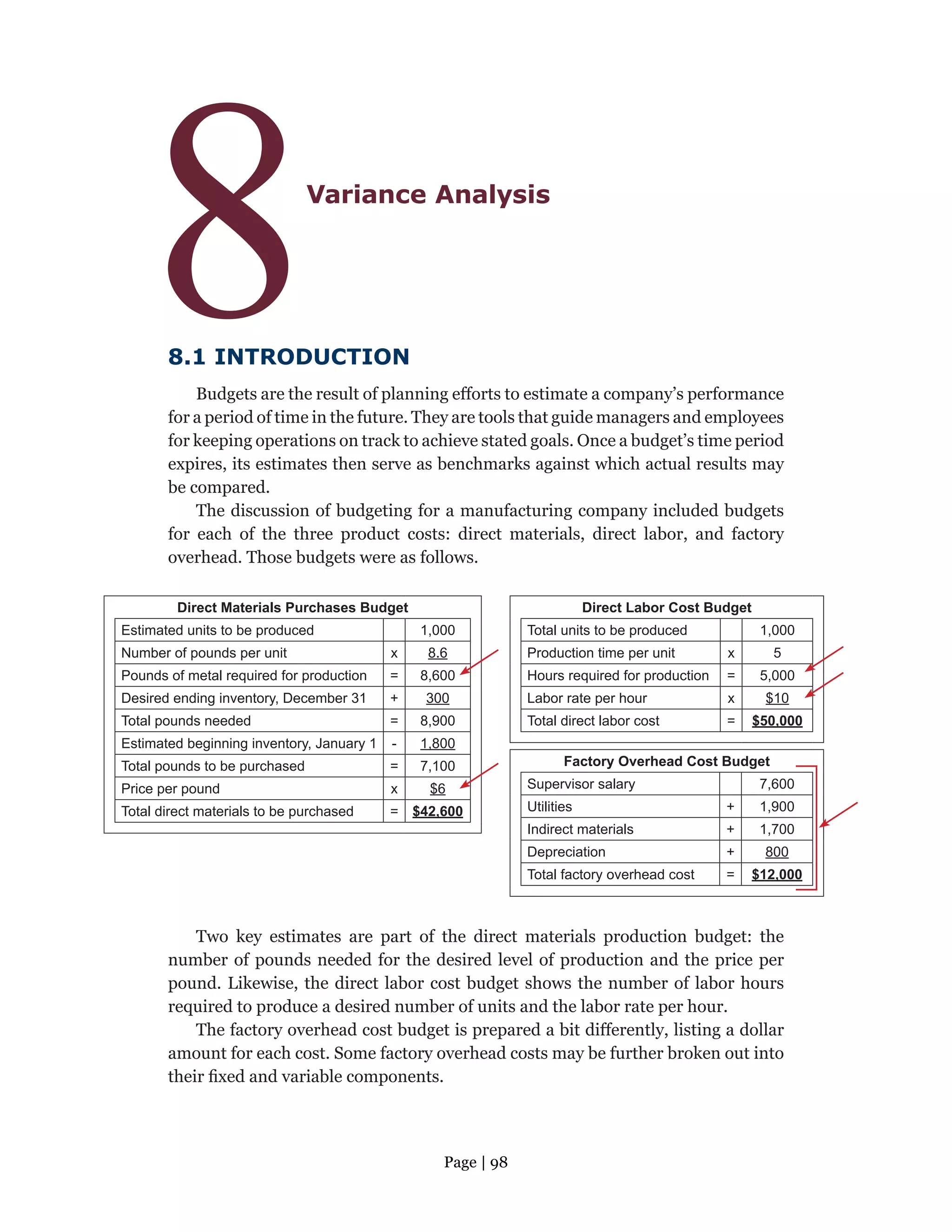

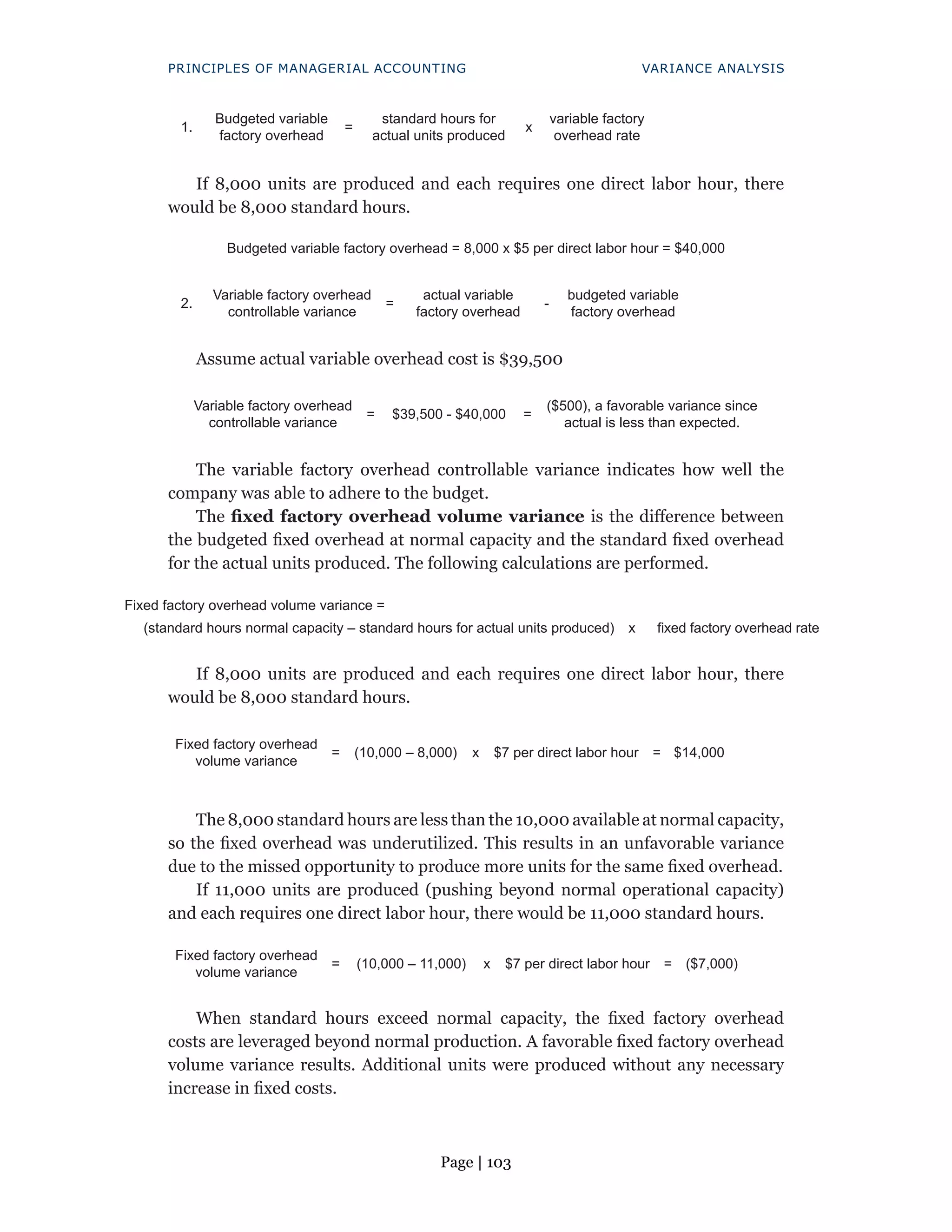

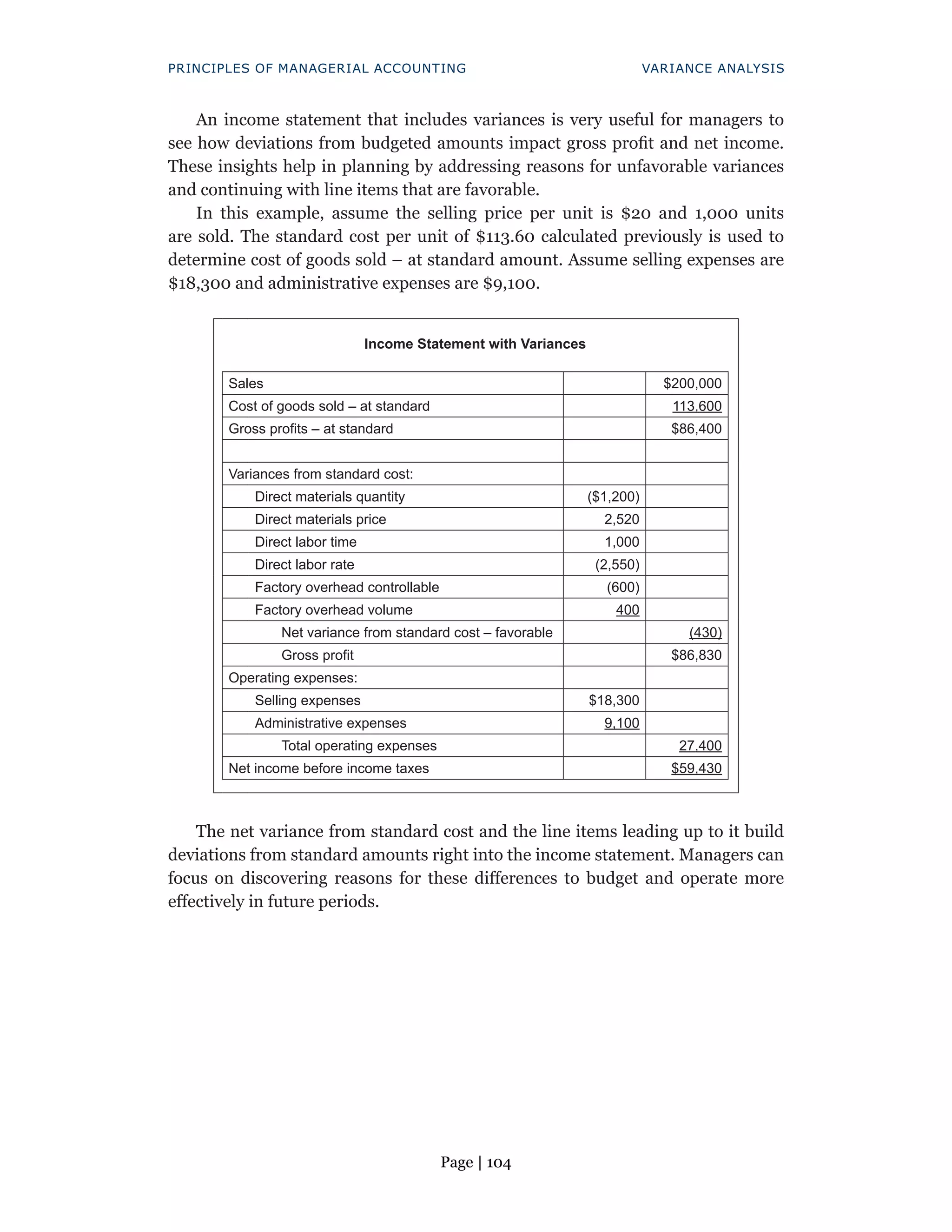

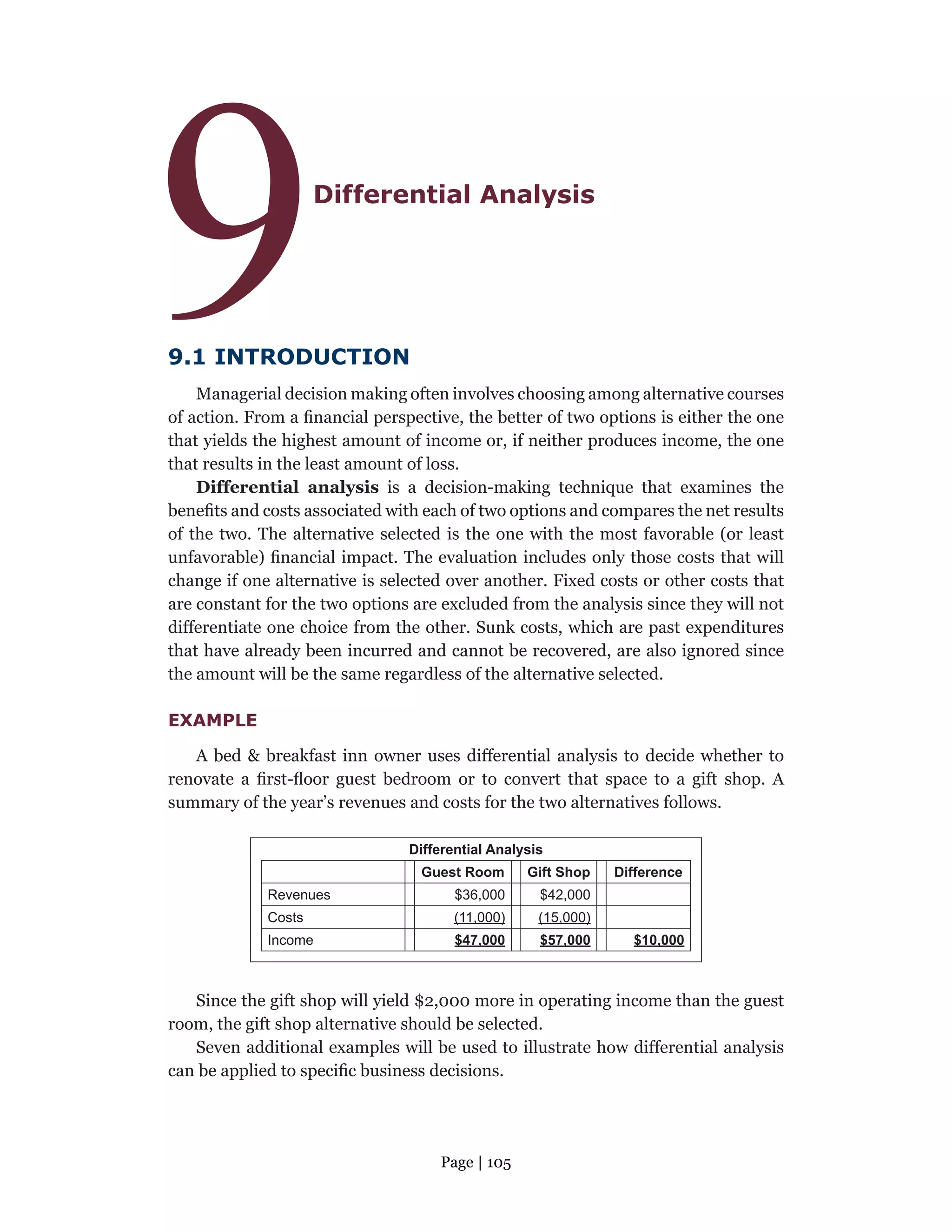

This document provides an introduction to managerial accounting concepts. It defines managerial accounting as providing internal reports customized for management decision making, as opposed to external financial reporting. It notes managerial accounting involves actual and estimated future financial data. The main topics covered include accumulating costs, analyzing costs, evaluating performance, and comparing alternatives. It states the goal is to generate profit by controlling costs, which impact profitability. Managerial accounting is relevant for service, merchandising, and manufacturing businesses.

![Cost accounting a managerial emphasis 2nd [Australian] edition. Edition Datar](https://cdn.slidesharecdn.com/ss_thumbnails/81045-250422035945-405477cc-thumbnail.jpg?width=640&height=640&fit=bounds)