The document outlines various auditing and accounting aspects of companies according to the Companies Act, including:

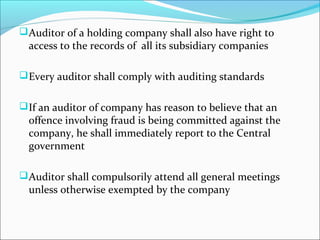

1) Auditors are appointed for a period of 5 years, except in specific cases like auditors appointed by CAG. Appointment must be ratified annually at the AGM. Auditors cannot be appointed for more than one 5-year term (individuals) or two 5-year terms (firms).

2) Companies must comply with auditor rotation within 3 years. Auditors can only be removed by special resolution with government approval before completing their term. Auditors are appointed based on audit committee recommendations.

3) Penalties are specified for companies, officers, and auditors if provisions are contraven

![KWL Chart Graphic Organizer in Green and Yellow Minimalist Style[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/kwlchartgraphicorganizeringreenandyellowminimaliststyle1-241211092106-322ddd2c-thumbnail.jpg?width=640&height=640&fit=bounds)