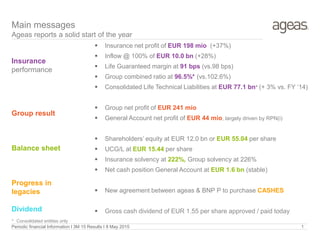

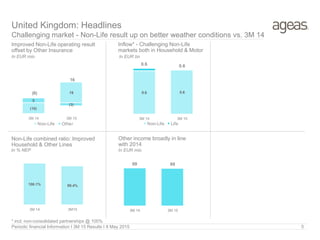

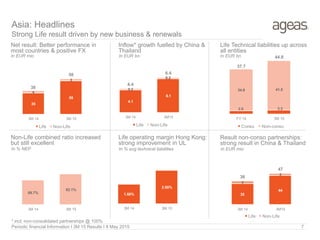

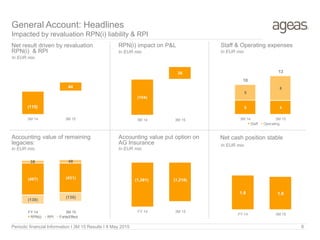

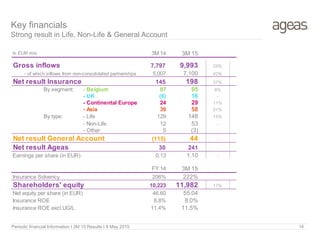

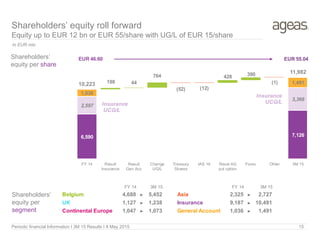

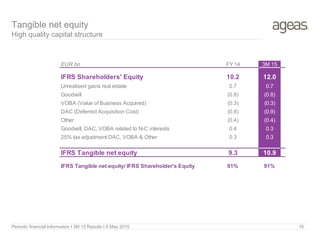

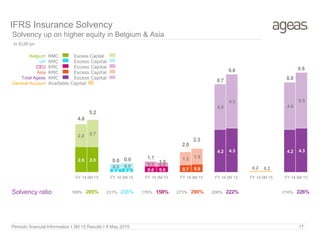

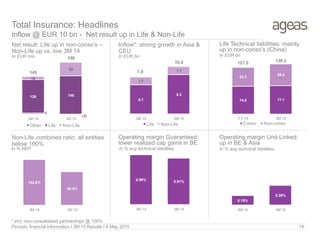

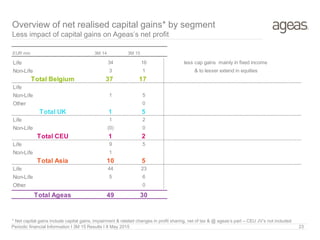

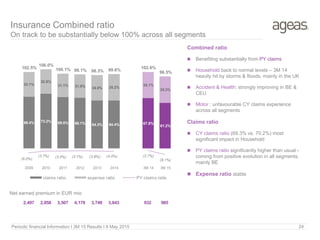

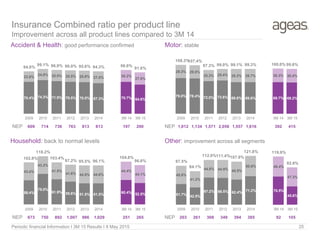

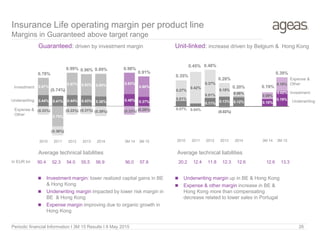

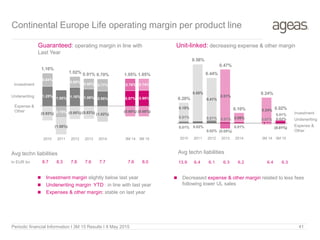

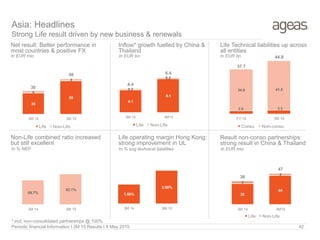

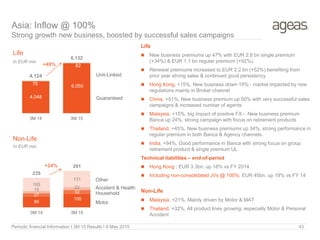

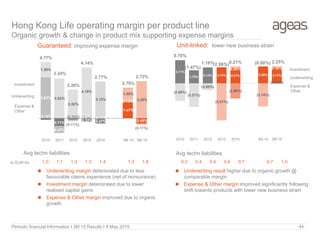

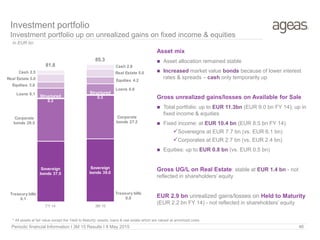

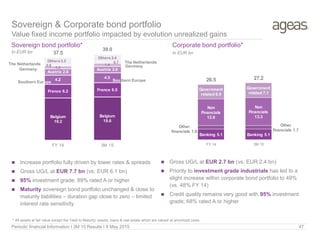

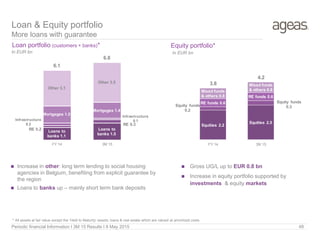

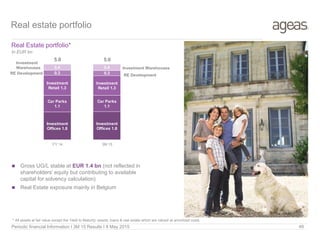

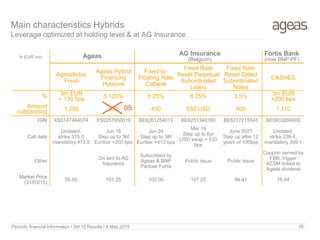

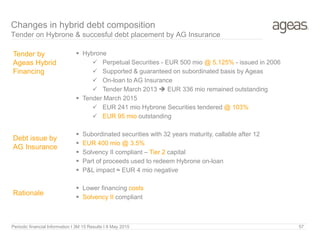

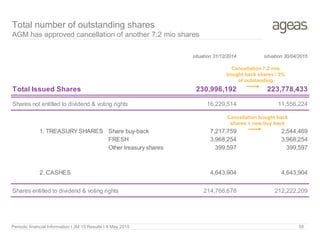

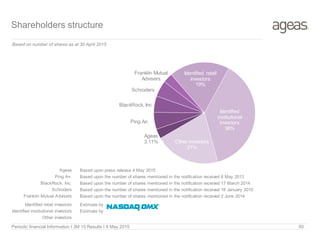

Ageas reported solid results for the first quarter of 2015. Insurance net profit increased 37% to EUR 198 million, driven by growth in both life and non-life segments. Gross inflows also increased 28% to EUR 9.9 billion. The group's net profit was EUR 241 million and shareholders' equity rose to EUR 11.9 billion. Insurance solvency increased to 222% and Ageas approved a gross cash dividend of EUR 1.55 per share to be paid.

![Awareness of digital currency[1] (1).pptx](https://cdn.slidesharecdn.com/ss_thumbnails/awarenessofdigitalcurrency11-260125155504-b1badee4-thumbnail.jpg?width=640&height=640&fit=bounds)