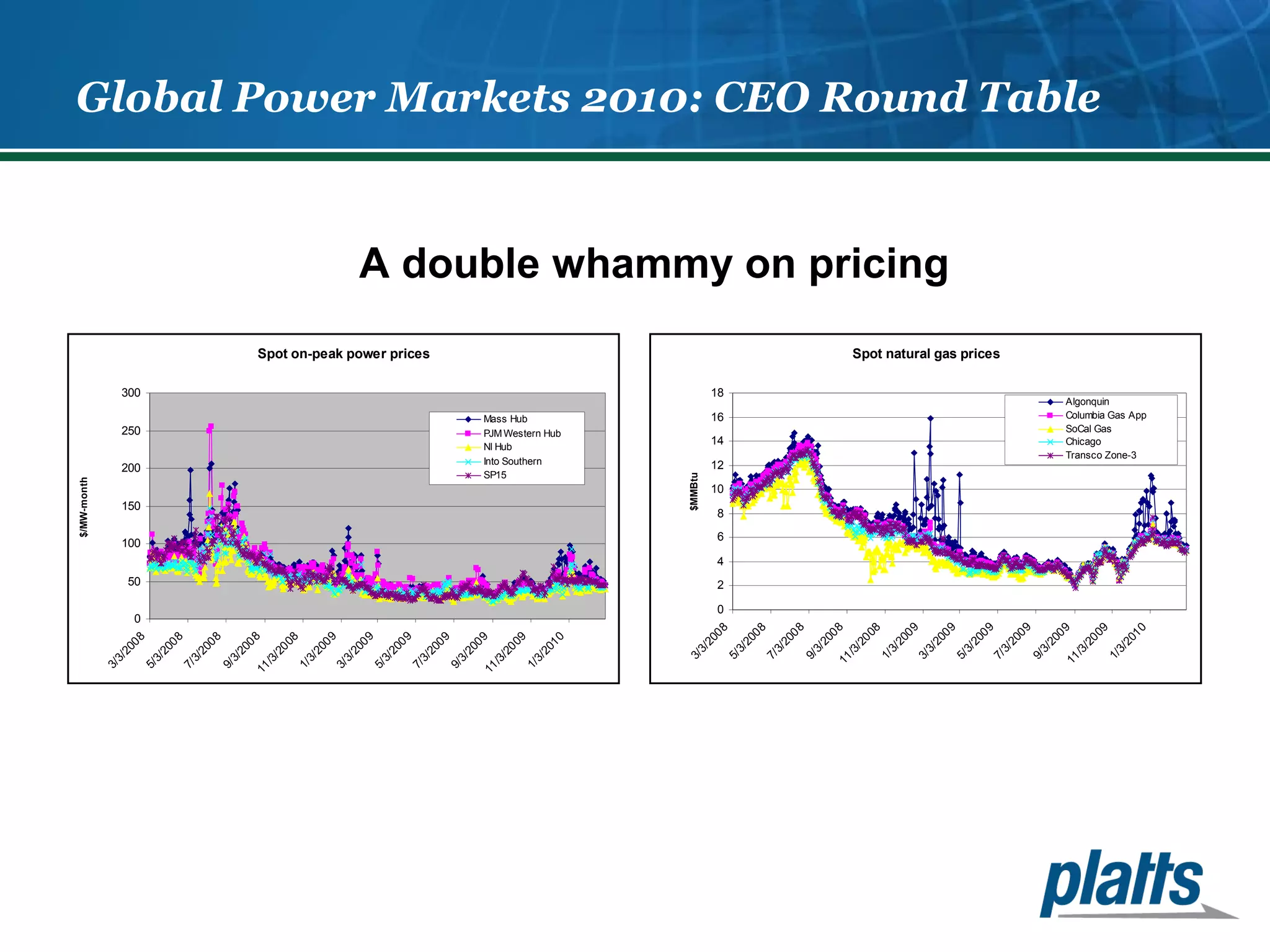

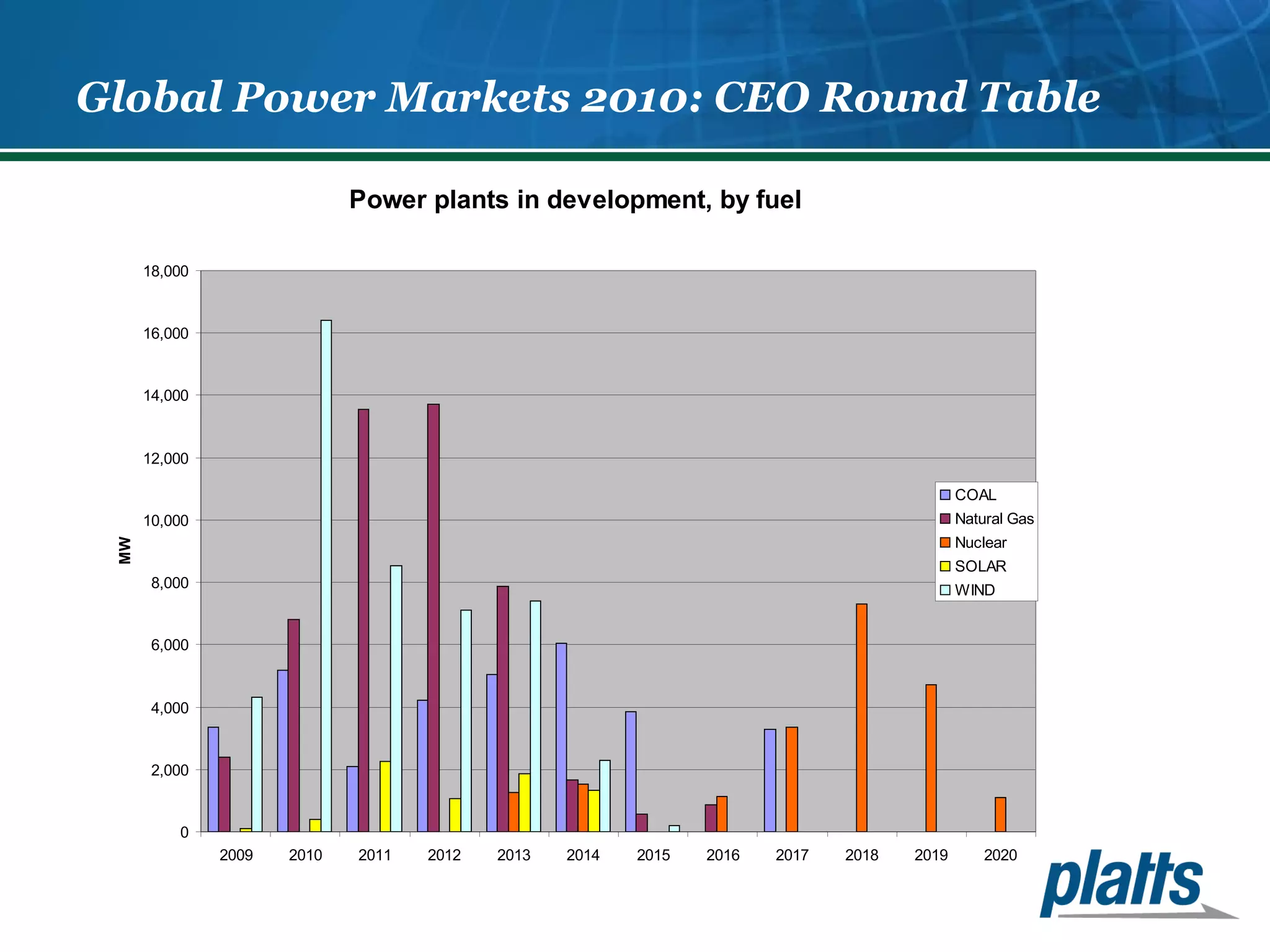

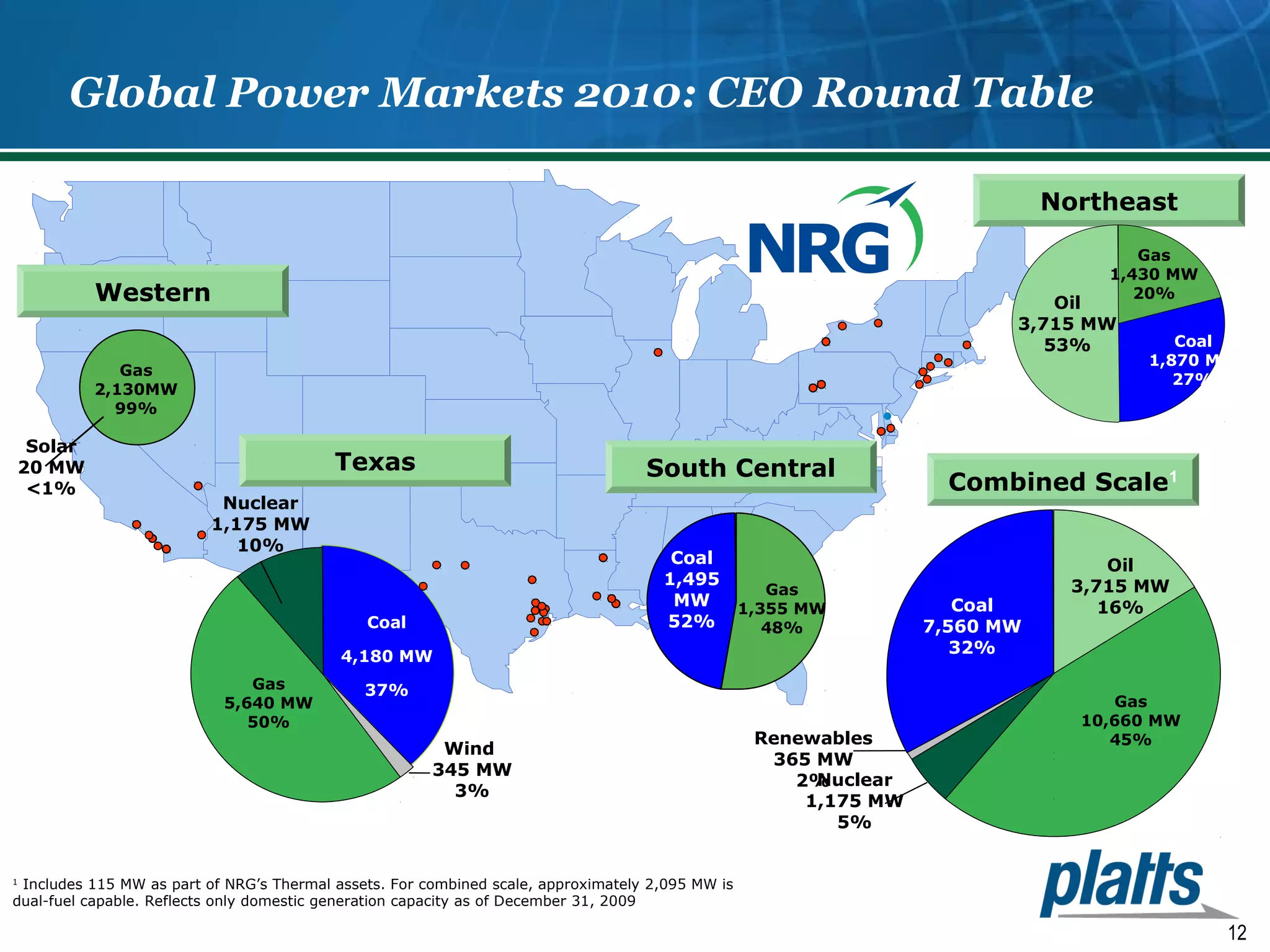

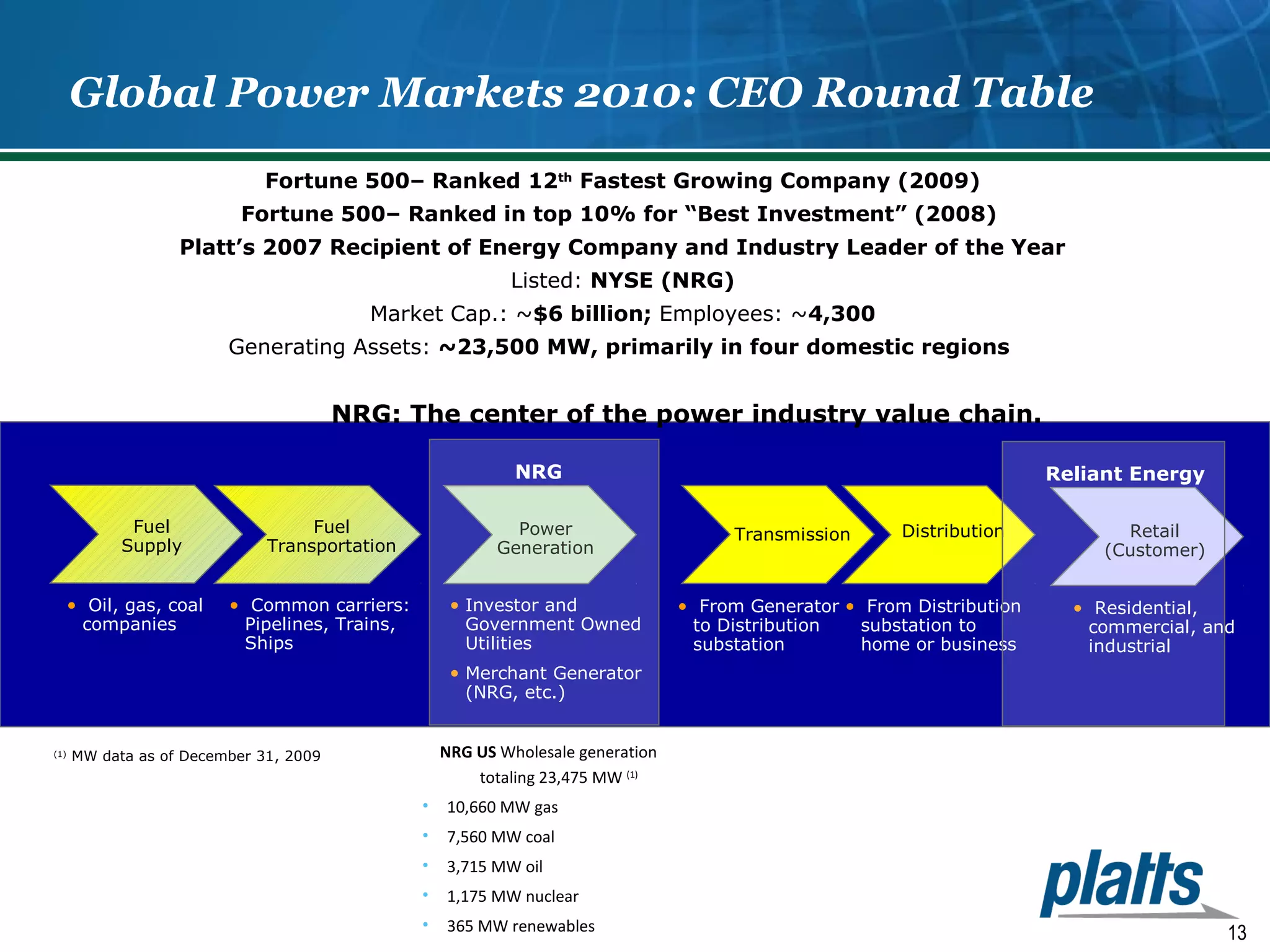

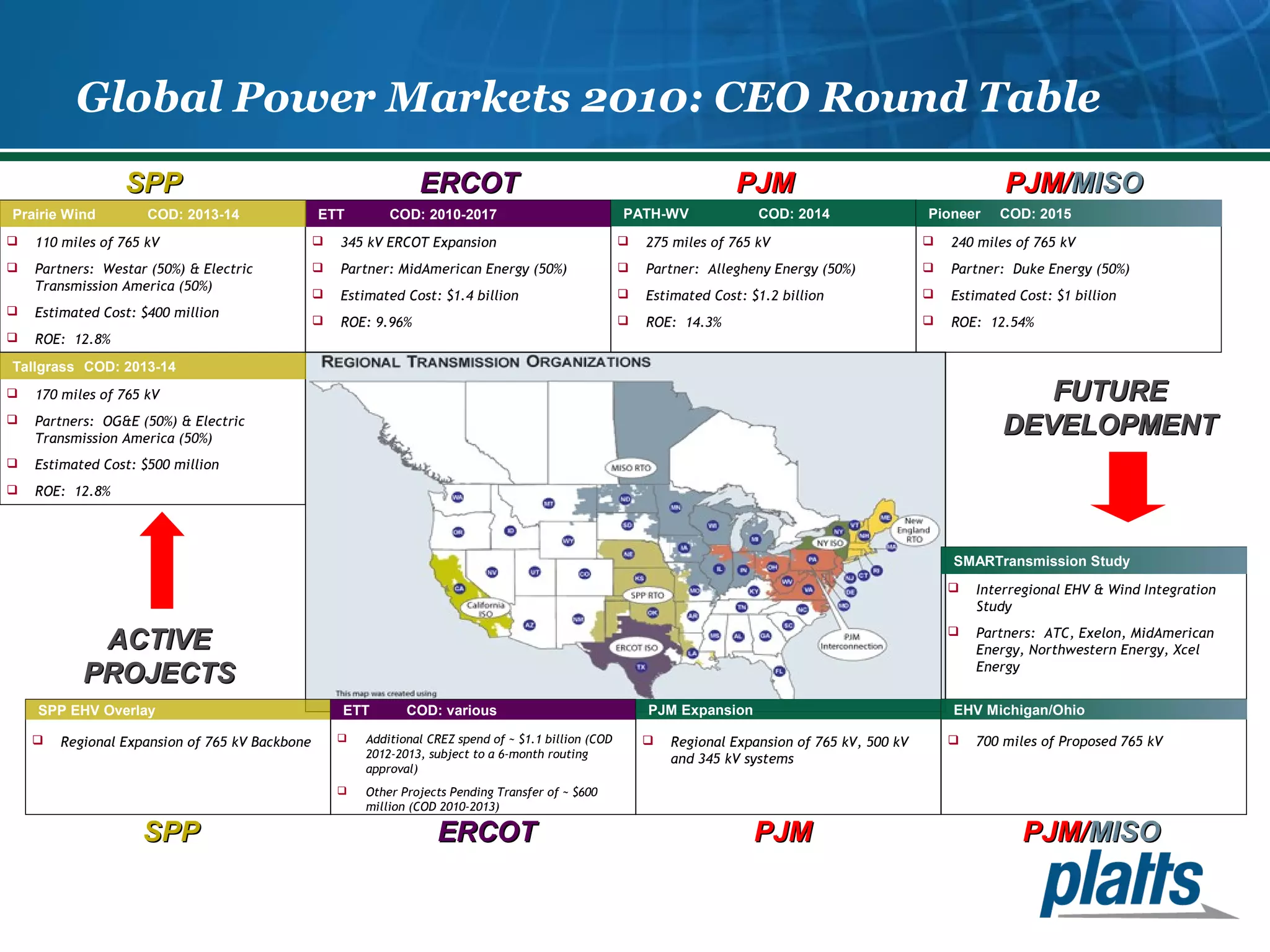

This document summarizes the 25th Annual Global Power Markets Conference held in Las Vegas in 2010. It discusses several key topics from the conference including pending US climate change legislation, electricity demand trends, spot power and natural gas prices, renewable energy projects receiving federal funding, and power plants under construction or development in the US. It also includes presentations from CEOs of major power companies such as NRG Energy, Calpine, and American Electric Power who discuss their business strategies and generation portfolios.