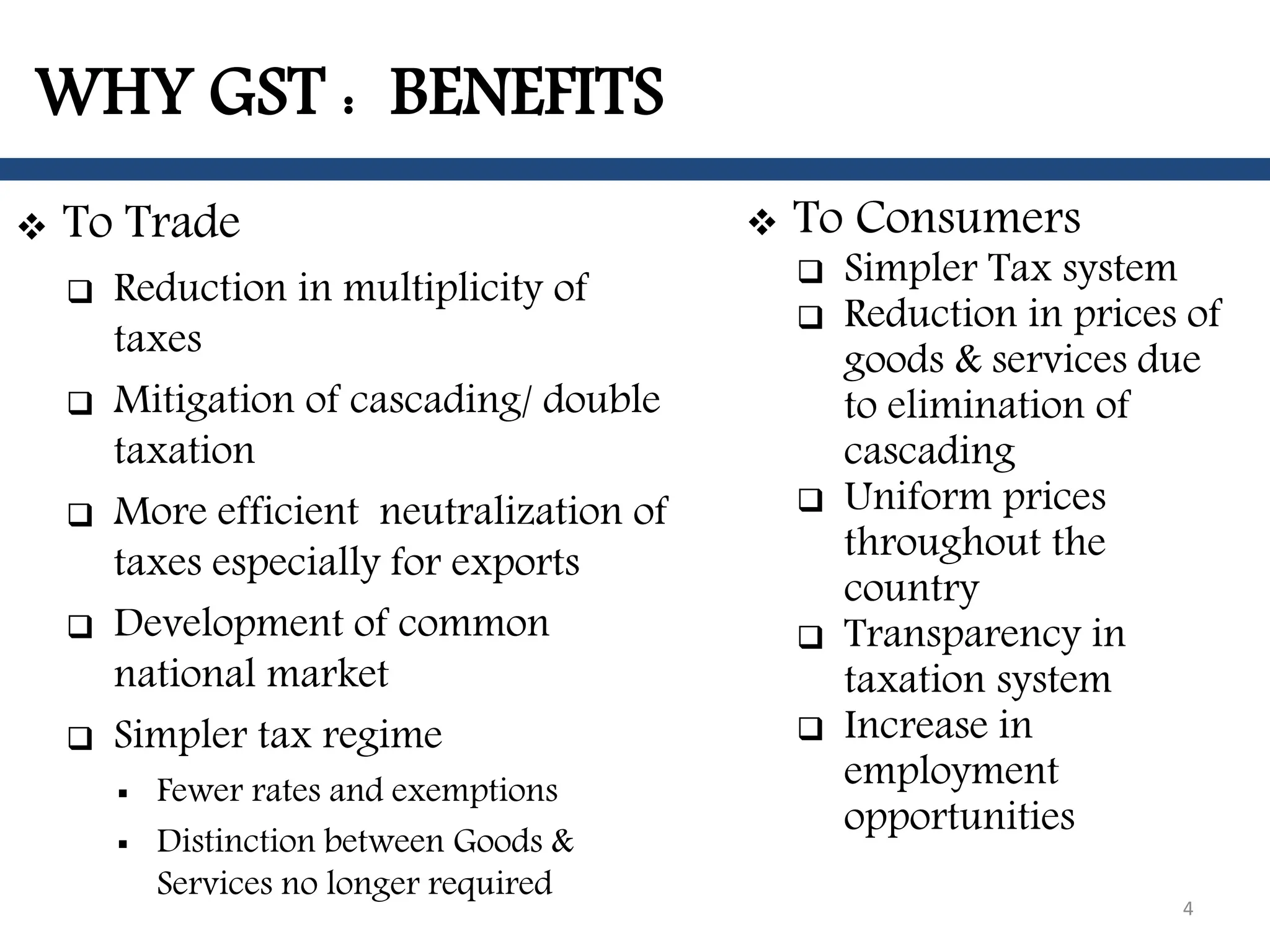

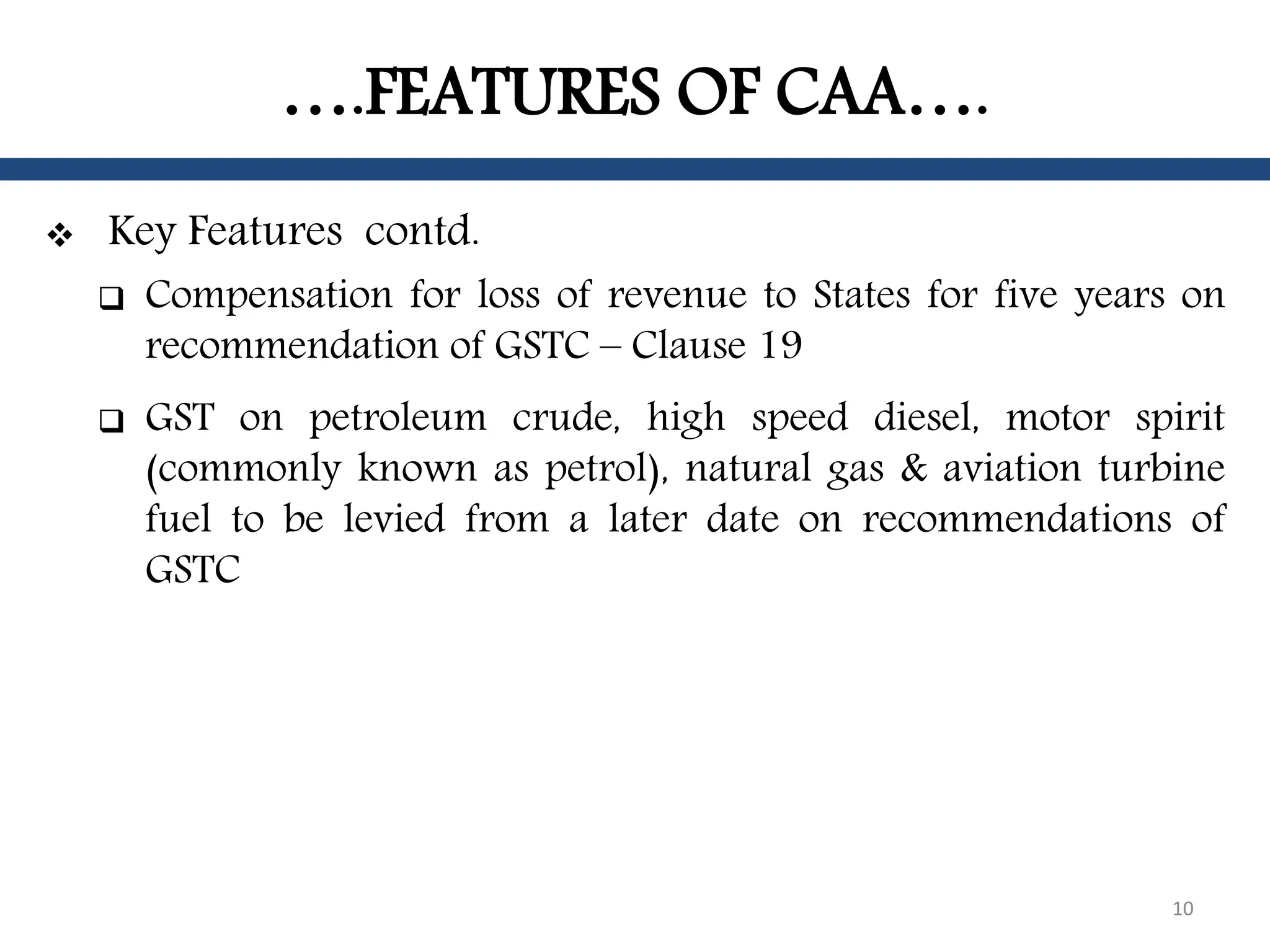

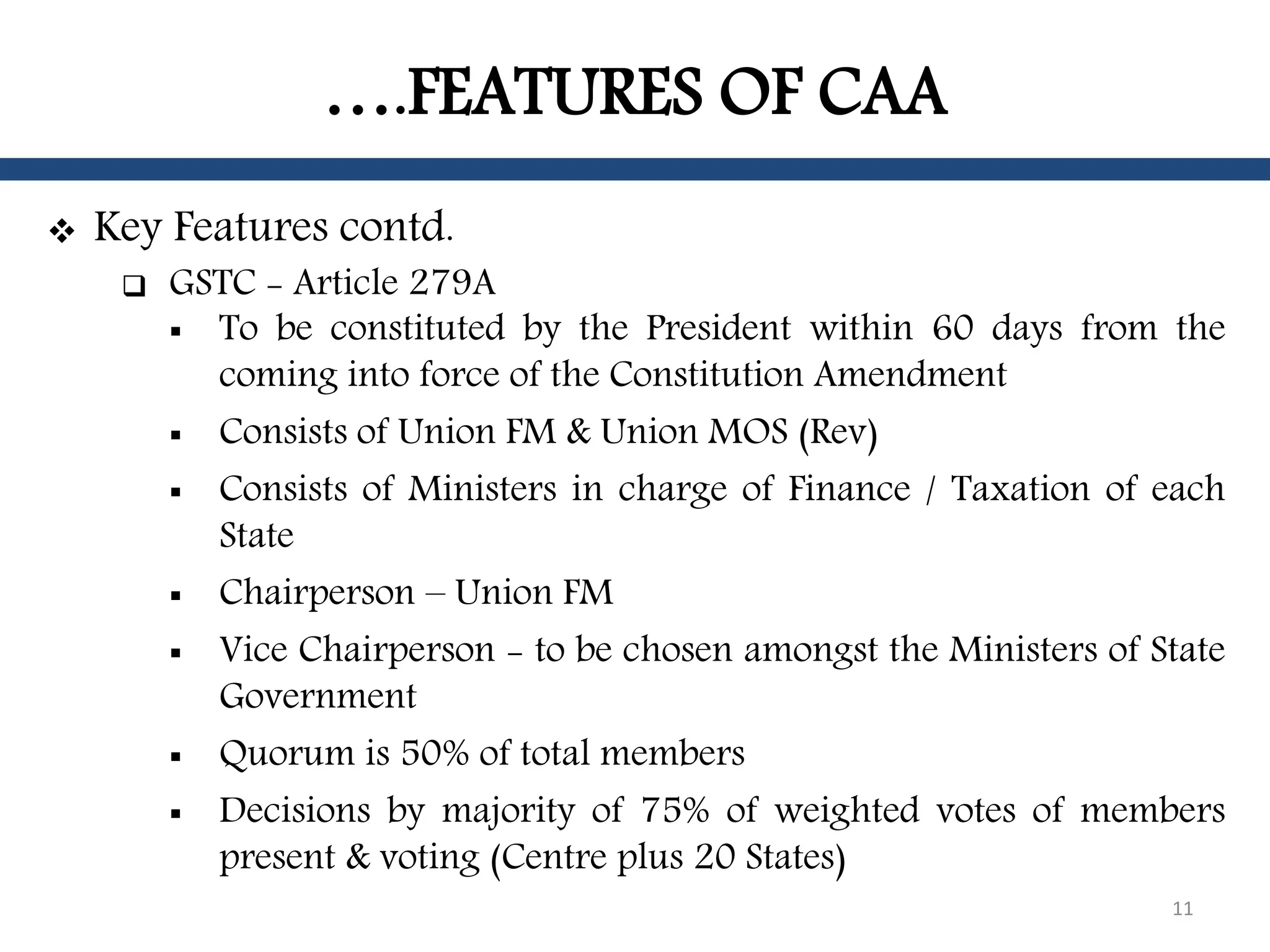

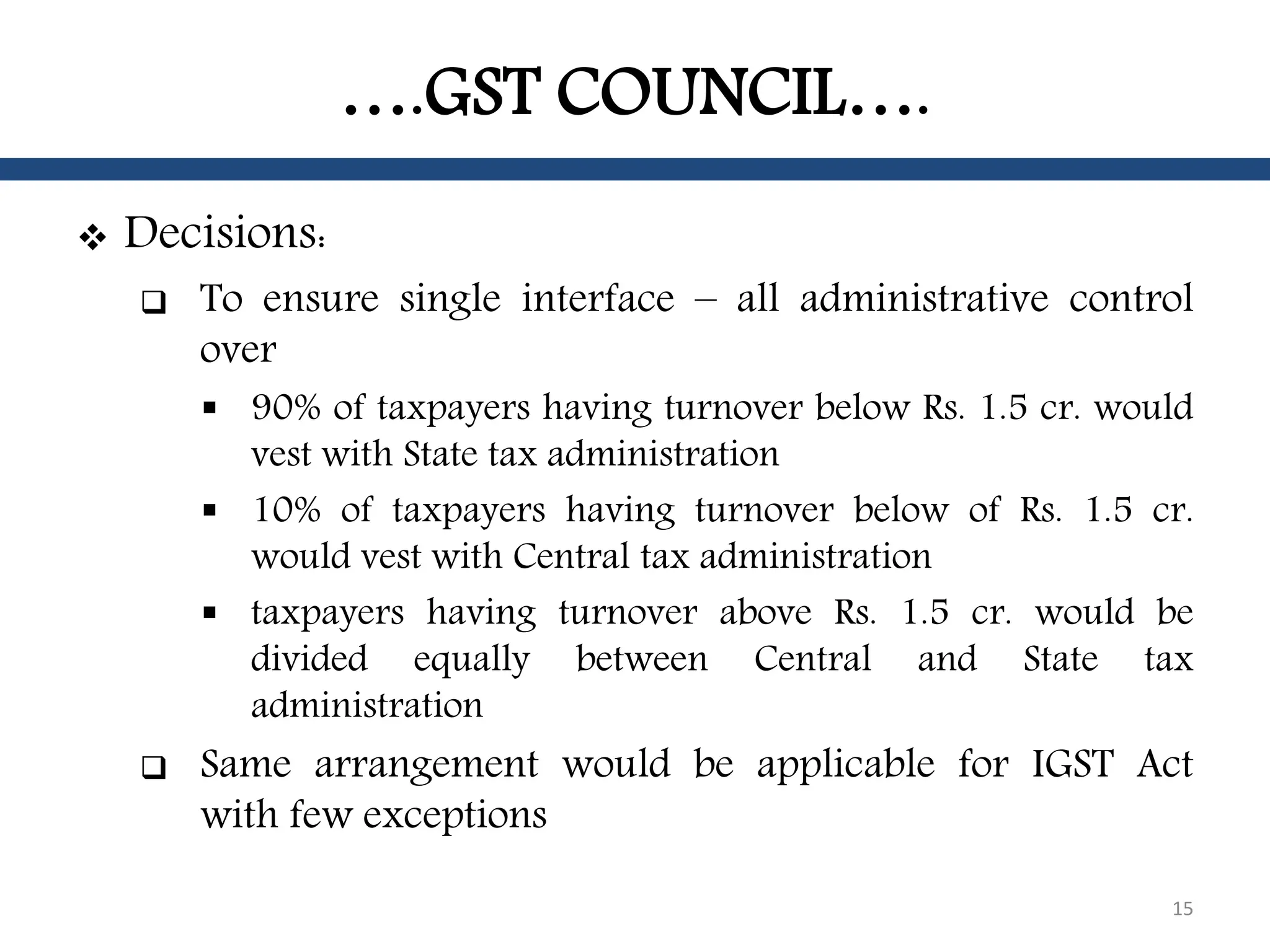

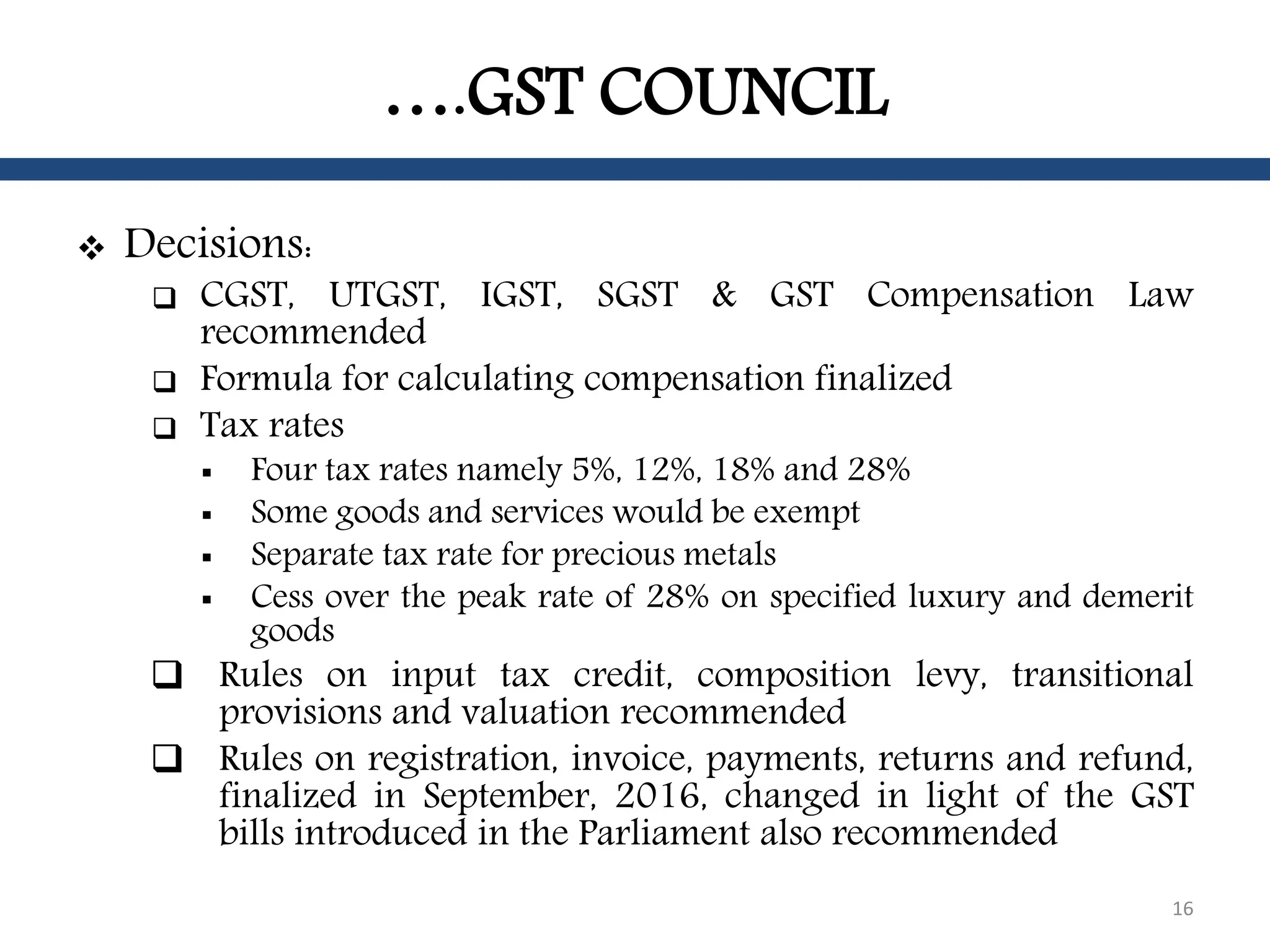

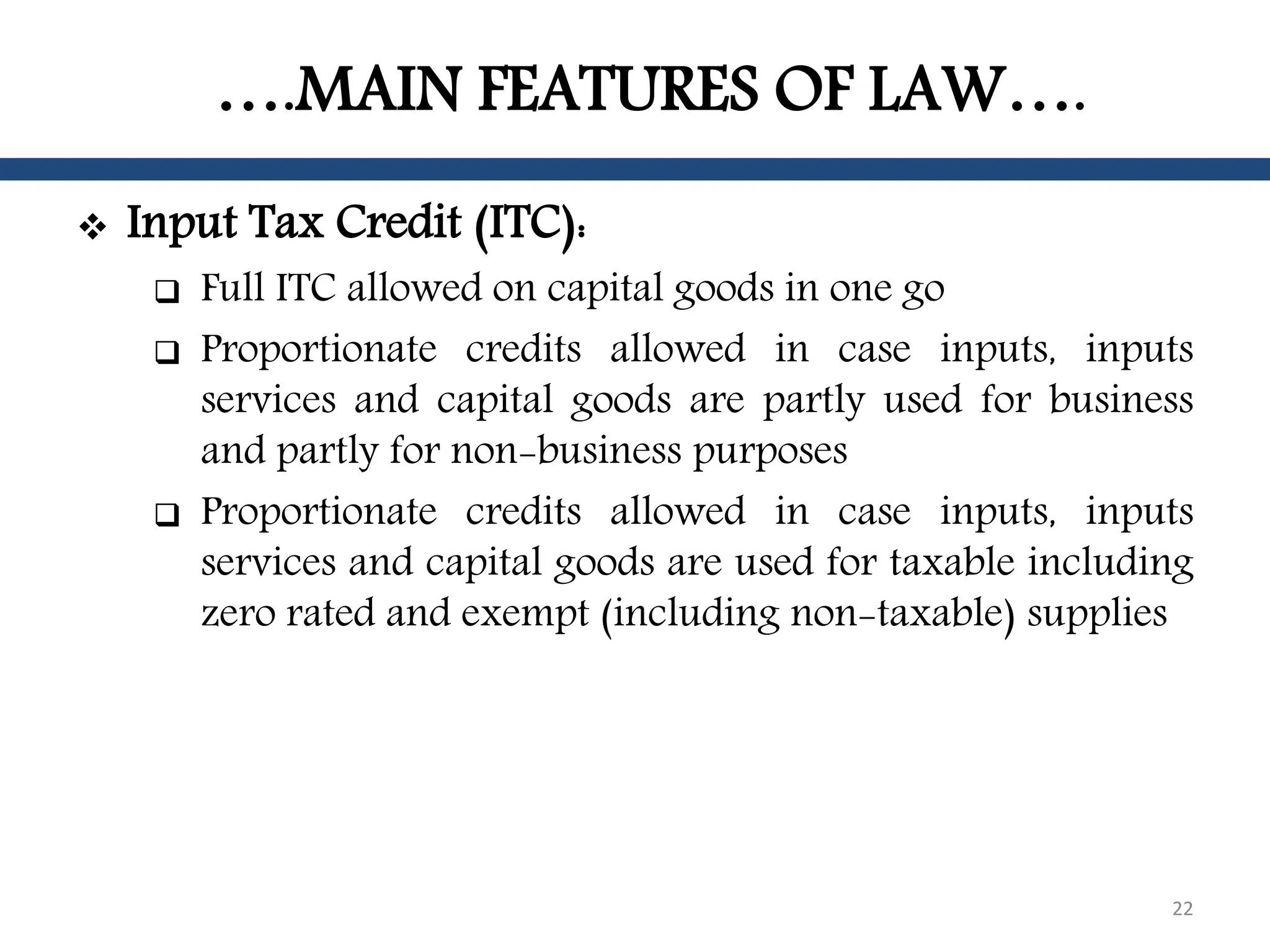

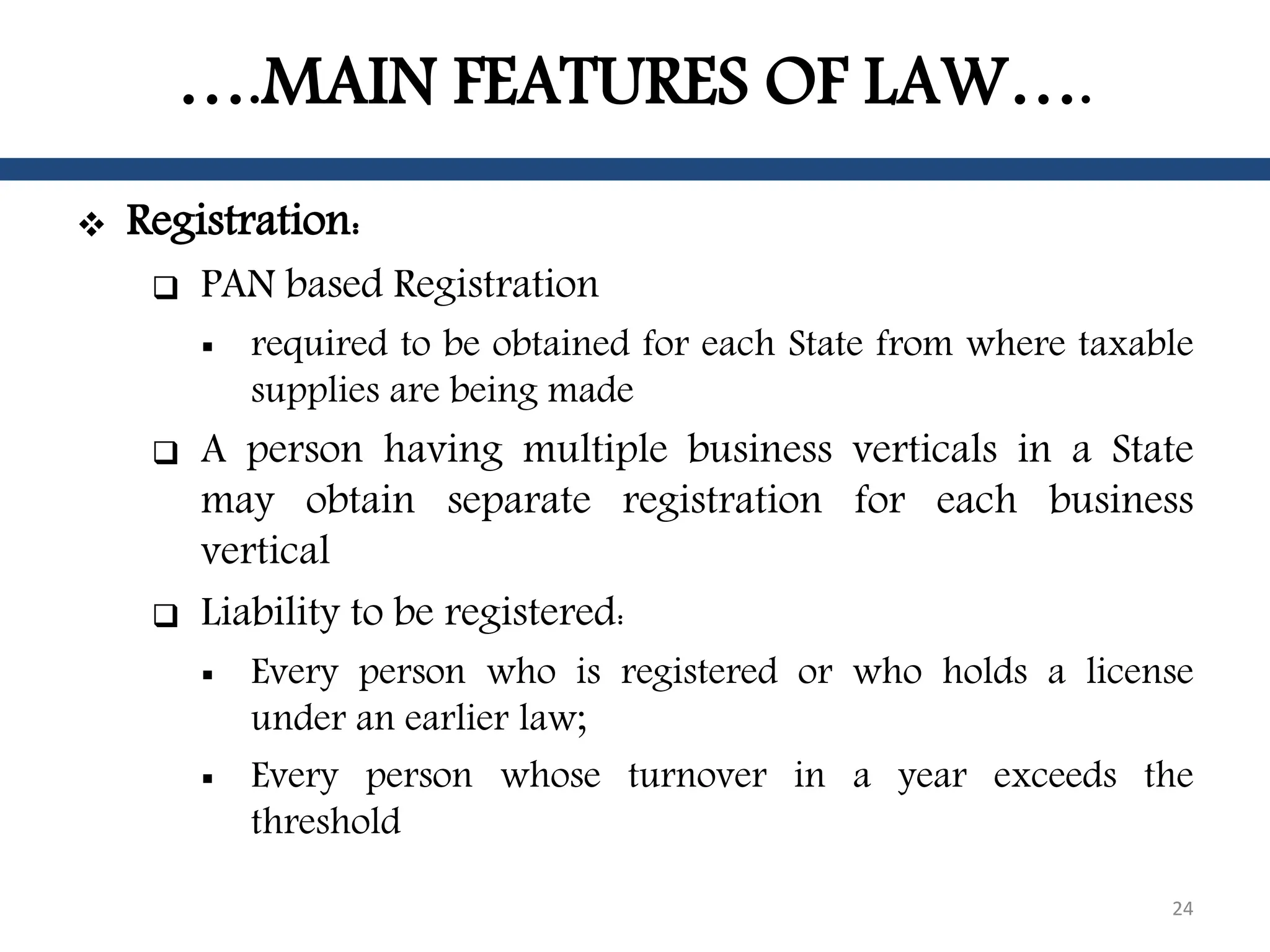

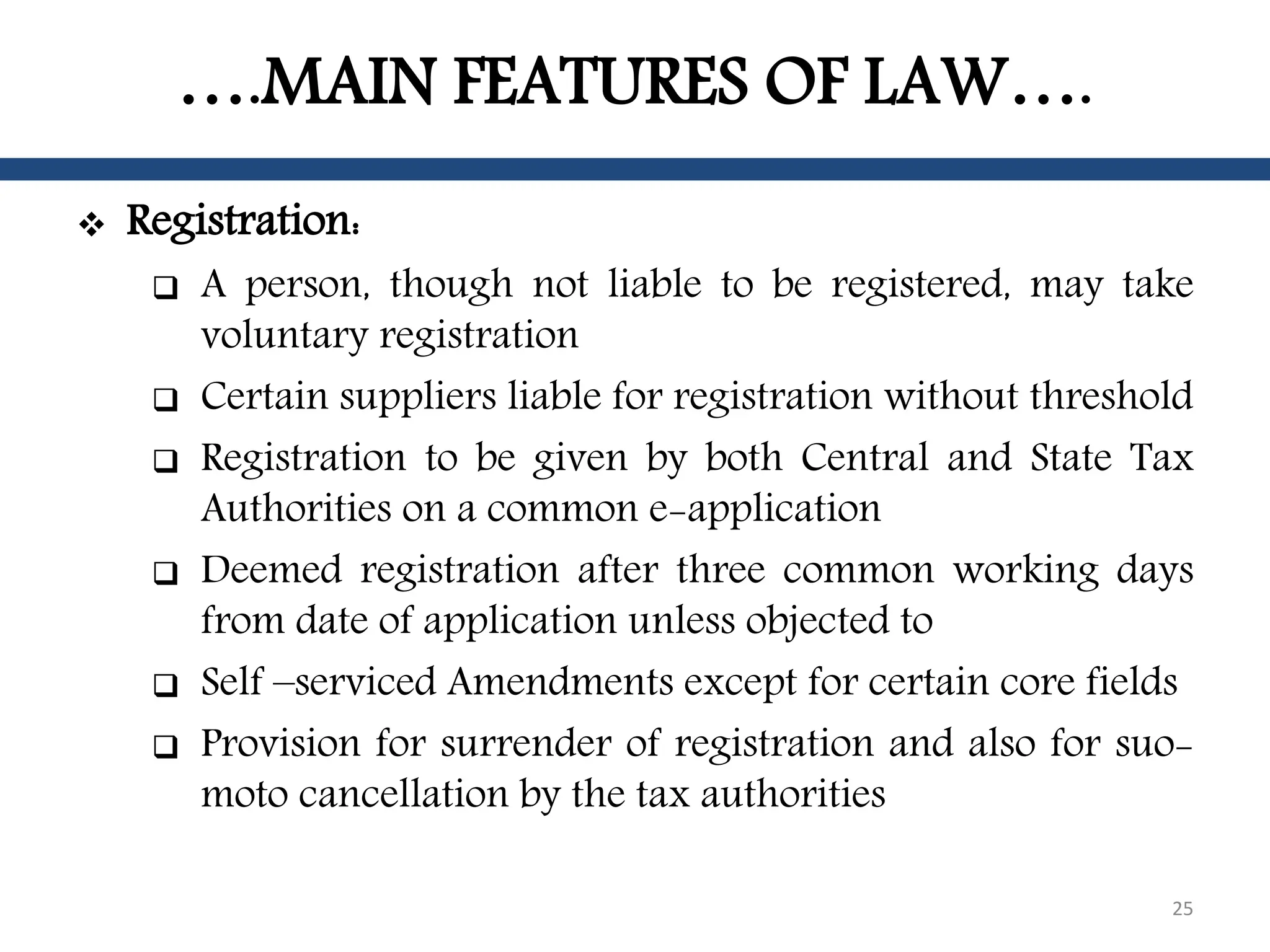

The document outlines the introduction of Goods and Services Tax (GST) in India, highlighting its benefits such as reducing the multiplicity of taxes, creating a common national market, and providing a simpler tax regime for both traders and consumers. It details the constitutional amendments required for its implementation, the formation of the GST council, its decision-making structure, and the primary features of the GST law including tax rates, input tax credits, and registration processes. Additionally, it emphasizes the role of the GST Network (GSTN) and the Central Board of Excise and Customs (CBEC) in the operationalization and regulation of the GST system.