Download to read offline

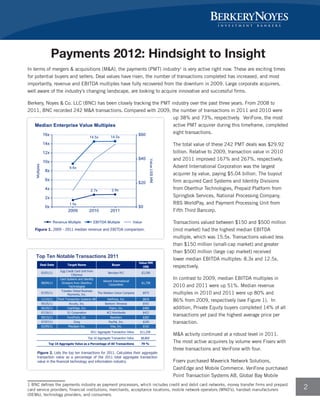

The document summarizes M&A activity and valuations in the payments industry from 2008-2011 based on data from Berkery, Noyes & Co. It finds that the number and value of M&A transactions increased substantially after 2009 and median revenue and EBITDA multiples also increased sharply. The top 10 deals by value in 2011 accounted for 79% of total transaction value that year. It also identifies factors that drive higher valuations for payments companies, such as controlling infrastructure, satisfying demands of consumers and merchants, extending products to new markets, and leveraging existing infrastructure. Finally, it discusses trends in the industry like growth in mobile payments, opportunities in emerging markets, new strategic partnerships, and effects of regulations.