Paul Maynard , the Pensions Minister spells out his intent on open DB schemes

•

0 likes•172 views

Paul Maynard , the Pensions Minister spells out his intent on open DB schemes

Recommended

Recommended

More Related Content

Similar to Paul Maynard , the Pensions Minister spells out his intent on open DB schemes

Similar to Paul Maynard , the Pensions Minister spells out his intent on open DB schemes (20)

More from Henry Tapper

More from Henry Tapper (20)

Recently uploaded

Recently uploaded (20)

Paul Maynard , the Pensions Minister spells out his intent on open DB schemes

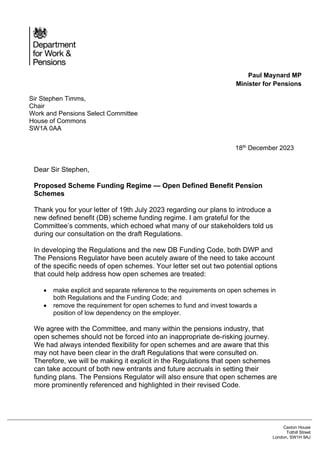

- 1. Sir Stephen Timms, Chair Work and Pensions Select Committee House of Commons SW1A 0AA Paul Maynard MP Minister for Pensions 18th December 2023 Caxton House Tothill Street London, SW1H 9AJ Dear Sir Stephen, Proposed Scheme Funding Regime — Open Defined Benefit Pension Schemes Thank you for your letter of 19th July 2023 regarding our plans to introduce a new defined benefit (DB) scheme funding regime. I am grateful for the Committee’s comments, which echoed what many of our stakeholders told us during our consultation on the draft Regulations. In developing the Regulations and the new DB Funding Code, both DWP and The Pensions Regulator have been acutely aware of the need to take account of the specific needs of open schemes. Your letter set out two potential options that could help address how open schemes are treated: • make explicit and separate reference to the requirements on open schemes in both Regulations and the Funding Code; and • remove the requirement for open schemes to fund and invest towards a position of low dependency on the employer. We agree with the Committee, and many within the pensions industry, that open schemes should not be forced into an inappropriate de-risking journey. We had always intended flexibility for open schemes and are aware that this may not have been clear in the draft Regulations that were consulted on. Therefore, we will be making it explicit in the Regulations that open schemes can take account of both new entrants and future accruals in setting their funding plans. The Pensions Regulator will also ensure that open schemes are more prominently referenced and highlighted in their revised Code.

- 2. However, we do not believe that there is a need for separate arrangements, or indeed a separate regime, for open schemes. Although some schemes may technically be considered to be ‘open’ as they are admitting small numbers of new members, they are still nevertheless maturing, much like a closed scheme. To provide a separate regime for such schemes would leave the system open to inappropriate gaming and may not effectively protect members’ benefits, which is a fundamental cornerstone of our proposals. In the proposed regulations, the need to de-risk will be explicitly linked to the extent to which the scheme is currently or is likely to become more mature in the future, as well as on the strength of the sponsoring employer. This scheme specific approach ensures that if an open scheme is not maturing, it will not get closer to the point at which it is expected to become significantly mature and will not therefore have to move towards low dependency. Therefore, where appropriate, open schemes can continue to invest in a significant proportion of long-term productive assets. The Scheme Funding and Investment Strategy Regulations will be laid before Parliament in the New Year. Please be reassured that we will be publishing a full impact assessment alongside the Regulations and the Government response to our consultation. I would like to thank you and the Committee again for your input. Yours sincerely, Paul Maynard MP Minister for Pensions

- 3. 19 July 2023 Laura Trott MBE MP Minister for Pensions Department for Work and Pensions (By e-mail only) Dear Laura, Proposed new funding regime—open DB schemes We are grateful for your commitment to take account of the Committee’s conclusions and recommendations in deciding how to proceed with proposals to introduce a new funding regime legislated for under the Pension Schemes Act 2021 (s123).1 You told us on 12 July 2023 that you intended to look again at the proposals and come with a decision on how to proceed, hopefully in the autumn.2 Concerns about the potential impact on open schemes were debated when the legislation was before Parliament in November 2020. The then Pensions Minister, Guy Opperman MP, said that “open schemes with a strong sponsoring employer that are immature and have managed their risk appropriately should not be forced into an inappropriate de-risking journey.” He said the Government committed to ensuring that: The secondary legislation works in a way that does not prevent appropriate open schemes from investing in riskier investments where there are potentially higher returns as long as the risks can be supported and members’ benefits and the Pension Protection Fund are effectively protected.3 The evidence we have received to our current inquiry on Defined Benefit Pension Schemes, and our previous one on Defined benefit pensions with LDI, suggests the Government has not effectively delivered on this commitment in the draft guidance. In our view, the Government must do so, to help achieve two important objectives: • Enabling pension schemes to invest in the UK economy. It is clear from the Chancellor’s Mansion House speech on 10 July and your comments following the speech, that the Government is keen for pension schemes to invest in the UK economy where this is consistent with providing the best possible outcome to pension scheme 1 Q304, 22 March 2023 2 10.30am 3 PBC Deb 5 November 2020 c80

- 4. House of Commons Palace of Westminster London SW1A 0AA workpencom@parliament.uk +44 (0)20 219 8976 Social: @CommonsWorkPen parliament.uk members.4 We agree. Open schemes do invest in the UK economy. They are concerned that the funding code will limit their ability to do so. • Supporting people to achieve adequate incomes in retirement. As we noted in our Report on Saving for Later Life, people who have access to a defined benefit (DB) pension are much more likely to be on course for an adequate income in retirement, than those who do not.5 Concerns In our Report on Defined Benefit Pension Schemes with Liability Driven Investments, we noted concern that the proposals could exacerbate existing trends for scheme closures and difficulties supporting the Government’s growth agenda.6 It is clear from evidence to our current inquiry on DB schemes that these concerns persist.7 A core concern with the current proposals is the requirement on open schemes to define and fund towards a target of having low dependency on the sponsoring employer, even when they are not expected to mature in the foreseeable future.8 This would require them to de-risk, increasing the cost of ongoing DB accrual unnecessarily, potentially making it more expensive for employers (and in shared cost schemes, such as the railways’ and universities’ schemes, also employees). This could have the effect of accelerating scheme closures. XPS Pensions Group said it was seeing this “limit the ability for sponsors to argue for following higher-returning strategies even with other contingent protections (guarantees and securities) being in place.”9 The Universities Superannuation Scheme (USS) told us that it was concerned both about the drafting of the new rules and how they might be applied: over time, as significantly mature schemes become the norm, and regulatory and policy knowledge and experience is built around de-risked schemes at or near their ‘end- game’, inappropriate expectations or requirements of remaining open schemes and their sponsors might be set.10 A compelling reason to revisit the proposals is to ensure they are appropriate to the circumstances of today. Since the inception of the policy in 2016, the overall trend has been for 4 Chancellor Jeremy Hunt’s Mansion 5 Protection pension savers: five years on from the pension freedoms: Saving for Later Life, Work and Pensions Committee, June 2023, para 26 6 Defined benefit pension schemes with Liability Driven Investments, Work and Pensions Select Committee, June 2023, paras 144 and 149 7 DBP0054 (PLSA); DBP0063 (Railways Pension Trustee Company Limited); DBP0078 (Universities Superannuation Scheme) 8 DBP0063 (Railway Pension Scheme Trustee Company Ltd) 9 XPS Pensions Group, DBP0041 10 DBP0078 (Universities Superannuation Scheme)

- 5. House of Commons Palace of Westminster London SW1A 0AA workpencom@parliament.uk +44 (0)20 219 8976 Social: @CommonsWorkPen parliament.uk aggregate scheme funding levels to improve.11 In addition, the cost of building up new benefits in a DB scheme has fallen, by around 5%, from 20–25% to 10–15%, in the case of the Railways Pension Schemes.12 This provides a new and more favourable environment in which it is easier for employers to keep schemes open. This opportunity must not be undermined by a new funding regime which increases costs unnecessarily.13 Options We understand that two things would help address these concerns: • Explicit and separate reference to the requirements on open schemes in both Regulations and the Funding Code; and • Removing the requirement for open schemes to fund and invest towards a position of low dependency on the employer.14 There are important reasons to justify a different approach for open schemes: • Where they remain open at a time that most have closed, this is because the sponsoring employer(s) has taken an active decision to keep them open on the grounds that it meets their needs or those of their workforce.15 • A pipeline of new and younger members means assets do not need to be liquid and a far longer investment horizon is possible. In fact, where supported by a strong employer covenant, open DB schemes are able to carry long-term risks as part of their investment strategy, even as they approach maturity.16 Some witnesses before us argued that more is needed: for example, that The Pensions Regulator (TPR) should have a new objective to have regard to future build-up of benefits rather than just to protect benefits already built-up. We will explore this further as our inquiry proceeds. 11 PPF 7800 index – June 2023, Chart 1. 12 Q21 Oral evidence to the Work and Pensions Select Committee 21 June 2023 13 Q15 Oral evidence to the Work and Pensions Select Committee 21 June 2023 14 Supplementary evidence (Railway Pension Scheme Trustee Company Ltd); DBP0078 (Universities Superannuation Scheme); DBP0054 (Pension and Lifetime Savings Association) 15 DBP0078 (Universities Superannuation Scheme); Q17 [Joe Dabrowski] 16 Pensions and Growth, PLSA, June 2023; Q17-18

- 6. House of Commons Palace of Westminster London SW1A 0AA workpencom@parliament.uk +44 (0)20 219 8976 Social: @CommonsWorkPen parliament.uk In our LDI Report, we recommended that you should publish a full impact assessment of the current proposals, including the impact on financial stability and on open DB schemes.17 This is still needed to allow a more fundamental review of the policy, which we heard many are concerned will increase ‘herding’ in investment strategies. We hope that these comments are helpful to you as you continue to develop the new funding regime. As is usual practice with the Committee’s correspondence, I will be publishing this letter and your response on the Committee’s website. Yours sincerely, Rt Hon Sir Stephen Timms MP Chair, Work and Pensions Committee 17 Defined benefit pension schemes with Liability Driven Investments, Work and Pensions Select Committee, June 2023