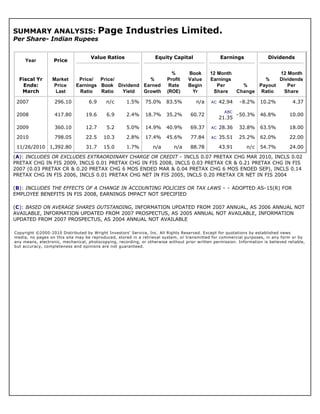

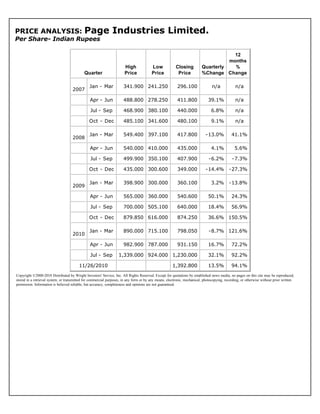

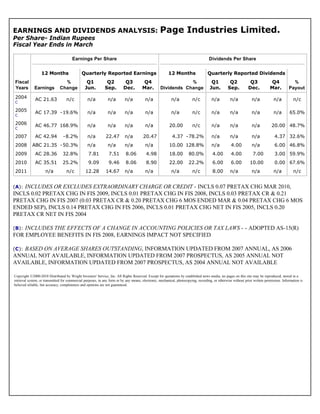

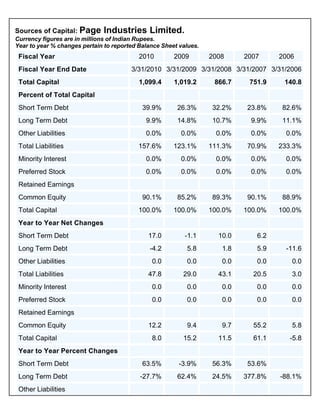

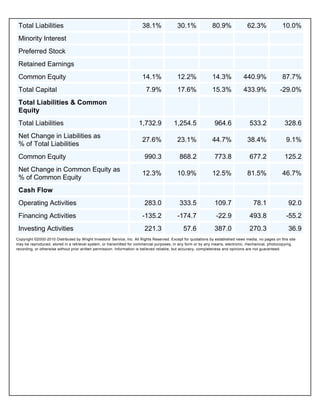

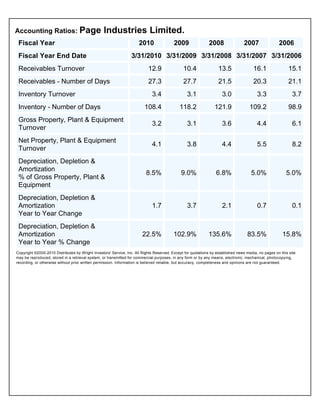

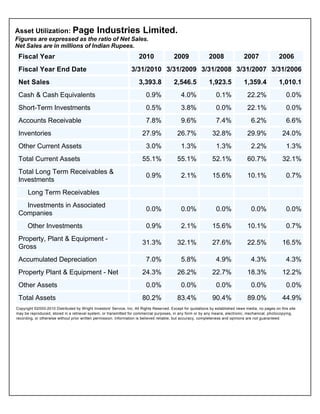

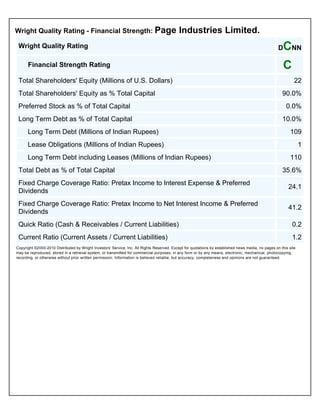

Page Industries Limited is an India-based manufacturer of garments. It holds the license to manufacture and distribute JOCKEY branded innerwear and leisurewear in India and surrounding countries. According to a recent analysis, Page Industries has experienced strong sales growth and increasing profitability in recent years. However, its stock valuation ratios are high relative to competitors in the apparel manufacturing industry.

![Company FundamentalsComparative Business Analysis

A Wright Investors' Service Research Report:

Page Industries Limited.

440 Wheelers Farms Road

Provided By CorporateInformation.com Milford, CT 06461 U.S.A.

Wright Comparative Business Analysis Report

Report Date: 11/26/2010

Company Description

Page Industries Limited is an India-based company. It is engaged in the business of manufacturing garments. The

Company is the licensee of JOCKEY International Inc. (USA) for manufacture and distribution of the JOCKEY

brand innerwear/leisurewear for men and women in India, Sri Lanka, Bangladesh and Nepal. Its range of products

include Men's Innerwear, which consists of Zone Stretch, Comfort Stretch, Jockey Gold Edition, Elance, Jockey

Zone, Modern Classic and Boys; its Women's Innerwear consists of Active Bras, Essence Bras, Soft Wonder,

Comfort Stretch, Jockey Comfies and Simple Comfort. The Company Sport and Leisure product consist of Sport

performance, Sport, 24x7 stretch and Socks; Its Thermals product includes both Men's and Women's wear. As of

March 31, 2010, the Company authorized franchisees, opened ten Exclusive Brand Outlets (EBO) and 54 outlets

across the cities of India.

Competitor Analysis

Page Industries Limited. operates in the Men's & boys' underwear & nightwear sector. This analysis compares

Page Industries Limited. with three other companies: K-Lifestyle & Industries Limited (2010 sales of 5.56

billion Indian Rupees [US$125.99 million] of which 100% was Textiles), Pearl Global Limited (2009 sales: 3.87

billion Indian Rupees [US$87.60 million] of which 100% was Readymade Garments), and Birla Cotsyn India

Limited (2010 sales of 3.44 billion Indian Rupees [US$77.92 million] of which 63% was Trading). Note: not all of

these companies have the same fiscal year: the most recent data for each company are being used.

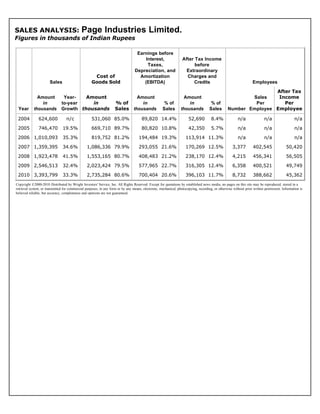

Sales Analysis

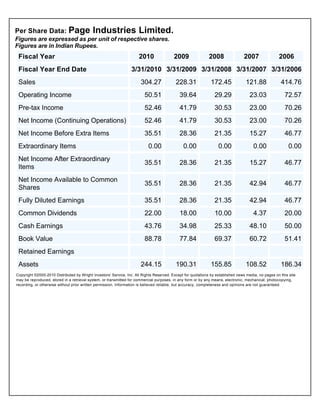

Page Industries Limited. reported sales of 3.39 billion Indian Rupees (US$76.87 million) for the fiscal year ending

March of 2010. This represents an increase of 33.3% versus 2009, when the company's sales were 2.55 billion

Indian Rupees. Sales at Page Industries Limited. have increased during each of the previous five years (and since

2005, sales have increased a total of 355%).

Recent Sales at Page Industries Limited.

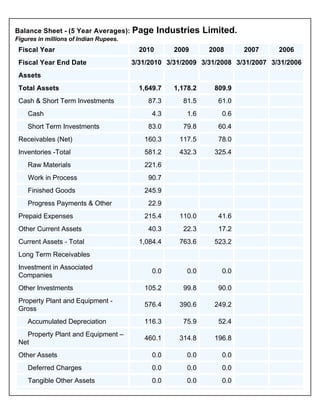

3.39

2.55

1.92

1.36

1.01

0.75

2005 2006 2007 2008 2009 2010

(Figures in Billions of Indian Rupees)

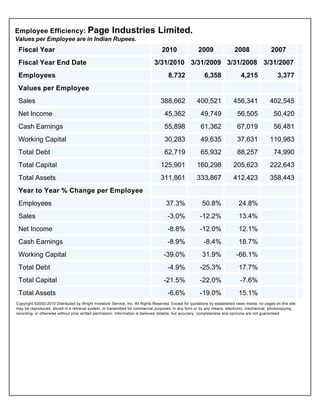

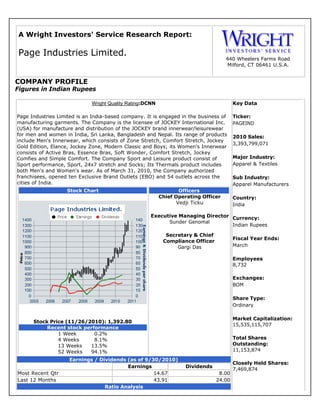

Page Industries Limited. currently has 8,732 employees. With sales of 3.39 billion Indian Rupees (US$76.87

million) , this equates to sales of US$8,803 per employee. This company's employees do not appear to be very

efficient in generating sales.

Sales Comparisons (Most Recent Fiscal Year)

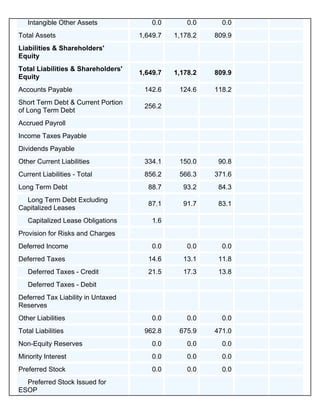

Year Sales Sales Sales/

Company Ended (blns) Growth Emp (US$) Largest Region

Page Industries Limited. Mar 2010 3.394 33.3% 8,803 India (100.0%)

K-Lifestyle & Industries Limited Mar 2010 5.562 11.0% N/A India (100.0%)](https://image.slidesharecdn.com/pageindustries-120517022003-phpapp02/85/Page-industries-3-320.jpg)