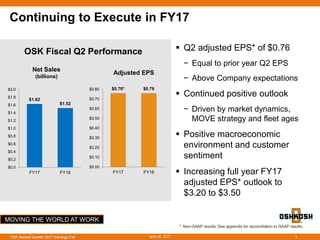

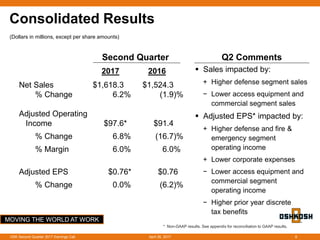

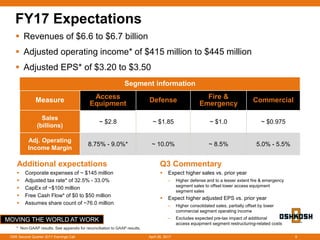

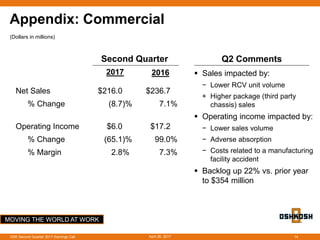

Oshkosh Corporation reported its financial results for the second quarter of fiscal year 2017. Net sales increased 6.2% to $1.618 billion compared to the same period last year, and adjusted earnings per share were $0.76, equal to the prior year. The defense segment performed well due to the JLTV program ramp up and international sales. The access equipment and commercial segments faced challenges with lower sales volumes impacting operating income. For fiscal year 2017, the company increased its adjusted EPS outlook to a range of $3.20 to $3.50.