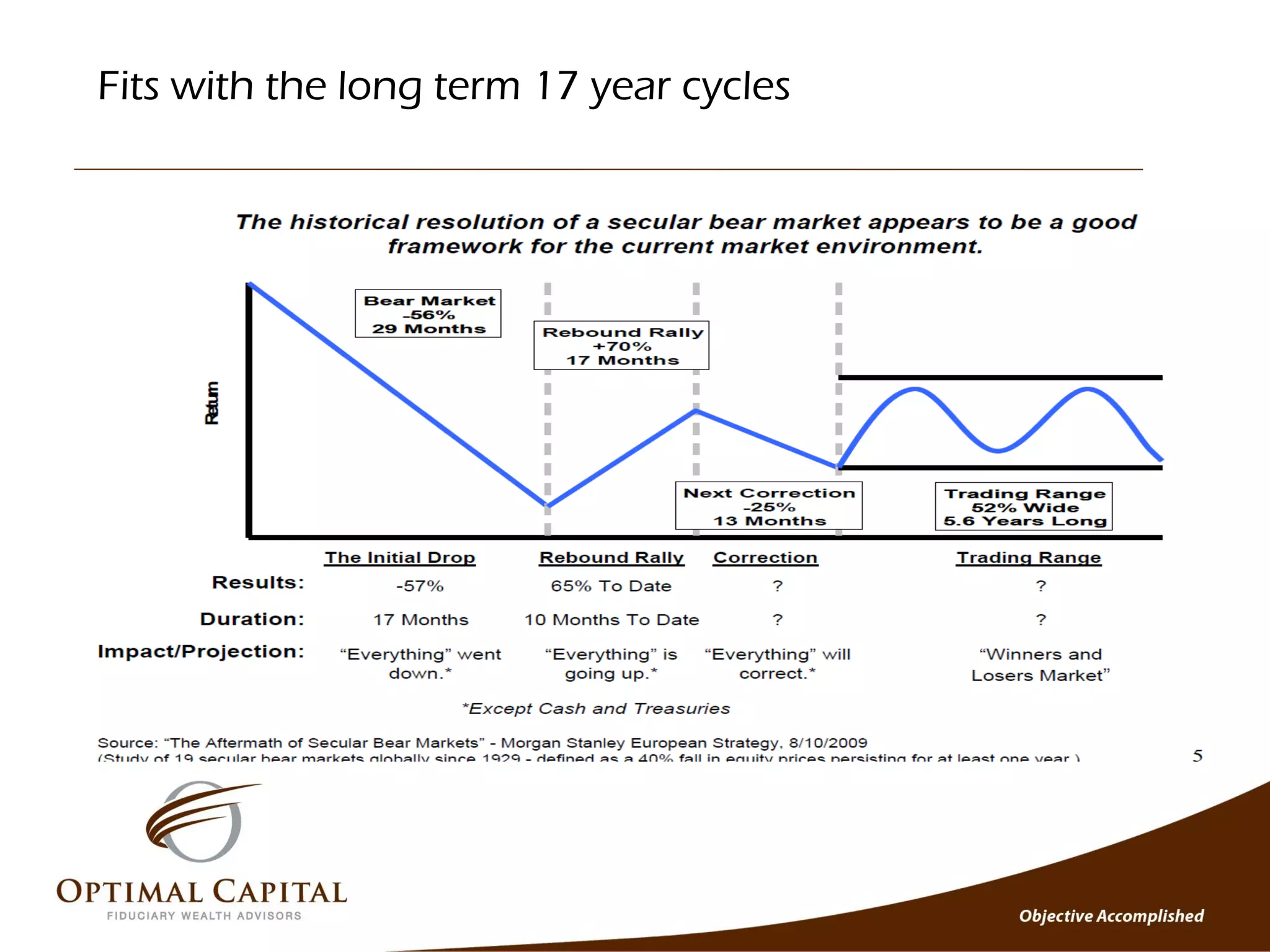

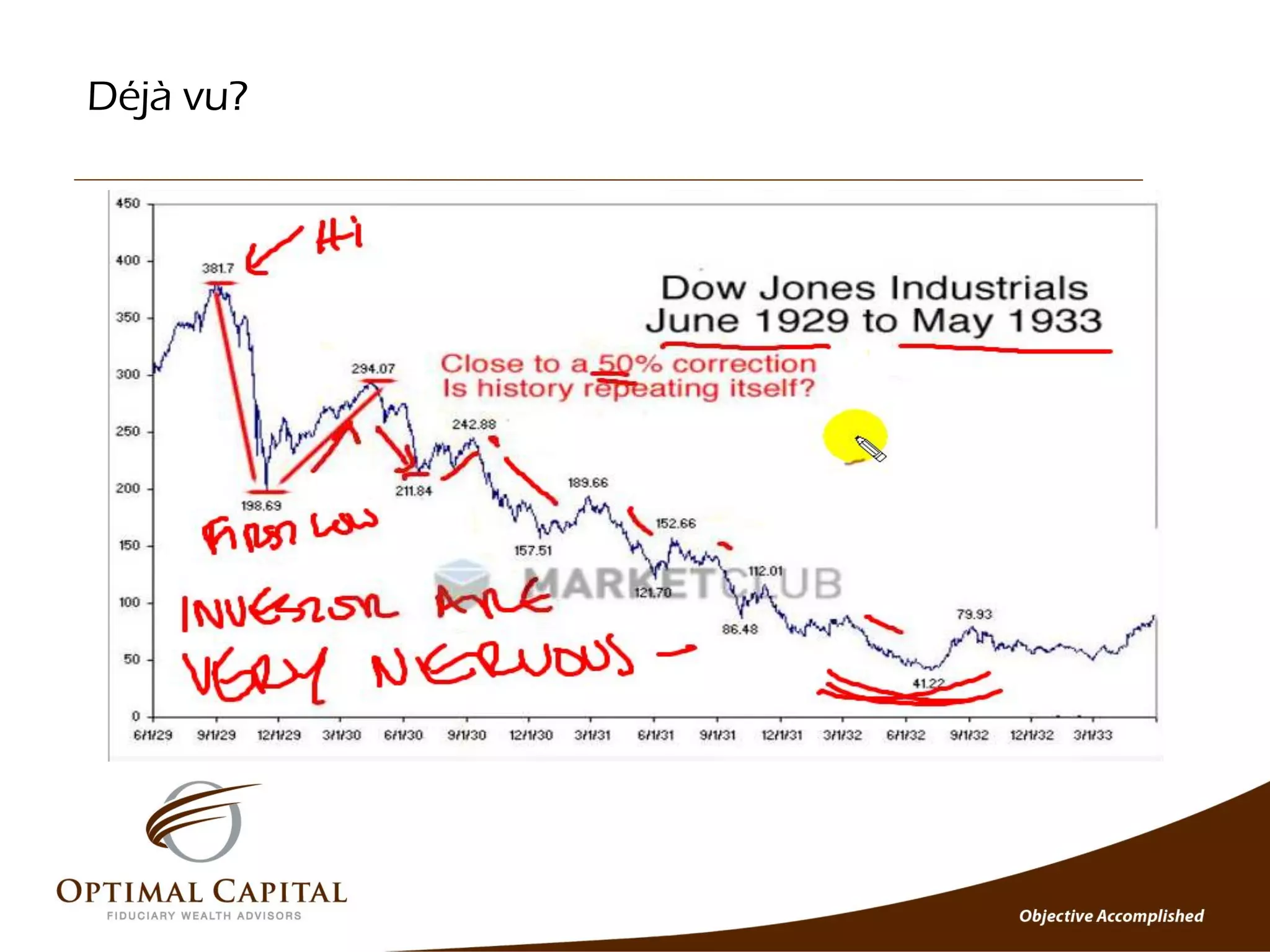

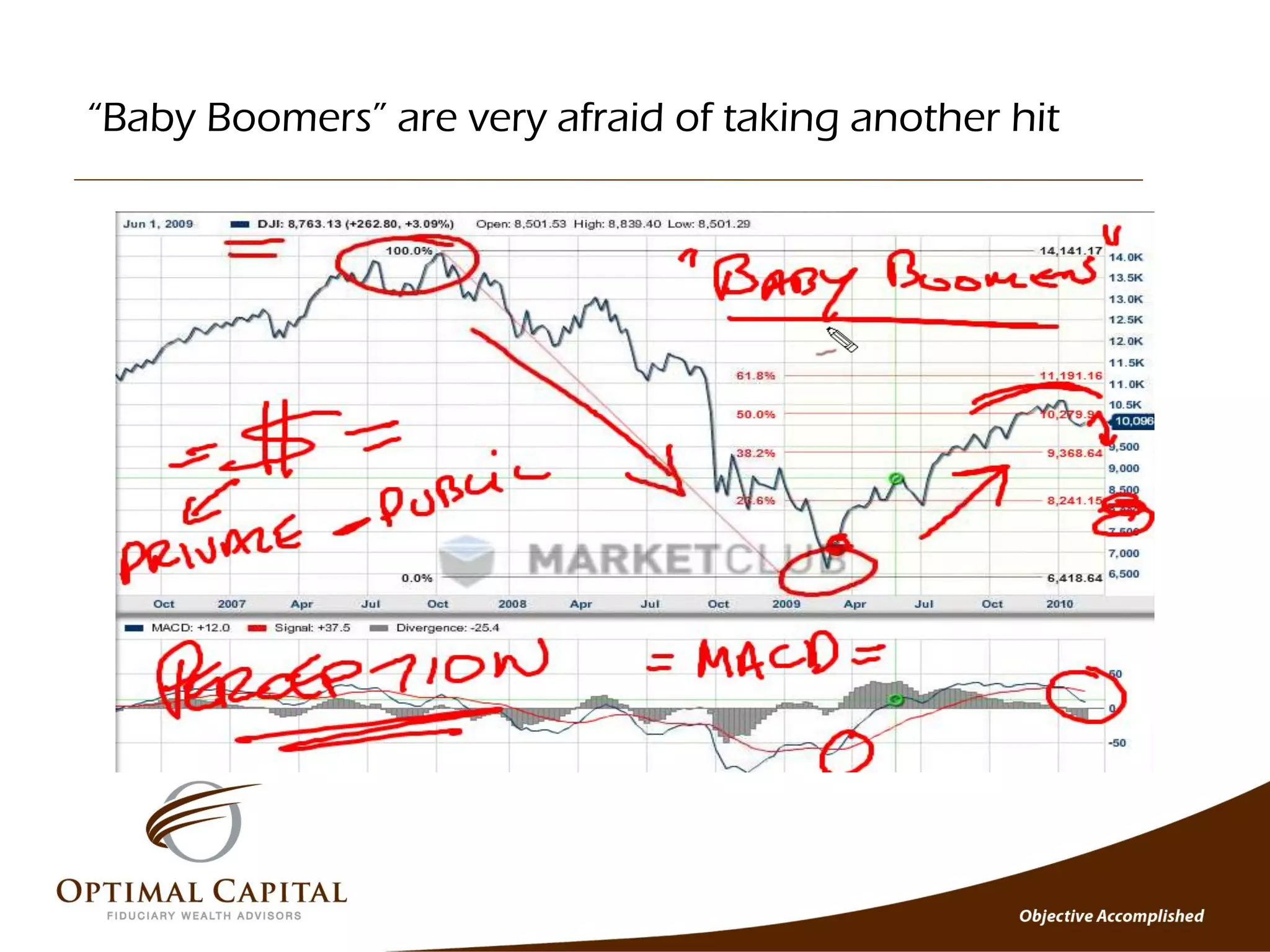

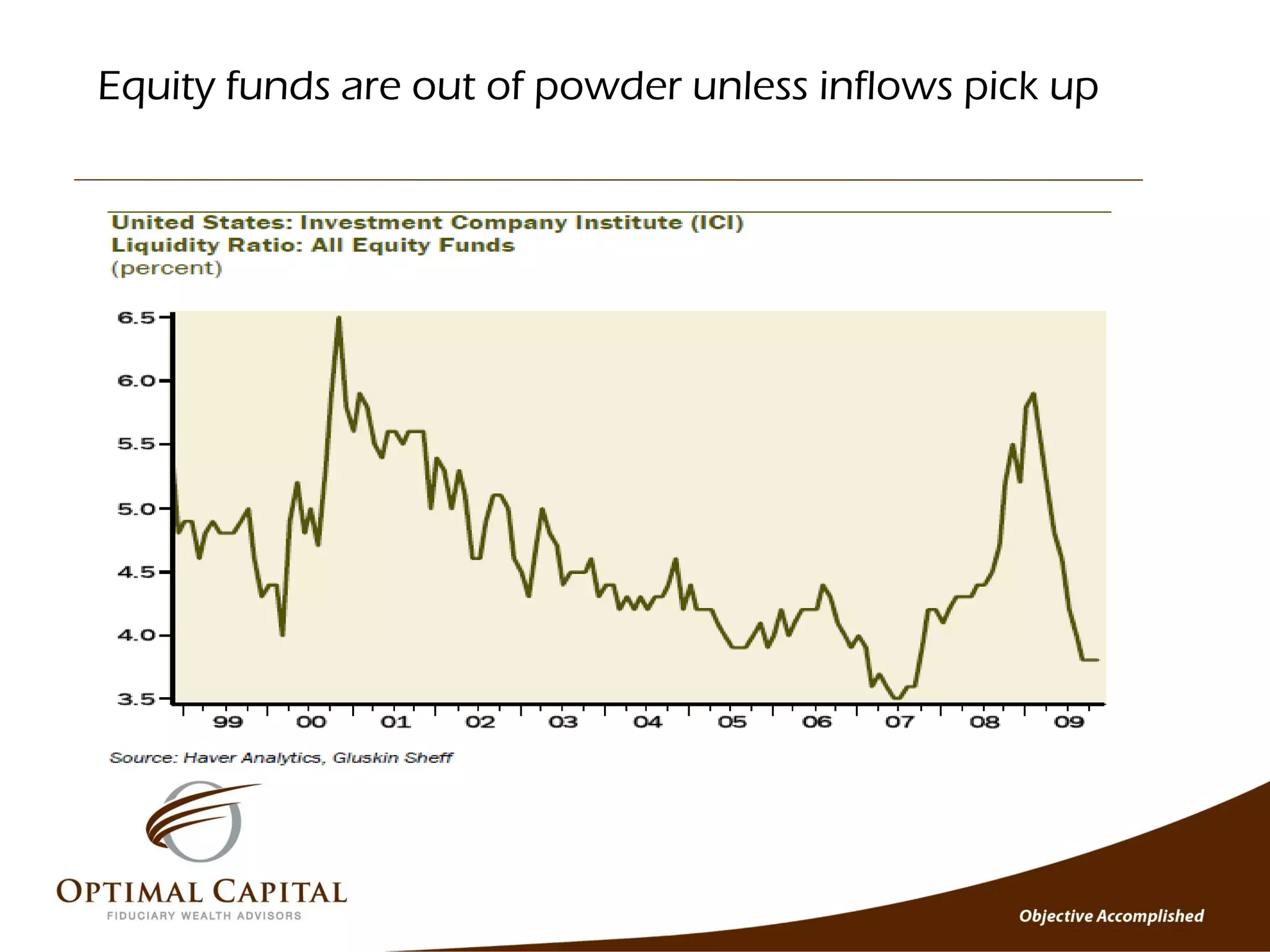

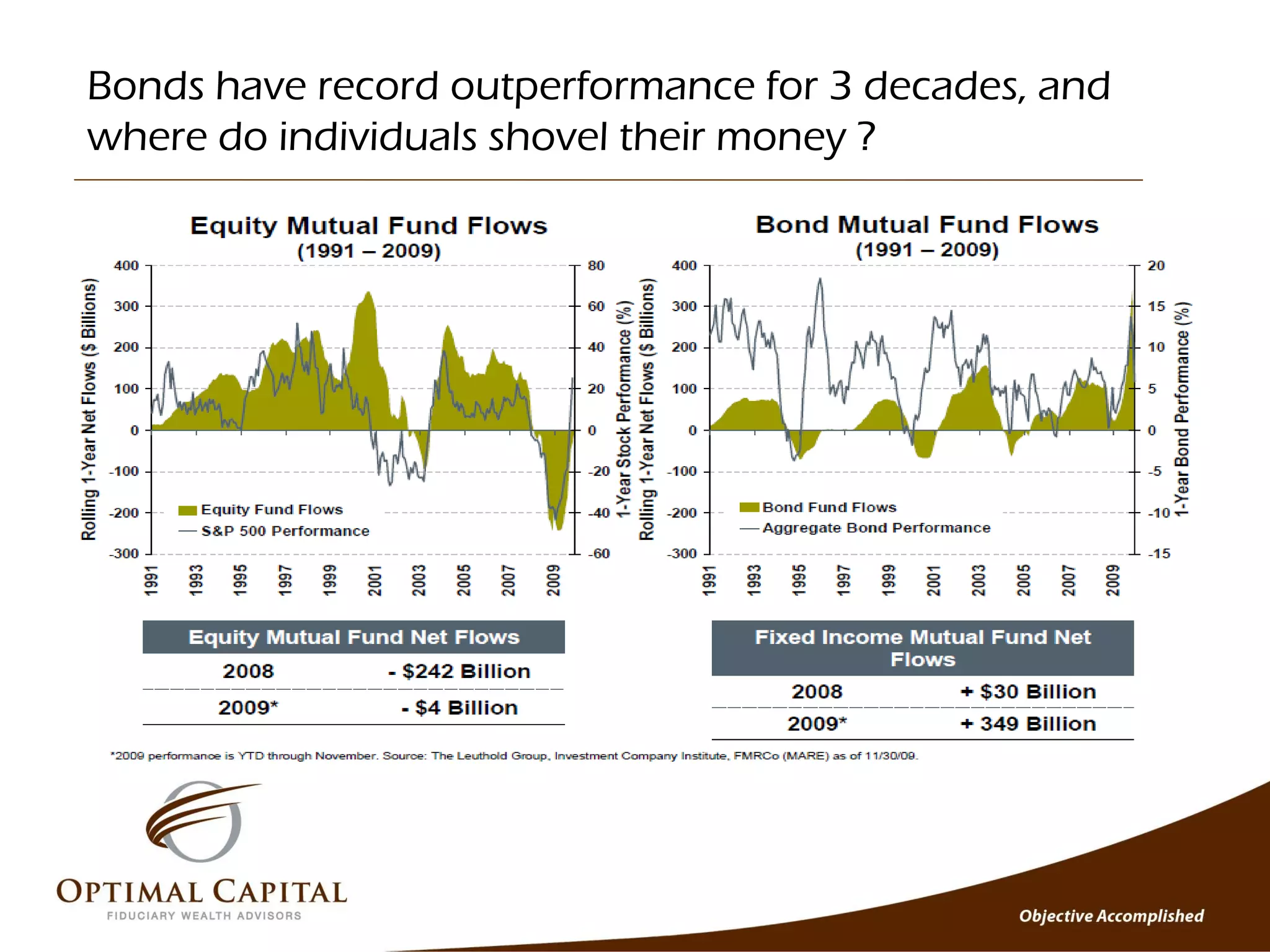

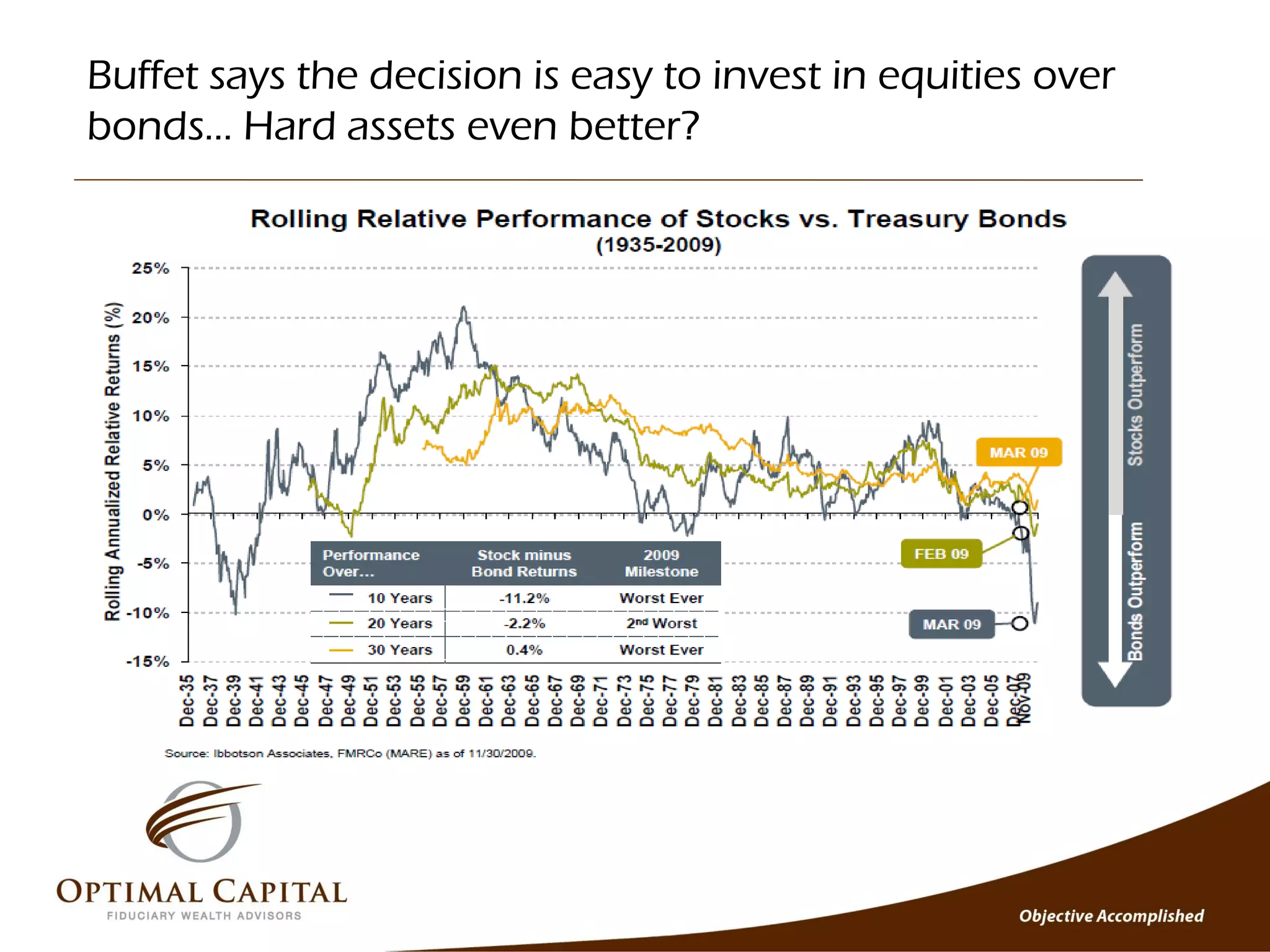

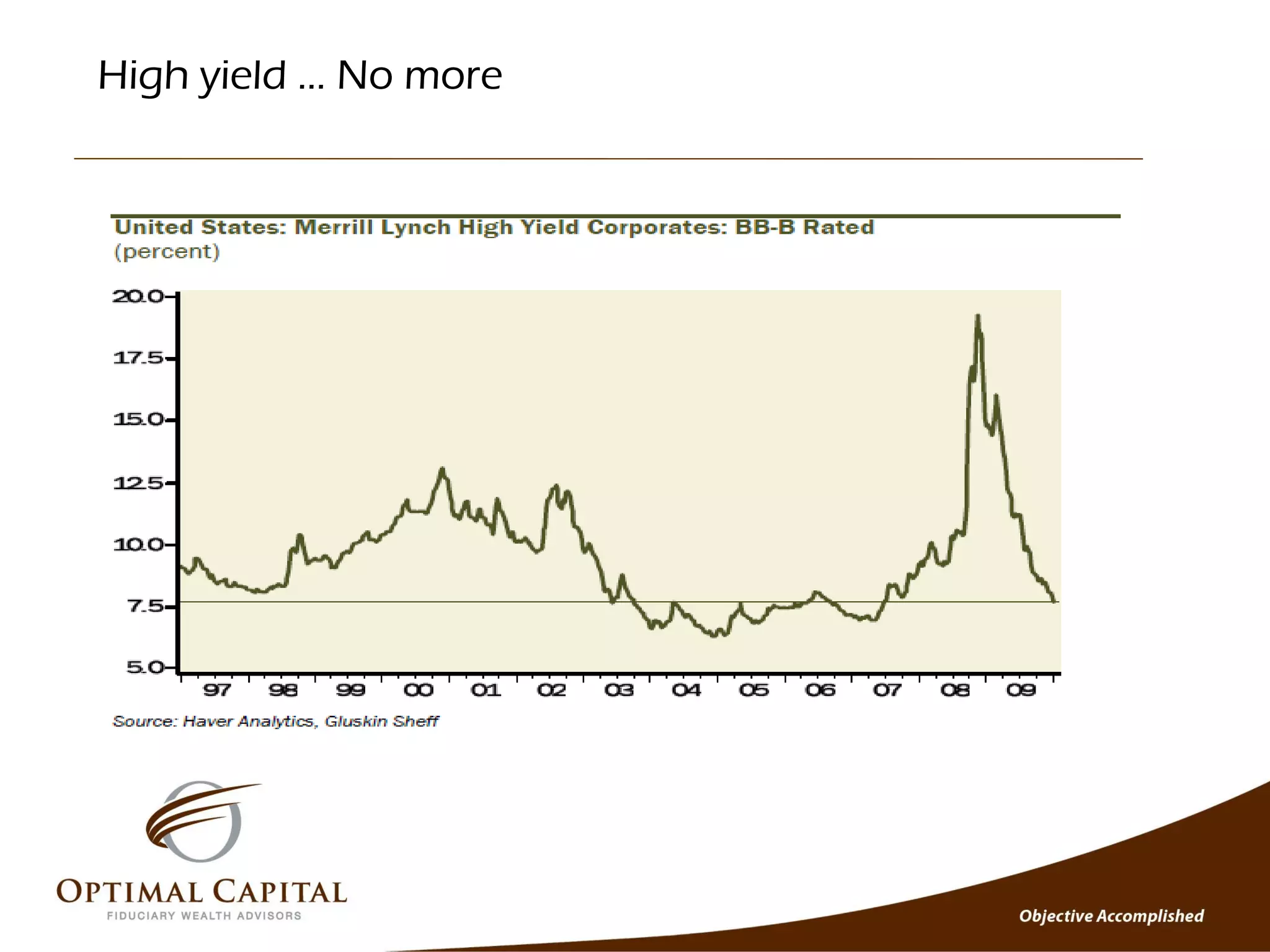

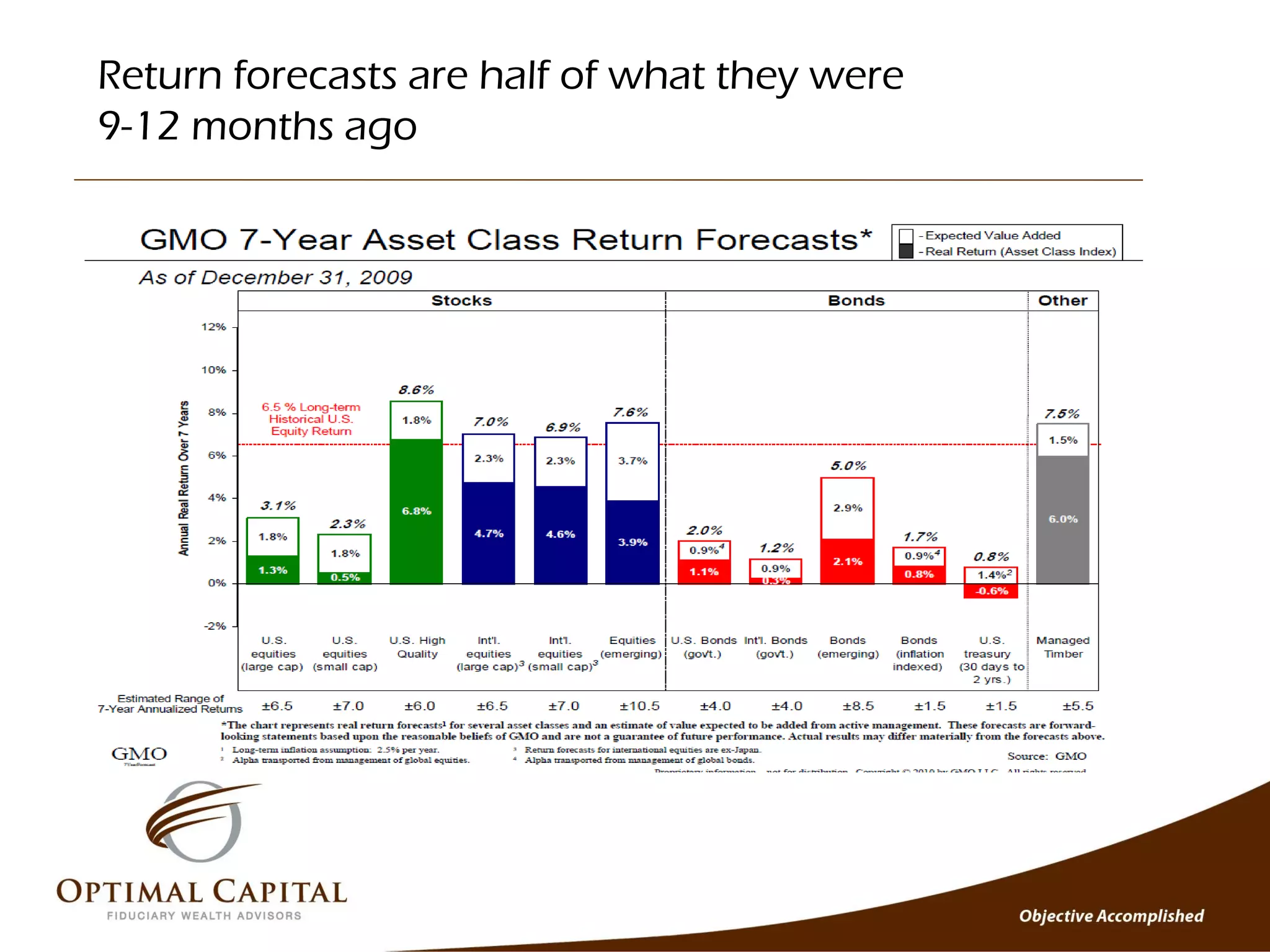

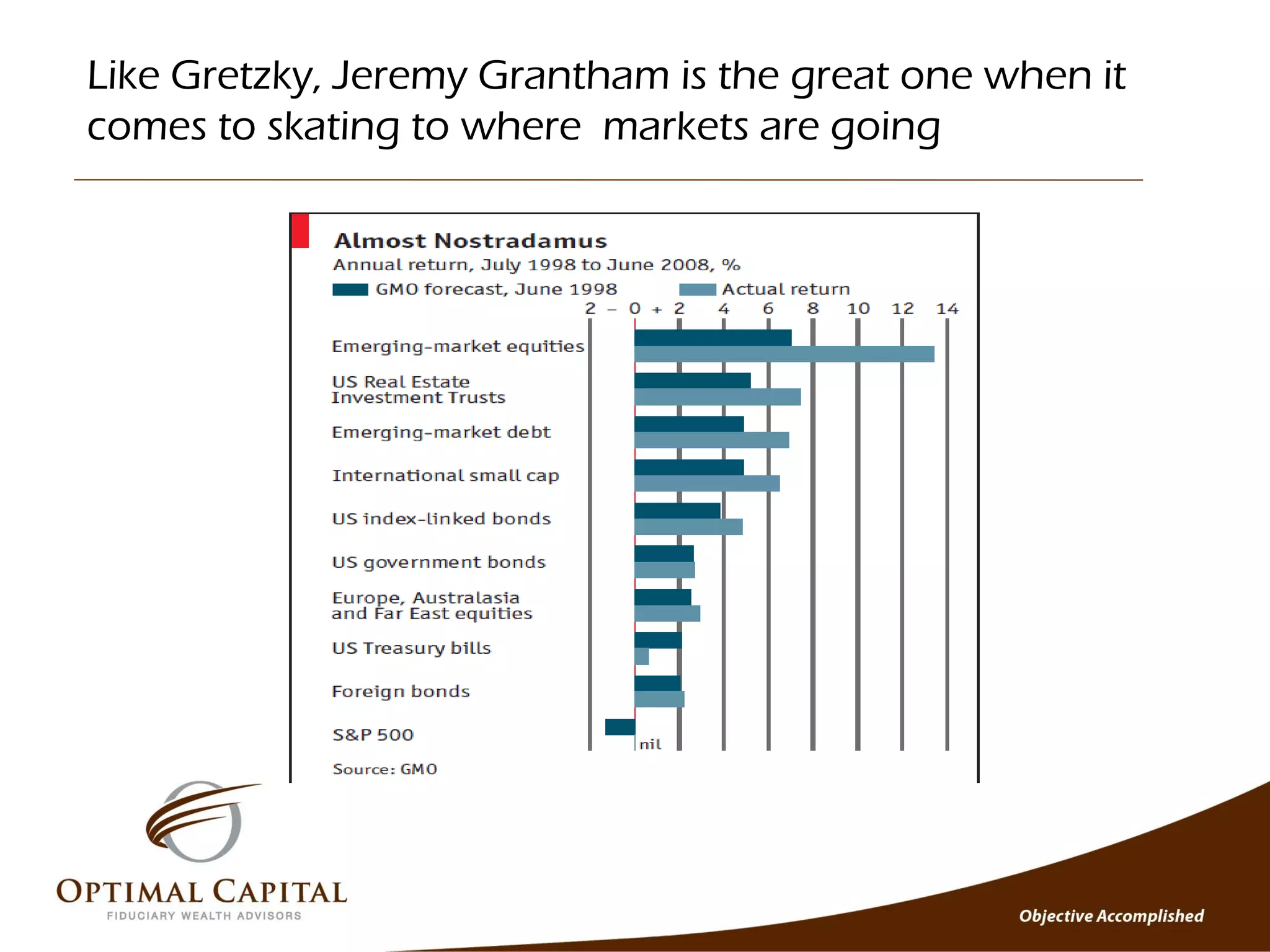

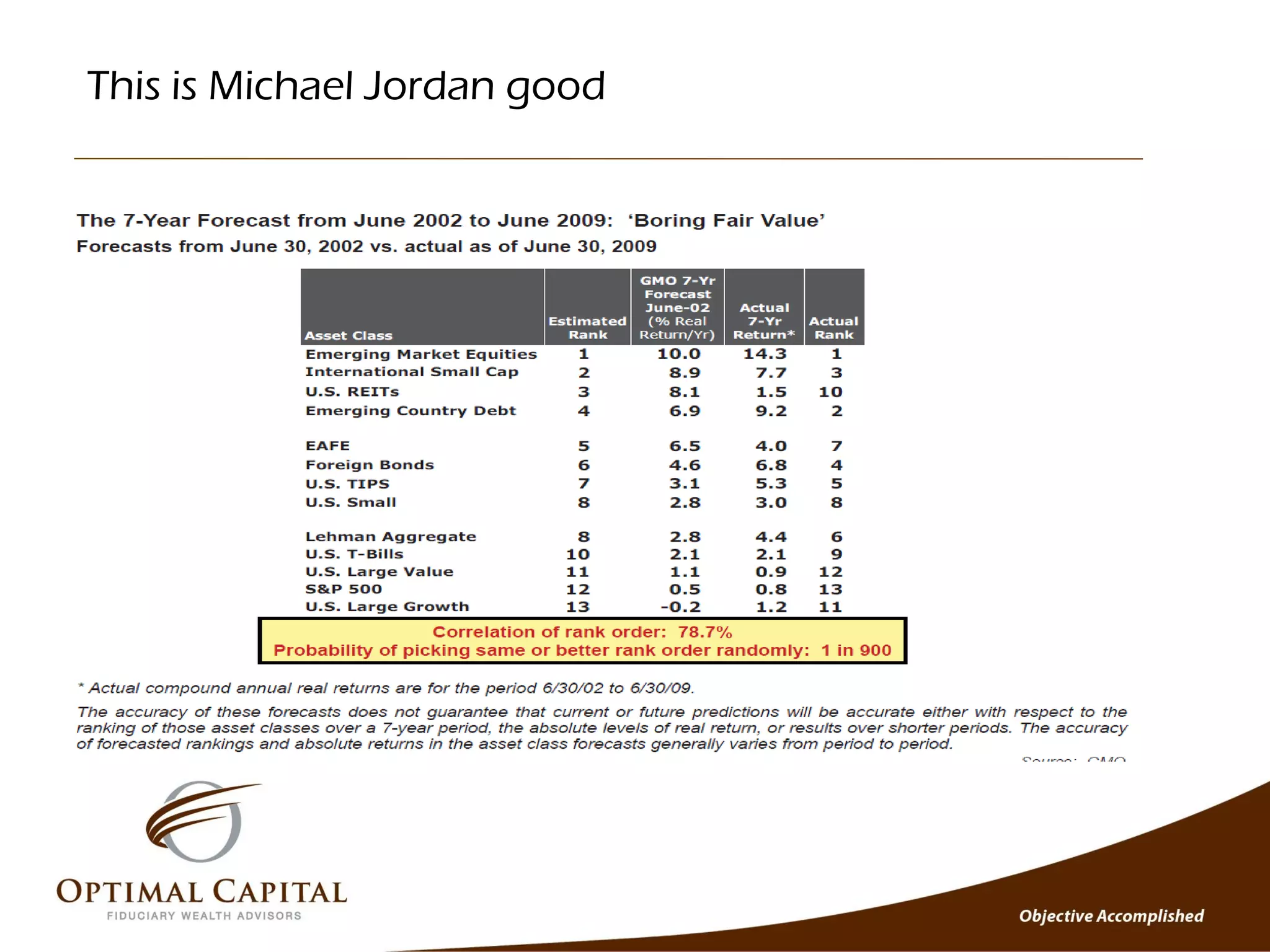

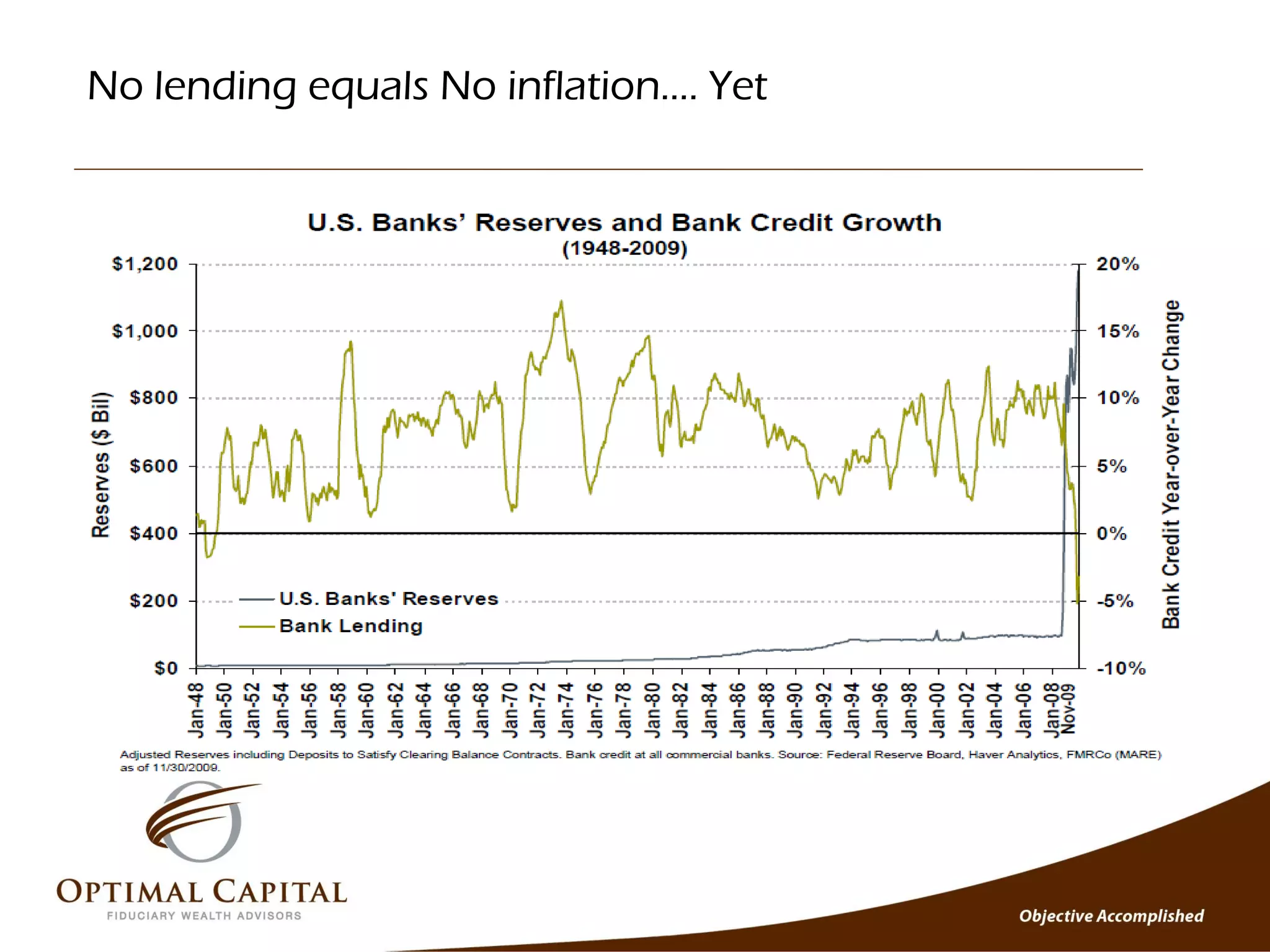

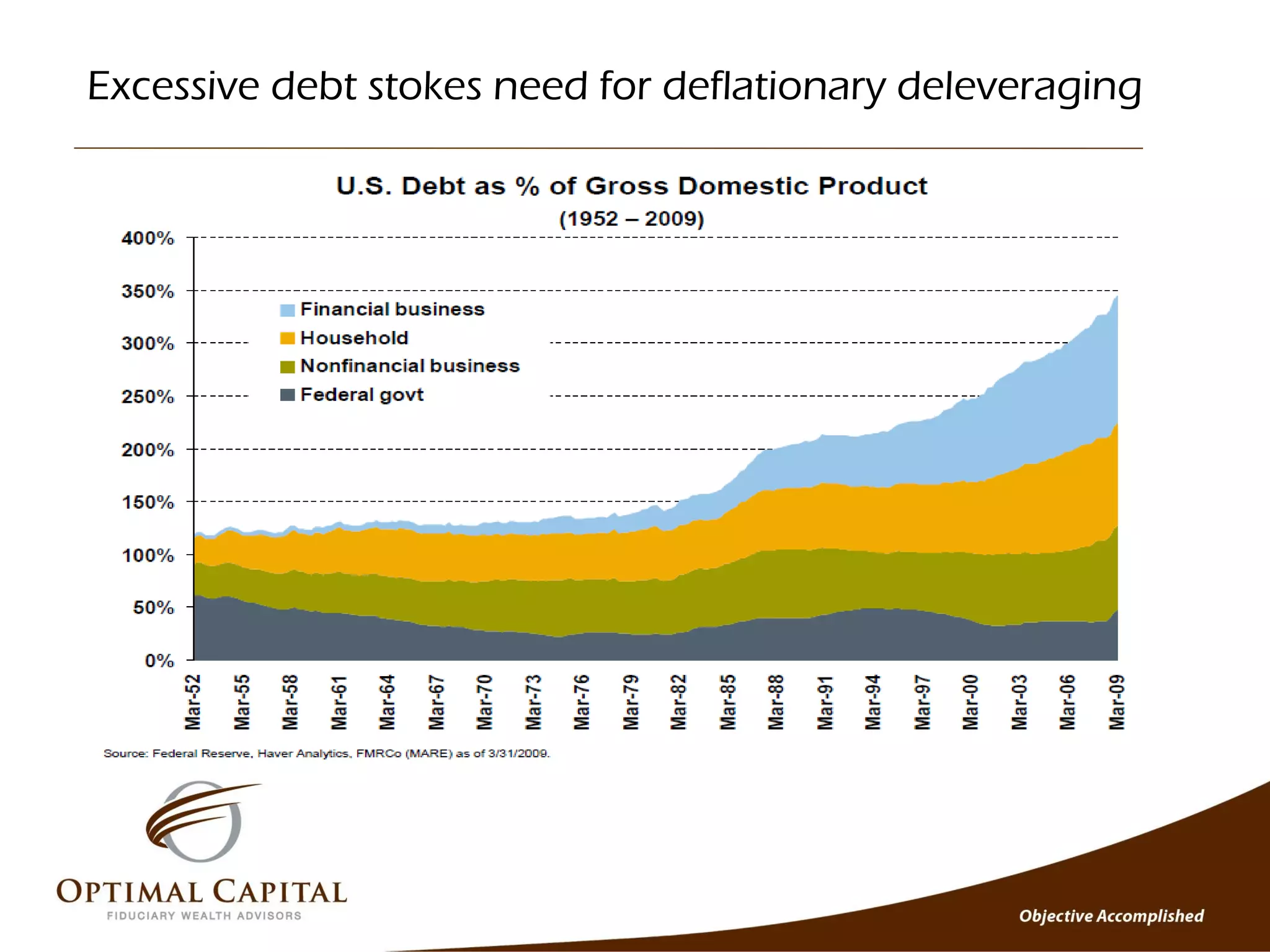

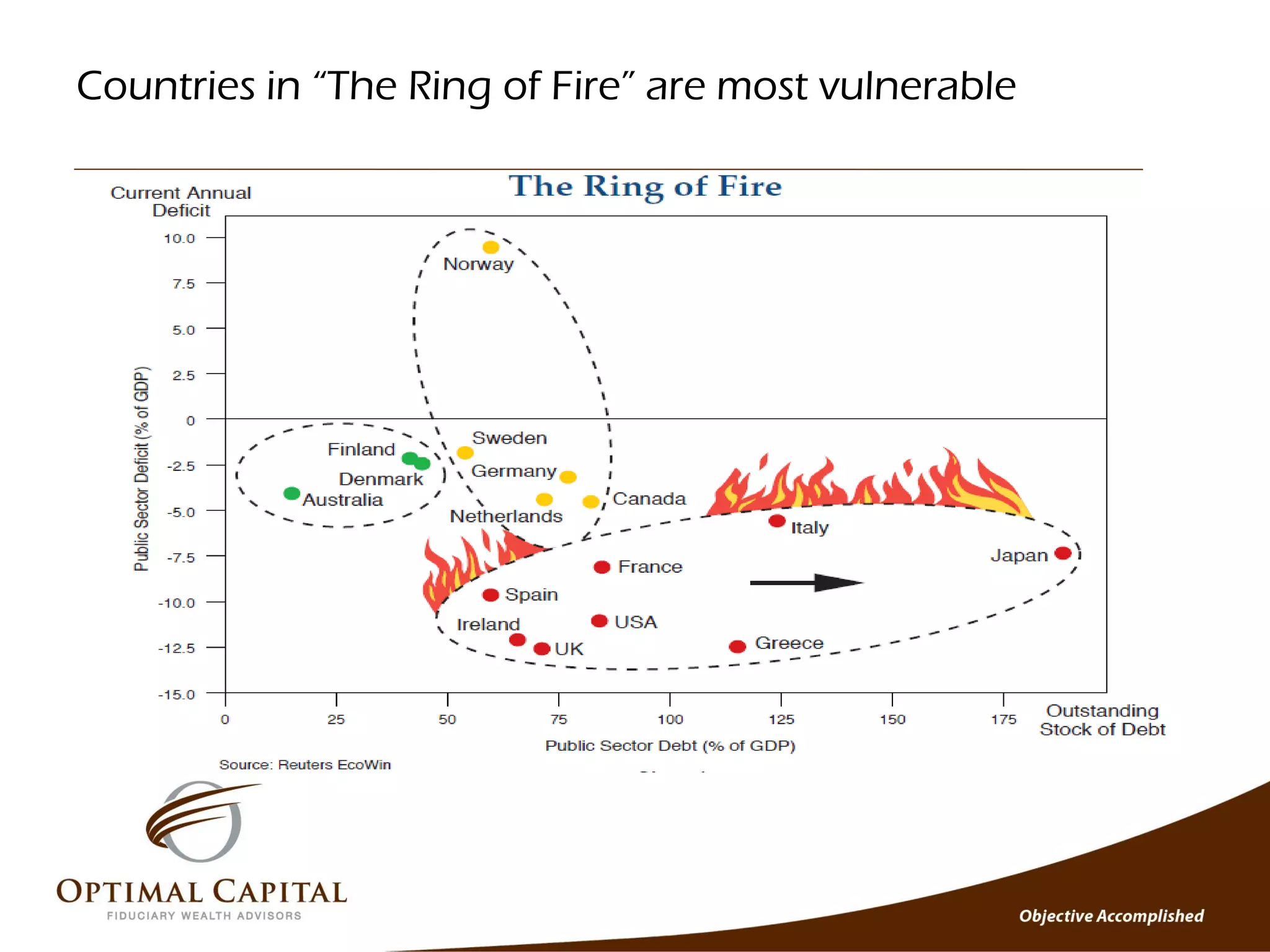

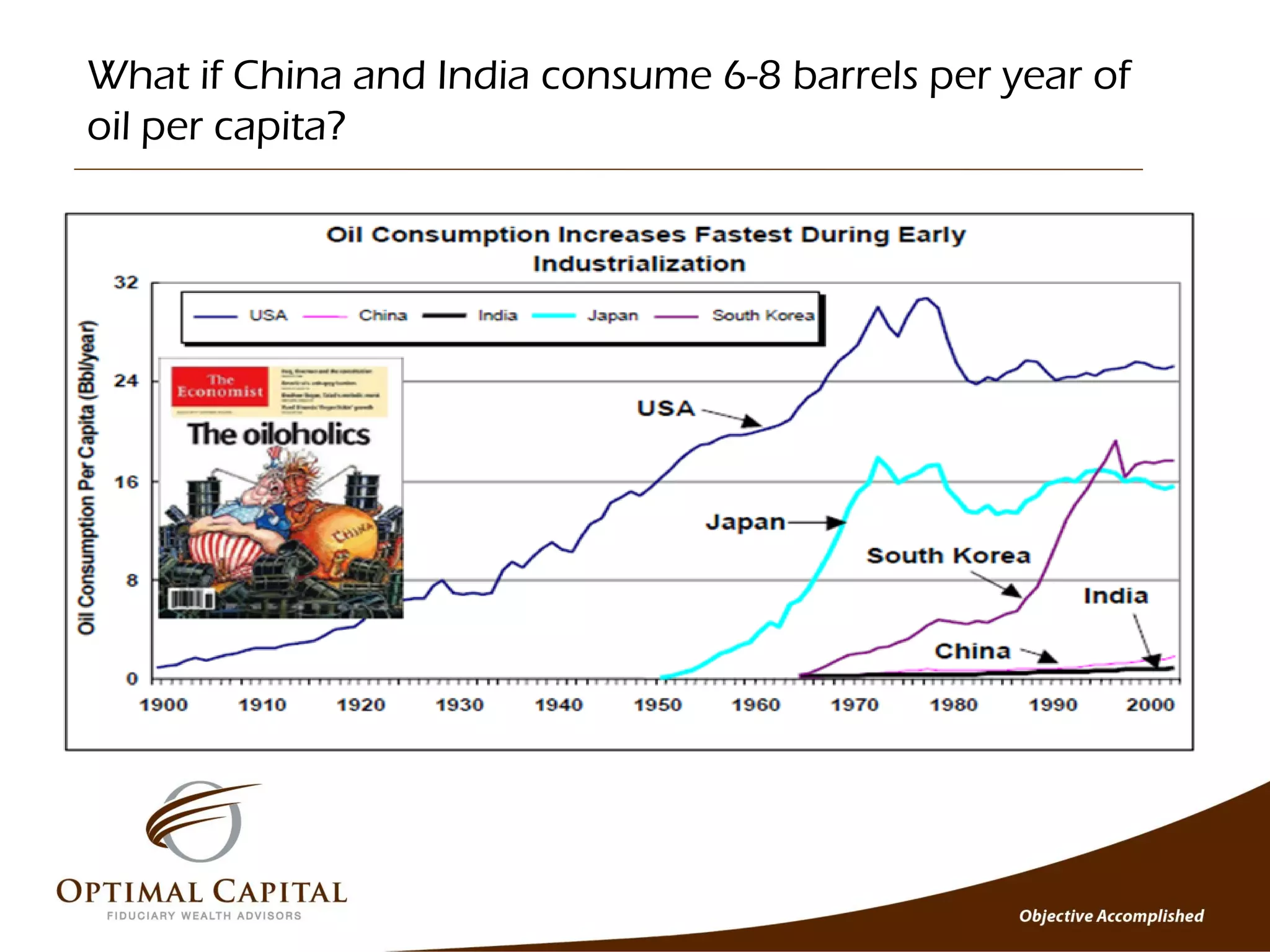

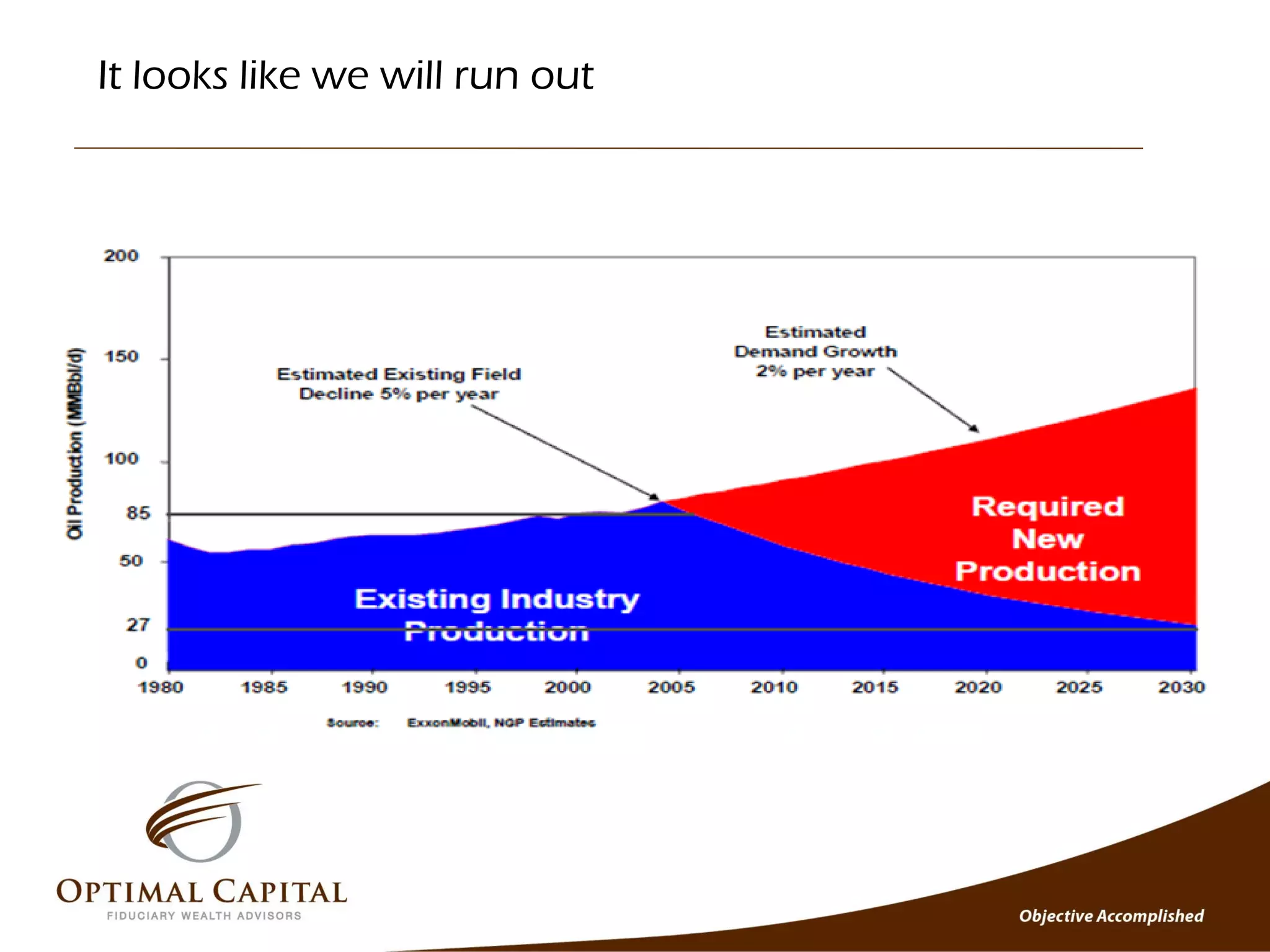

- The document provides an investment outlook and commentary for the 1st quarter of 2010. It discusses various factors impacting the capital markets, including the state of the economy, the equity and bond markets, and risks related to the US dollar and developing economies.

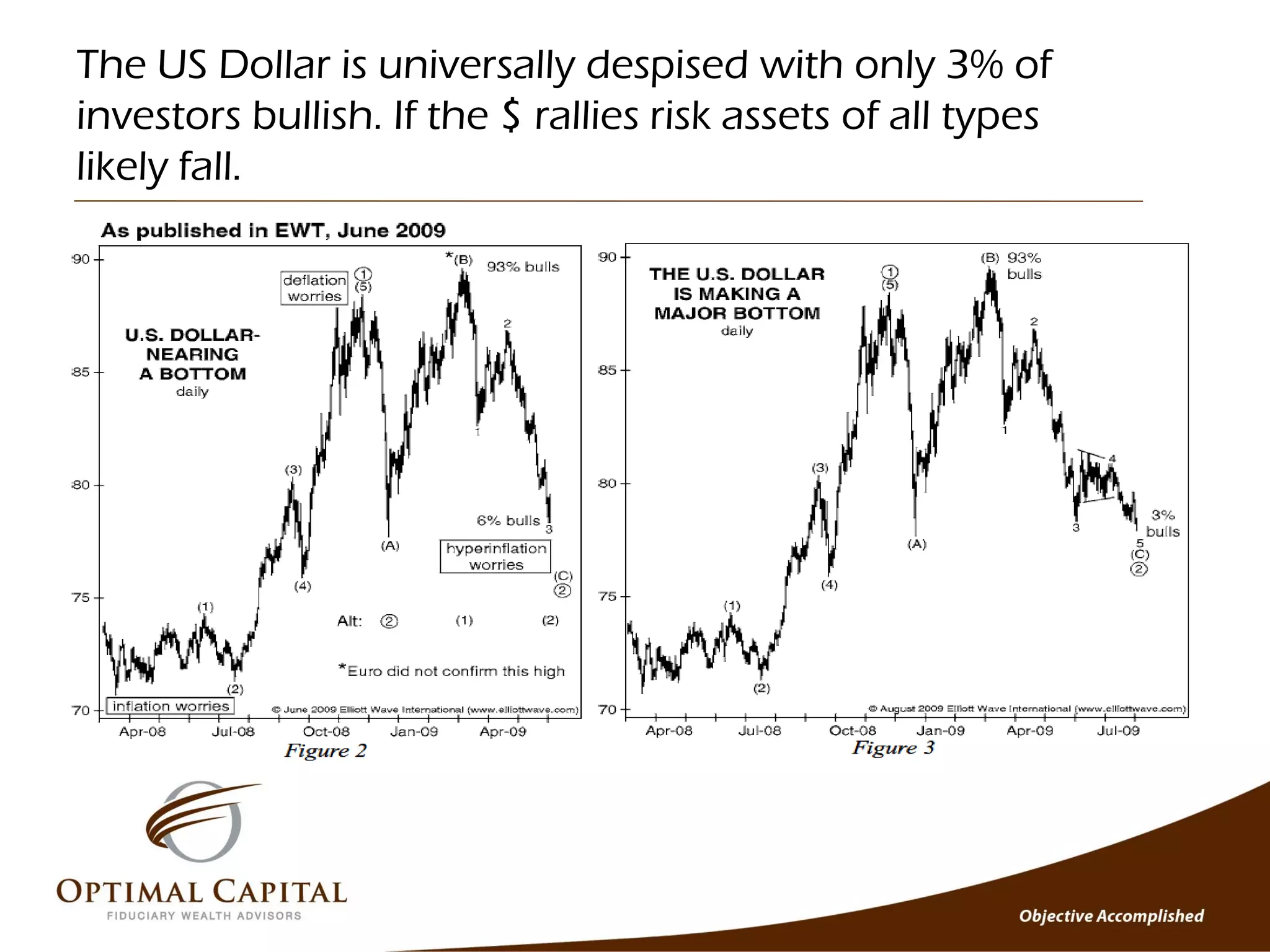

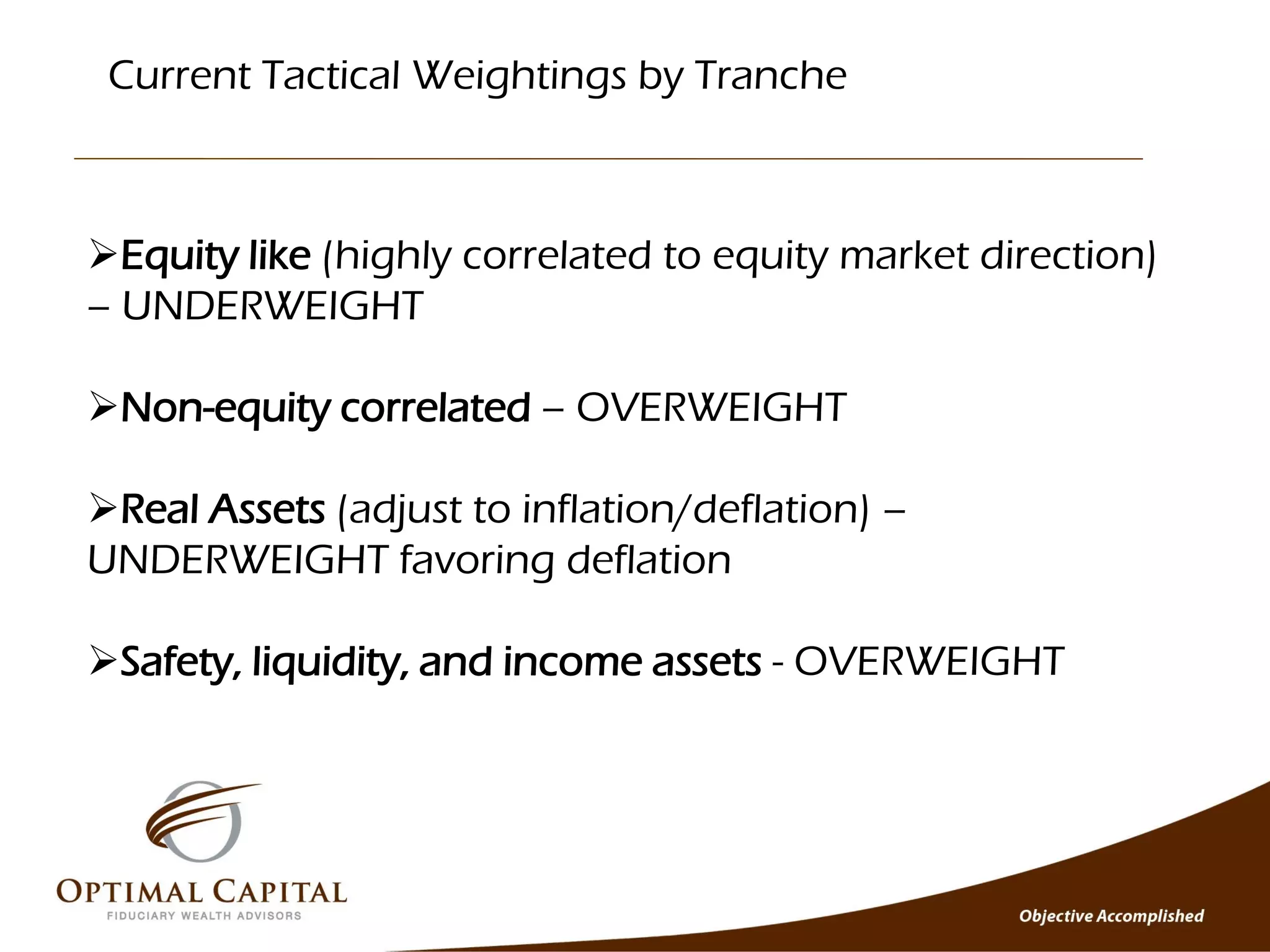

- The author recommends being underweight in equity-like investments, overweight in non-equity correlated investments, underweight real assets favoring deflation, and overweight safety, liquidity, and income assets. Key risks discussed include high government debt levels, potential issues in developing economies, and uncertainty around the US dollar.

![Strategic & Tactical[1]](https://cdn.slidesharecdn.com/ss_thumbnails/309c6a96-abbe-4571-84a4-cc5aa58b8a8d-150211041549-conversion-gate02-thumbnail.jpg?width=640&height=640&fit=bounds)