Downloaded 17 times

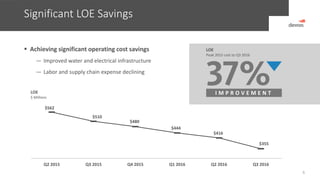

This document provides an investor presentation for Devon Energy from November 2016. It summarizes Devon's asset portfolio, including premier positions in the STACK, Delaware Basin, and other US resource plays. It highlights Devon's operating strategy to maximize productivity and reduce costs, delivering best-in-class well results. The presentation outlines Devon's plans to accelerate activity in the STACK and Delaware Basin while preserving continuity in other plays. It also emphasizes Devon's strong financial position and hedging program.