Download to read offline

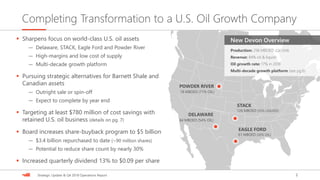

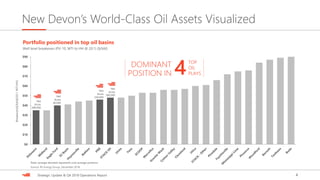

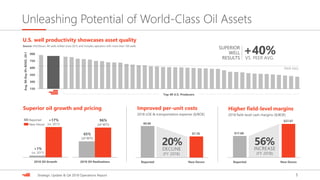

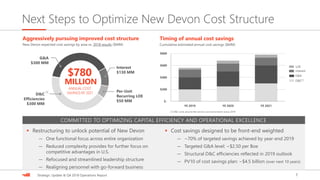

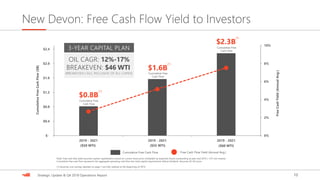

- Devon Energy is completing its transformation into a U.S. oil growth company by focusing on its core U.S. oil assets and pursuing strategic alternatives for its Canadian and Barnett Shale assets. - It is targeting $780 million in annual cost savings by 2021 from operational efficiencies and restructuring, and has an increased $5 billion share repurchase program. - The company expects to deliver 12-17% annual oil production growth through 2021 and generate over $1.6 billion in cumulative free cash flow at $55 WTI oil prices, while maintaining its strong financial position.