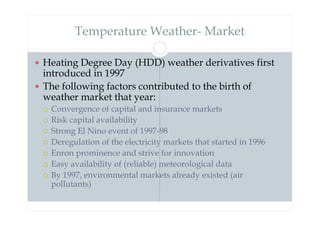

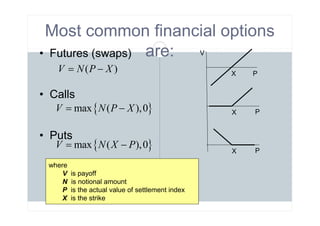

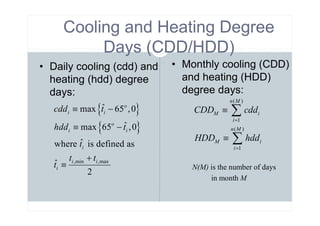

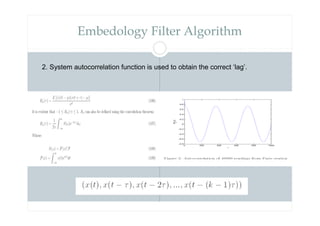

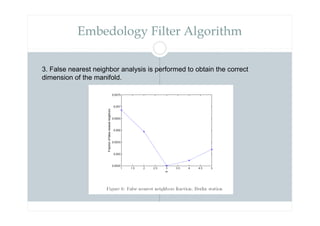

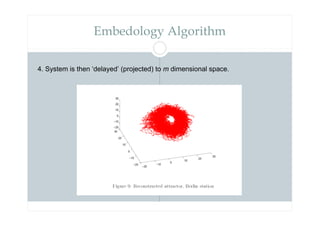

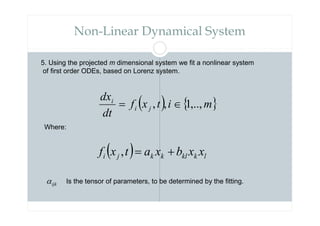

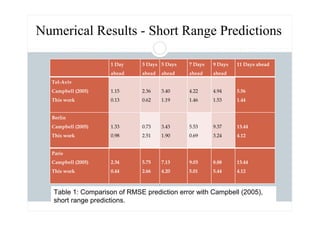

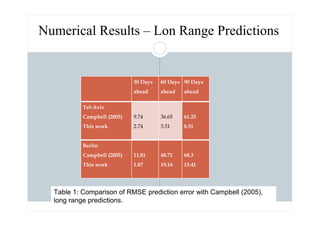

The document discusses nonlinear weather forecasting techniques used for pricing weather derivatives, particularly focusing on temperature modeling and the impact of various market factors that led to the establishment of weather markets in 1997. It includes methodologies like GARCH models and embedology algorithms to predict temperature trends and seasonal volatility. Additionally, it compares prediction accuracy against previous studies, highlighting methodologies and numerical results for short and long-term weather forecasts.

![Temperature Modeling and Forecasting:

Alaton et al. (2002)

Alaton et al. (2002) obtain the following stochastic

differential equation in continuous form:

The above equation can be rewritten in discrete form:

can be estimated based on Equations (2) and (3).

can be obtained using the OLS regression and

)

5

(

)]

(

)

/

[( t

t

t

a

t

a

t

t dW

dt

T

T

dt

dT

dT σ

α +

−

+

=

a

j

T

( ) )

8

(

)

ˆ

1

(

ˆ

~

2

1

ˆ

1

2

1

1

2

∑

=

−

− −

−

−

−

=

µ

α

α

σ

µ

µ

N

j

j

a

j

j T

T

T

N

)

month

in

days

(

,

,

1

),

1

,

0

(

~

(7)

)

1

(

)

(

~

1

1

1

1

µ

η

η

σ

α

α

µ

µ

µ

N

N

j

N

T

T

T

T

T

T

j

j

j

a

j

a

j

a

j

j

j

K

=

+

−

+

=

−

−

≡ −

−

−

−

α̂

Time Trend

Mean-Reverting](https://image.slidesharecdn.com/nonlinearweatherforecasting-orsis-220427093214/85/Nonlinear-Weather-Forecasting-ORSIS-pdf-10-320.jpg)

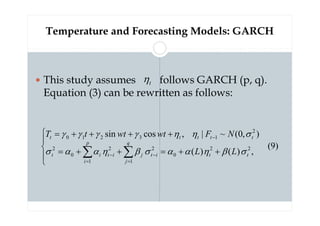

![HDD/CDD Option Price Formula . Alaton et al. 2002)

)

15

(

2

)

(

)

(

)

(

)

(

]

|

}

0

,

[max{

(14)

2

)

(

)

(

)

(

)

(

]

|

}

0

,

[max{

2

2

2

2

1

2

)

(

0

)

(

)

(

2

)

(

)

(

)

(

−

+

−

Φ

−

Φ

−

=

−

=

−

=

+

−

Φ

−

=

−

=

−

=

−

−

−

−

−

−

−

−

−

−

−

−

∞

−

−

−

−

∫

∫

n

n

n

n

n

n

n

n

n

n

n

n

e

e

K

e

dx

x

f

x

K

e

F

H

K

E

e

p

e

K

e

dx

x

f

K

x

e

F

K

H

E

e

c

n

n

n

n

n

t

t

r

K

H

t

t

r

t

n

Q

t

t

r

t

n

n

n

t

t

r

K

H

t

t

r

t

n

Q

t

t

r

t

σ

µ

α

α

π

σ

σ

µ

α

µ

π

σ

α

µ](https://image.slidesharecdn.com/nonlinearweatherforecasting-orsis-220427093214/85/Nonlinear-Weather-Forecasting-ORSIS-pdf-28-320.jpg)

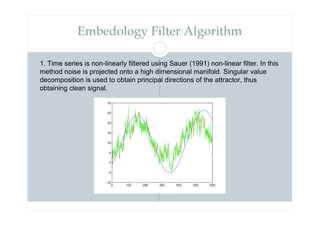

![Alaton et al. (2002) estimate the conditional variance

.

0

)

20

(

]

)[

1

)(

2

/

1

(

]

|

,

[

)

19

(

]

)[

1

)(

2

/

1

(

]

|

[

)

18

(

]

)[

1

)(

/

(

)

(

]

|

[

2

2

2

2

1

2

)

(

2

2

2

2

1

2

2

1

)

(

u

t

s

e

e

F

T

T

Cov

e

F

T

Var

e

T

e

T

T

F

T

E

t

s

s

s

t

s

u

t

t

s

s

s

t

t

s

s

m

t

s

t

m

s

s

s

t

Q

≤

≤

≤

+

+

+

−

=

+

+

+

−

=

+

+

+

−

−

+

−

=

+

+

−

−

−

+

+

−

+

+

−

−

−

σ

σ

σ

α

σ

σ

σ

α

σ

σ

σ

α

λ

α

α

α

α

α

L

L

L](https://image.slidesharecdn.com/nonlinearweatherforecasting-orsis-220427093214/85/Nonlinear-Weather-Forecasting-ORSIS-pdf-29-320.jpg)

![First-Order and Second-Order Moments of Hn and Cn

( )

( )

)

27

(

]

│

,

[

2

]

|

[

]

│

[

)

26

(

23

]

|

[

|

23

]

|

[

)

25

(

]

|

,

[

2

]

|

[

]

|

[

)

24

(

]

|

[

23

|

23

]

|

[

1

1

1

1

1

1

∑∑

∑

∑

∑

∑∑

∑

∑

∑

=

=

=

=

=

=

+

≈

−

=

−

≈

+

≈

−

=

−

≈

j

i

t

t

t

n

t t

t

t

n

n

i t

t

Q

t

n

i t

Q

t

n

Q

j

i

t

t

t

n

t t

t

t

n

n

i t

t

Q

t

n

i t

Q

t

n

Q

F

T

T

Cov

F

T

Var

F

C

Var

n

F

T

E

F

n

T

E

F

C

E

F

T

T

Cov

F

T

Var

F

H

Var

F

T

E

n

F

T

n

E

F

H

E

j

i

i

i

j

i

i

i](https://image.slidesharecdn.com/nonlinearweatherforecasting-orsis-220427093214/85/Nonlinear-Weather-Forecasting-ORSIS-pdf-30-320.jpg)