Download to read offline

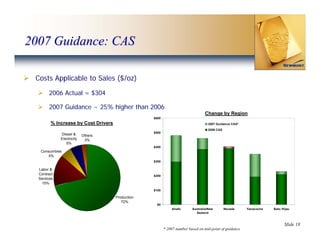

This presentation discusses Newmont Mining Corporation capitalizing on the gold bull market. Newmont is the only major US gold company and has gold assets in Nevada, Peru, Indonesia, Australia, and Ghana. In 2006, Newmont had equity gold sales of 5.9 million ounces. Newmont provides leverage to rising gold prices with no gold hedges. Guidance is given for 2007 production and costs at each region. Costs applicable to sales are expected to increase approximately 25% in 2007 due to increases in factors such as labor, fuel and consumables.