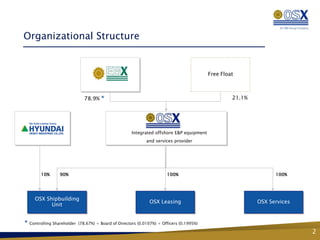

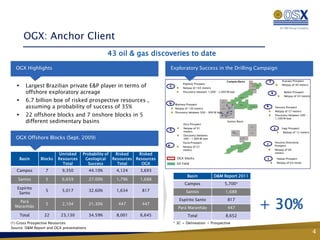

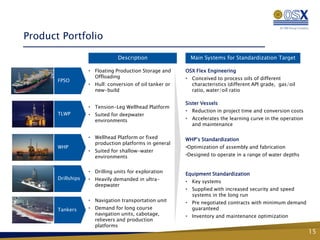

OSX is an integrated offshore oil and gas equipment and services provider with a focus on Brazil. It has a large order book from OGX of 48 offshore units worth $30 billion. OSX is building a state-of-the-art shipyard in Açu, Brazil in partnership with Hyundai Heavy Industries, the largest shipbuilder in the world, to help meet local content requirements and demand from Petrobras and OGX for pre-salt development. The shipyard will leverage Hyundai's expertise and technology to efficiently produce FPSOs, WHPs, and other offshore units for the growing Brazilian offshore oil and gas market.

![Osx corporate presentation english_february [modo de compatibilidade]](https://cdn.slidesharecdn.com/ss_thumbnails/osxcorporatepresentationenglishfebruarymododecompatibilidade-130215140050-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Osx apresentação corporativa português_fevereiro [modo de compatibilidade]](https://cdn.slidesharecdn.com/ss_thumbnails/osxapresentaocorporativaportugusfevereiromododecompatibilidade-130215135903-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)