Downloaded 102 times

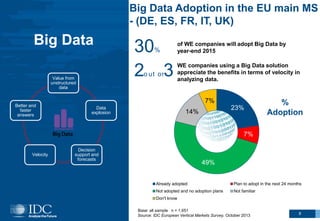

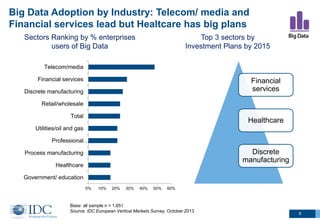

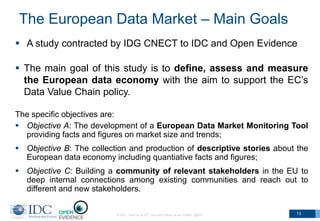

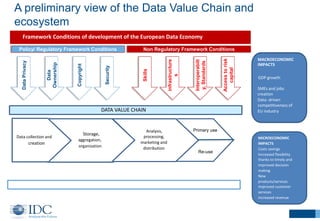

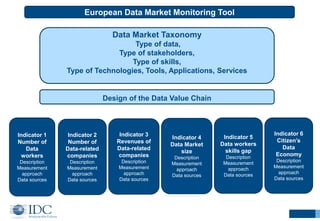

The 2014 NESSI summit discussed the rapid growth of the European big data market, highlighting key trends, challenges in measuring the market, and the need for a collaborative community effort. The adoption of big data technologies is accelerating, particularly in the UK, Germany, and France, with sectors like financial services and healthcare leading investment plans. Additionally, the summit emphasized the importance of addressing data privacy issues and developing a European data market monitoring tool to support economic policies.

![제 23회 보아즈(BOAZ) 빅데이터 컨퍼런스 - [MBOAX] : ABSA를 활용한 소비자 반응 분석 기반 운영 효율화 대시보드 설계](https://cdn.slidesharecdn.com/ss_thumbnails/3-1boaz23rdconferencemboax-260203102709-9d519923-thumbnail.jpg?width=640&height=640&fit=bounds)

![7.__Developing_a_Research_Proposal[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/7-260131073037-df92dd7d-thumbnail.jpg?width=640&height=640&fit=bounds)

![Hacking-Uncovered-How-People-Get-Hacked-and-How-to-Stay-Safe[1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/hacking-uncovered-how-people-get-hacked-and-how-to-stay-safe1-260130170011-4883a9c7-thumbnail.jpg?width=640&height=640&fit=bounds)