The document discusses economic trends in the United States. It notes that the US economy is divided into eight regions, and the finance, insurance and real estate industry and manufacturing industry make up 37% of GDP. Certain regions and states have experienced stronger growth than others in recent years, led by industries like mining, utilities and information. The largest states by GDP are California, Texas, New York, Florida and Illinois.

Did you know total nonfarm payroll employment fell by 701,000 in March 2020, measuring the effects of COVID-19 and efforts to contain it? Employment in leisure and hospitality fell by 459,000, mainly in food services and drinking places. Notable declines also occurred in health care and social assistance, professional and business services, retail trade, and construction.

Fred Dickson, Chief Investment Strategist for DA Davidson spoke at the Southern Oregon Business Conference on January 26, 2011. While our region has some specific challenges, it is good to hear that we are avoiding a double-dip recession and we can expect to continue a slow recovery.

The Federal Government has spent almost $32 billion on cybersecurity-related expenditures in the past 10 years. More importantly, the cyber spending boom shows no sign of slowing, as spending increased 281 percent from 2006 to 2014 (an average of 22 percent annually). This historic growth in cyber spending runs counter to the greater trend in Federal Government spending that has led to a relatively modest increase of 4.2 percent annually over the same time period.

As the world becomes increasingly digitized, so has the Federal Government, but individual agencies are not spending on cybersecurity in similar ways. Each agency's funding over the past 10 years tells a unique story.

Tightening labour markets: threat or opportunity for HR service providers? The presentation start with an economic outlook and the conséquences for the labour market in Belgium. With some concluding remarks voor HR service providers.

Mercer Capital's Value Focus: Construction and Building Materials | Q1 2020 |...Mercer Capital

Mercer Capital's Construction Industry newsletter provides a broad range of specialized valuation and transaction advisory services to the construction industry, including residential, commercial, civil, paving, concrete, and more. Each issue includes a segment focus, market overview, mergers and acquisitions review, and more.

http://pwc.to/1lN91cC

Comme tous les mois, l’équipe d’économistes de PwC publie une note sur la situation macro-économique mondiale. Ce mois-ci, focus sur l’accroissement des inégalités dans les pays matures ; les incertitudes concernant la croissance chinoise ; et les prévisions de croissance pour la Grande-Bretagne.

Did you know total nonfarm payroll employment fell by 701,000 in March 2020, measuring the effects of COVID-19 and efforts to contain it? Employment in leisure and hospitality fell by 459,000, mainly in food services and drinking places. Notable declines also occurred in health care and social assistance, professional and business services, retail trade, and construction.

Fred Dickson, Chief Investment Strategist for DA Davidson spoke at the Southern Oregon Business Conference on January 26, 2011. While our region has some specific challenges, it is good to hear that we are avoiding a double-dip recession and we can expect to continue a slow recovery.

The Federal Government has spent almost $32 billion on cybersecurity-related expenditures in the past 10 years. More importantly, the cyber spending boom shows no sign of slowing, as spending increased 281 percent from 2006 to 2014 (an average of 22 percent annually). This historic growth in cyber spending runs counter to the greater trend in Federal Government spending that has led to a relatively modest increase of 4.2 percent annually over the same time period.

As the world becomes increasingly digitized, so has the Federal Government, but individual agencies are not spending on cybersecurity in similar ways. Each agency's funding over the past 10 years tells a unique story.

Tightening labour markets: threat or opportunity for HR service providers? The presentation start with an economic outlook and the conséquences for the labour market in Belgium. With some concluding remarks voor HR service providers.

Mercer Capital's Value Focus: Construction and Building Materials | Q1 2020 |...Mercer Capital

Mercer Capital's Construction Industry newsletter provides a broad range of specialized valuation and transaction advisory services to the construction industry, including residential, commercial, civil, paving, concrete, and more. Each issue includes a segment focus, market overview, mergers and acquisitions review, and more.

http://pwc.to/1lN91cC

Comme tous les mois, l’équipe d’économistes de PwC publie une note sur la situation macro-économique mondiale. Ce mois-ci, focus sur l’accroissement des inégalités dans les pays matures ; les incertitudes concernant la croissance chinoise ; et les prévisions de croissance pour la Grande-Bretagne.

This report offers a comprehensive overview of the situation in the United States focusing on the business perspective. The United States remains one of the world’s key economic players. With a real GDP per capita of US$62,479.3, this high-income country occupied 6th place in a 2019 global comparison. The U.S. was home to about 329.1 million people in 2019 and is renowned for its extensive entertainment industry.

What's included?

Economic conditions (incl. COVID-19 economic impact), public finances, and detailed information on the labor force

Demographics, consumption, and income

Imports, exports, foreign direct investments

Fitch Solutions operational risk indexes

Business culture and local habits

Government structure, overview of stability and threats, and the political environment

Territorial CO2 emissions, energy shares, and PM2.5 exposure

In the US …

> US federal R&E credit lapses again – will it be renewed?

> Presidential candidates acknowledge need for a better federal-level program

> California, Wisconsin and Indiana increase their state-level tax credits

In Canada …

> Ottawa hints at “SR&ED Overhaul” in 2008 budget

Breaking Out of a Circle of Scarcity: The Oregon Business Plan's Challenge f...The Oregon Business Plan

Sliding per capita income is leading to low investments in public services. Medicaid and Prison spending are squeezing out investments in education, further driving down personal incomes. Over the next decade the aging baby-boomers and an increasingly diverse population will put more pressure on government revenues. Oregon is trapped in a "circle of scarcity." Breaking out of it is the most important task for Oregon's business, elected and community leaders today.

Why the Income Tax Cuts Hurt More Than They HelpWomen for Kansas

Presentation by Bernie Koch, director of the Kansas Economic Progress Council, given at the Taking Back Kansas convention on August 30, 2014, in Wichita, Kansas.

U.S. employment update and outlook: November 2014JLL

October records another month of 200,000+ job gains

The U.S. economy saw the addition of 214,000 net new jobs in October. With revisions of earlier months’ data, this makes October the eighth consecutive month with gains surpassing 200,000 jobs.

This steady expansion has helped to push down unemployment, which fell by 10 basis points to 5.8 percent. Total unemployment—which includes detached workers—dropped by 30 basis points to a recovery low of 11.5 percent, also below the long-term average.

See more economic, office and real estate research at http://bit.ly/1wCNyXQ

Latin America’s emerging sectors:A closer look at fintech and renewable energyDubaiChamber

Latin America’s emerging sectors: A closer look at fintech and renewable energy is an Economist Intelligence Unit report, sponsored by Dubai Chamber of Commerce and Industry. This report explores high potential emerging economic sectors in Latin America, focusing on financial technology (fintech) and renewable energy. We review the factors driving growth in these

sectors and key impediments to further growth. This report is based on extensive desk research and in-depth interviews with entrepreneurs and regional experts in Latin America and the Caribbean (LAC). The interviews were conducted in December 2017 and January 2018.

This report offers a comprehensive overview of the situation in the United States focusing on the business perspective. The United States remains one of the world’s key economic players. With a real GDP per capita of US$62,479.3, this high-income country occupied 6th place in a 2019 global comparison. The U.S. was home to about 329.1 million people in 2019 and is renowned for its extensive entertainment industry.

What's included?

Economic conditions (incl. COVID-19 economic impact), public finances, and detailed information on the labor force

Demographics, consumption, and income

Imports, exports, foreign direct investments

Fitch Solutions operational risk indexes

Business culture and local habits

Government structure, overview of stability and threats, and the political environment

Territorial CO2 emissions, energy shares, and PM2.5 exposure

In the US …

> US federal R&E credit lapses again – will it be renewed?

> Presidential candidates acknowledge need for a better federal-level program

> California, Wisconsin and Indiana increase their state-level tax credits

In Canada …

> Ottawa hints at “SR&ED Overhaul” in 2008 budget

Breaking Out of a Circle of Scarcity: The Oregon Business Plan's Challenge f...The Oregon Business Plan

Sliding per capita income is leading to low investments in public services. Medicaid and Prison spending are squeezing out investments in education, further driving down personal incomes. Over the next decade the aging baby-boomers and an increasingly diverse population will put more pressure on government revenues. Oregon is trapped in a "circle of scarcity." Breaking out of it is the most important task for Oregon's business, elected and community leaders today.

Why the Income Tax Cuts Hurt More Than They HelpWomen for Kansas

Presentation by Bernie Koch, director of the Kansas Economic Progress Council, given at the Taking Back Kansas convention on August 30, 2014, in Wichita, Kansas.

U.S. employment update and outlook: November 2014JLL

October records another month of 200,000+ job gains

The U.S. economy saw the addition of 214,000 net new jobs in October. With revisions of earlier months’ data, this makes October the eighth consecutive month with gains surpassing 200,000 jobs.

This steady expansion has helped to push down unemployment, which fell by 10 basis points to 5.8 percent. Total unemployment—which includes detached workers—dropped by 30 basis points to a recovery low of 11.5 percent, also below the long-term average.

See more economic, office and real estate research at http://bit.ly/1wCNyXQ

Latin America’s emerging sectors:A closer look at fintech and renewable energyDubaiChamber

Latin America’s emerging sectors: A closer look at fintech and renewable energy is an Economist Intelligence Unit report, sponsored by Dubai Chamber of Commerce and Industry. This report explores high potential emerging economic sectors in Latin America, focusing on financial technology (fintech) and renewable energy. We review the factors driving growth in these

sectors and key impediments to further growth. This report is based on extensive desk research and in-depth interviews with entrepreneurs and regional experts in Latin America and the Caribbean (LAC). The interviews were conducted in December 2017 and January 2018.

IAR Public Policy Meetings, January 26, 2011.

Presented by Geoffrey J.D. Hewings, Director, Regional Economics Applications Laboratory - University of Illinois Institute of Government and Public Affairs

GroupM has released its Global Mid-Year Media Forecast that details how COVID-19 sharply transformed the global advertising economy from a 6.2% growth rate in 2019 to a double-digit decline this year.

This report report from Brookings, with Rockefeller Foundation support, shows that building up a region’s advanced industries is one such possibility with enormous potential. These industries not only create good jobs within the industry, but also up and down their massive supply chains. These jobs provide higher wages and greater opportunity to low and middle-income workers adversely affected by the economic recession.

Running head COMPARISON OF SOUTH KOREA AND USA .docxtodd271

Running head: COMPARISON OF SOUTH KOREA AND USA 1

COMPARISON OF SOUTH KOREA AND USA 6

COMPARISON OF SOUTH KOREA AND USA

Applied Managerial Economic

April 15, 2020

To asses and look at the Gross domestic product and different elements of the nation, it is significant for rulers to contemplate the administrative, financial aspects. Administrative, financial matters are the training of how phenomenal assets are assimilated most expertly to achieve administrative zones. It is an esteemed gear for inspecting business conditions to take better ends. We can concentrate as a matter of first importance the interest and its different components influencing the interest; it would be the primary substances of any nation or individual development. To assess the Gross domestic product of any nation, it is significant for the researcher to look at the interest capacities and their employment rate.

In 2018, the normal inflation rate in South Korea added up to about 1.48 percent contrasted with the earlier year, while in the USA added up to about 2.4 percent.

High paces of inflations are unfortunate, much the same as low rates, and South Korea is right now battling with the last mentioned. South Korea is really a prosperous nation and at present positions eleventh on the rundown of the 20 nations with the biggest Gross domestic product; however, its inflation rate is liable to worry, as it is right now at levels beneath 2 percent (Plecher, 2019).

Notwithstanding, there is still an expectation that inflation will come back to steady rates somewhere in the range of 3 and 4.5 percent. At present, South Korea is endeavoring to adjust its dependence on exports by growing the services industry, particularly as the export marketplace declines.

Gross domestic product is the aggregate of business offering manufactured in a nation annually; it is a solid pointer of financial quality. In 2018, South Korea's Gross domestic product was about 1.72 trillion U.S. dollars. While the USA's Gross domestic product was about 20.58 trillion dollars

In the USA, the economy is relied upon to develop at a gentler pace this year. Obscuring monetary upgrade and frail business venture will diminish development, while further drawback dangers radiate from a submissive worldwide crisis, the coronavirus epidemic and the impacts of waiting for exchange pressures. Economists see Gross domestic product extending 1.7% in 2020, declining 0.1 rate points from previous month prediction and in 2021, its 1.8 percent (U.S. Economic Outlook, 2020).

In South Korea, this year, monetary development is relied upon to speed up marginally because of improvement in fixed speculation and as the innovation and development parts fortify. Eventually, more vulnerable than-anticipated development in China, the coronavirus pandemic in the locale and political strains with Japan present significant draw.

This presentation provides analysis of GDP (Gross Domestic Product) for Canada. The presentation will highlight areas like consumer spending, exports, government spending and other areas.

The DC Development Report is a summary of the major development and construction projects in the District of Columbia. The Washington, DC Economic Partnership (WDCEP) began tracking development activity in 2001 with the hope of creating a comprehensive database that would answer a number of questions in regards to the construction activity in the city. The Report summarizes our entire database of projects, highlights major projects and what lies ahead for development in the District of Columbia.

This update of the DC Development Report is an overview of development activity and of the expansion occurring in DC. As a resource book, it is a compilation of nearly 14 years of data collection and research that provides an overview of an ever-changing development and construction cycle.

The WDCEP performs an annual “development census” in the month of September and receives contributions from more than 100 developers, architects, contractors and economic development organizations. This outreach results in updates to more than 350 projects. While our database of projects is constantly being updated, for the purposes of this publication all data reflects project status, design and information as of September 2014.

In 2014 the WDCEP partnered with CBRE to provide an economic overview of DC and in-depth analysis of the office, retail and residential markets. Although every attempt was made to ensure the quality of the information contained in this document, the WDCEP and CBRE makes no warranty or guarantee as to its accuracy, completeness or usefulness for any given purpose.

1.

1

Muni

Economic

Outlook

Overview

The

United

States

(U.S.)

landscape

is

separated

into

eight

different

regions:

New

England,

Mideast,

Great

Plains,

Southeast,

Plains,

Southwest,

Rocky

Mountain

and

Far

West.

Although

each

industry

has

an

industry

advantage,

the

finance,

insurance

and

real

estate

industry

and

the

manufacturing

industry

make

up

37%

of

U.S.

GDP.

There

has

been

strong

growth

in

the

mining

and

utility

industry

in

recent

years,

but

that

growth

has

slowed

down

from

its

highs

in

2012.

Most

of

the

jobs

however

are

in

the

healthcare

and

government

industries.

This

outlook

report

aims

to

take

a

look

at

GDP

growth

and

trends

for

regions,

states

and

industries,

population

growth

and

trends

for

states

and

metropolitan

areas,

tax,

income

and

debt

metrics

for

states

as

well

as

economic

performance

analysis

from

highly

regarded

think-‐tanks.

Quick

Takes

-‐ Mining

and

financial

activity

industries

have

grown

tremendously

since

2002

-‐ Health

care,

construction

and

financial

activity

industries

are

expected

to

be

growth

industries

until

2022

-‐ States

like

Texas,

South

Carolina,

North

Carolina,

Florida,

Georgia

and

North

Dakota

are

projected

to

be

the

leading

growth

states

in

2.

2

Past

&

Future

Trends

in

the

U.S.

Economy

GDP

Trends

Region

The

eight

regions

of

the

U.

S.

are

most

notably

known

for

their

exposure

to

the

finance,

insurance

and

real

estate

(financial

activity)

indsutry.

The

regions

driving

the

financial

activity

exposure

are

both

the

Mideast

and

the

Southeast

making

up

about

44%

of

the

industry.

The

Southeast

and

the

Far

West

are

the

two

largest

regions

from

a

GDP

standpoint

(see

chart

above).

The

Southeast

region

has

large

exposure

to

both

the

financial

activity

industrry

(22%)

and

manufacturing

industry

(15%).

The

Far

West

region

has

large

exposure

to

both

the

financial

activity

industry

(23%)

and

professional

and

business

service

industry

(14%),

which

consists

of

technical

services,

management

of

companies,

and

waste

services.

The

Soutwest

region

had

the

largest

growth

from

2011

to

2014.

This

growth

was

led

by

the

mining

industry

with

32%

growth.

Most

of

the

southwest

mining

exposure

comes

from

Texas,

who

has

greatly

benefitted

from

the

oil

boom

that

we

have

most

recently

seen.

State

California

is

the

largest

state

in

the

U.S.

from

a

GDP

standpoint

and

has

had

extraordinary

growth

in

the

information

industry

since

2011.

This

industry

consists

of

publishing,

software,

motion

picture

and

many

other

sectors.

Its

largest

industry

is

the

financial

activity

industry

representing

21%

of

their

GDP.

Texas

has

been

the

outlier

compared

to

other

large

states

with

growth

of

22%.

This

growth

has

been

fueled

by

both

the

utility

industry

(52%)

consisting

of

electric

power,

natural

gas,

water

supply

and

waste

management

and

the

mining

industry

(37%).

Area

Percent

Growth

(2011-2014)

2014 GDP

(Millions)

% of U.S.

Economy

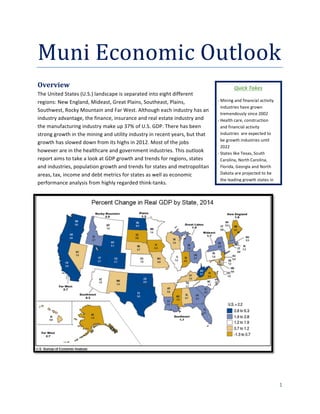

Southwest 16.90 1,975,615 13%

Rocky Mountain 8.60 542,102 3%

Far West 8.20 2,947,421 19%

United States 7.60 15,773,516 100%

Plains 7.20 1,021,091 6%

Great Lakes 6.40 2,187,656 14%

Mideast 5.60 2,876,279 18%

Southeast 5.00 3,365,475 21%

New England 4.70 852,517 5%

Percent

Growth

(2011-2014)

United States 12.3 15,773,516$ 100.0%

California 13.7 2,113,280$ 13.4%

Texas 22 1,467,342$ 9.3%

New York 13.8 1,279,921$ 8.1%

Florida 14 769,662$ 4.9%

Illinois 9.6 680,448$ 4.3%

Area

2014 GDP

(Millions)

% of U.S.

Economy

3.

3

From

a

growth

perspective,

different

states

take

the

stage.

North

Dakota

led

the

way

with

36%

growth

led

by

the

mining

industry

(107%)

and

the

construction

industry

(61%).

Although

North

Dakota

should

not

be

discounted,

it

only

represents

0.3%

of

U.S.

GDP.

Colorado,

behind

Texas

is

the

second

largest

state

with

notable

growth.

Colorado

has

seen

growth

in

its

construction

industry

(33%)

and

utility

industry

(20%).

The

financial

activity

industry

represents

19%

of

their

GDP

and

grew

at

a

rate

of

17%

from

2011

to

2014.

Industry

Trends

The

private

industry

accounts

for

88%

of

the

U.S.

GDP.

A

substaintial

amount

of

the

U.S.

GDP

comes

from

the

financial

activity

industry,

professional

and

business

services

industry,

and

the

manufacturing

industry.

The

financial

activity

industry

represnts

about

23%

of

GDP

and

grew

about

15%

from

2011

to

2014.

The

professional

and

business

services

industry

represents

about

14%

of

GDP

and

grew

about

15%

from

2011

to

2014.

The

manufacturing

industry

represents

about

14%

of

GDP

and

grew

about

9%

from

2011

to

2014.

Although

the

manufacturing

industry

has

grown

over

the

four

year

span,

the

rate

at

which

it

has

grown

year

over

year

has

been

declining.

This

can

mainly

be

attributed

to

developing

coutries

having

a

cheap

labor

advantage,

therefore

companies

outsource

their

manufacturing

to

countries

other

than

the

U.S.

From

a

growth

perspective,

the

construction

industry

had

the

highest

growth

than

any

other

industry

at

18%.

Although

they

recorded

the

highest

growth,

their

industry

growth

growth

has

been

decreasing

year

over

year.

On

the

other

hand,

indutries

like

utilities

and

mining

have

experienced

lower

growth,

but

consistenet

increases

in

year

over

year

growth.

The

utility

inudstry

only

experienced

7%

growth

from

2011

to

2014,

but

their

growth

trend

is

positive

at

8%.

The

mining

industry

experienced

15%

growth

from

2011

to

2014

and

their

growth

trend

has

been

positive

at

3%.

Industries

that

have

had

large

negative

growth

trends

are

agriculture,

construction,

trade

and

manufacturing.

Percent

Growth

(2011-2014)

United States 12.3 15,773,516$ 100.0%

Texas 22 1,467,342$ 9.3%

Colorado 15 279,650$ 1.8%

Oklahoma 13.2 162,377$ 1.0%

Utah 13.4 128,178$ 0.8%

North Dakota 36.2 48,233$ 0.3%

Area

2014 GDP

(Millions)

% of U.S.

Economy

4.

4

Although

most

of

the

U.S.

GDP

between

2011

and

2014

came

from

the

financial

activity

industry,

that

was

not

the

case

for

job

growth.

The

professional

and

business

services

industry

is

the

largest

industry,

other

than

the

government

from

an

employment

standpoint.

The

professional

and

business

services

industry

represents

12%

of

the

private

jobs

and

grew

about

12%

since

2002.

The

healthcare

and

social

assistance

industry

represents

12%

of

private

industry

jobs

and

has

grown

25%

since

2002.

Forward

looking,

health

care

and

social

assistance

had

the

highest

projected

job

growth

from

2012

to

2022

with

a

growth

rate

of

about

29%.

Some

reasons

this

could

be

the

case

is

the

shift

towards

an

older

demographic

creating

more

care

needs

and

the

implementation

of

Obamacare

(ACA)

bringing

more

customers

to

healthcare

companies.

Some

of

the

areas

that

could

benefit

from

healthcare

growth

are

Houston,

TX;

Philadelphia,

PA;

Boston,

MA;

Denver,

CO

and

Fargo,

ND.

Following

right

along,

construction

is

also

projected

to

grow

at

about

29%

between

that

time

period

as

well.

Although

the

U.S.

economy

is

considered

to

be

sluggish,

it

is

continuing

to

grow,

and

the

construction

industry

is

an

industry

highly

correlated

with

GDP

growth.

Some

of

the

areas

that

could

benefit

from

the

increase

in

construction

are

New

York,

NY;

Dallas,

TX;

Washington,

D.C.

and

Atlanta,

GA.

On

the

other

hand,

some

of

the

industries

where

employment

fell

by

21%

were

agriculture

and

manufacturing.

States

that

have

large

exposure

to

the

agriculture

industry

are

Rhode

Island,

Idaho,

New

Mexico

and

Alaska

and

states

that

have

large

exposure

to

the

manufacturing

industry

are

Indiana,

Wisconsin,

Michigan,

Iowa

and

Alabama.

As

we

look

towards

future

investments

in

municipal

bonds,

states

with

large

exposure

to

these

declining

industries

will

certainly

be

a

factor

in

determining

final

investment.

5.

5

Population

Trends

State

U.S.

population

grew

at

an

average

rate

of

0.76%

and

a

total

rate

of

3%

from

2010

to

2014.

Twenty-‐eight

states

had

population

growth

less

than

the

U.S

and

thirty-‐one

states

had

population

outflows.

The

most

notable

states

with

outflows

were

Alaska,

Washington,

D.C.,

New

Mexico,

Wyoming

and

Connecticut.

On

the

contrary,

the

states

with

the

most

notable

population

inflows

were

Nevada,

North

Dakota,

Arizona,

Idaho

and

South

Carolina.

It

is

interesting

to

see

the

states

that

have

seen

the

highest

population

outflows

also

have

some

of

the

highest

outstanding

debt

per

capita.

As

mentioned

earlier,

California

is

the

largest

state

from

a

GDP

standpoint

and

as

we

can

see

from

the

chart

on

our

right,

it

is

also

the

largest

state

from

a

population

standpoint.

Most

notably,

the

state’s

population

that

grew

the

most

over

this

time

period

was

Texas.

The

reason

that

Texas’

population

grew

at

such

a

high

rate

is

because

of

the

growth

in

the

utility

industry

and

mining

industry.

Utility

and

mining

industry

growth

was

also

prominent

in

North

Dakota

where

it

grew

about

107%

and

was

a

large

factor

in

their

10%

population

growth

since

2010.

Population

growth

and

trends

carry

a

lot

of

weight

when

looking

at

this

type

of

data.

Population

growth

gives

us

an

indication

as

to

where

people

have

been

moving

to

and

the

trend

helps

us

to

gage

a

better

indication

as

to

where

people

are

headed

to

in

the

future.

State Population Growth Since 2010 Trend

California 38,802,500 3.9% -0.01%

Texas 26,956,958 6.8% 0.07%

Florida 19,893,297 5.5% 0.14%

New York 19,746,227 1.8% -0.37%

Illinois 12,880,580 0.3% -0.22%

Pennsylvania 12,787,209 0.6% -0.21%

Ohio 11,594,163 0.5% 0.15%

Georgia 10,097,343 3.9% 0.01%

North Carolina 9,943,964 4.0% 0.00%

Michigan 9,909,877 0.3% 0.13%

Top 10 States by Population

State Population Growth Since 2010 Trend

North Dakota 739,482 9.7% 0.54%

District of Columbia 658,893 8.9% -1.01%

Texas 26,956,958 6.8% 0.07%

Colorado 5,355,866 6.1% 0.18%

Utah 2,942,902 6.1% -0.10%

Florida 19,893,297 5.5% 0.14%

Nevada 2,839,099 5.0% 1.15%

Arizona 6731484 5.0% 0.50%

Washington 7,061,530 4.7% 0.07%

South Dakota 853,175 4.5% -0.07%

Top 10 States by Growth

6.

6

Metropolitan

Area

Metropolitan

areas

(metro

areas)

have

always

been

viewed

as

the

most

populated

areas

given

the

mass

amount

of

employers

in

those

areas.

As

we

approached

2015

however,

that

trend

has

been

reversing.

The

average

population

growth

trend

for

all

U.S.

metro

areas

has

been

flat

since

2010

and

there

has

been

total

population

outflows

from

metro

areas

of

-‐0.24%.

Based

on

population

growth

in

metro

areas

from

2010

to

2014,

there

seems

to

be

a

negative

growth

trend.

To

understand

more

about

what

metro

areas

are

causing

this

negative

trend,

we

will

dig

into

growth

data

for

the

largest

metro

areas,

highest

growth

metro

areas,

and

metro

areas

with

the

best

and

worst

trends.

The

top

five

populated

metro

areas

are

New

York-‐Newark-‐Jersey

City,

NY-‐NJ-‐PA;

Los

Angeles-‐Long

Beach-‐Anaheim,

CA;

Chicago-‐Naperville-‐Elgin,

IL-‐IN-‐WI;

Dallas-‐Fort

Worth-‐Arlington,

TX

and

Houston-‐

The

Woodlands-‐Sugar

Land,

TX.

On

average,

population

in

those

these

areas

grew

about

4%

from

2010

to

2014

with

the

Houston-‐The

Woodlands-‐Sugar

Land

metro

area

being

the

highest

at

9%

and

Chicago-‐

Naperville-‐Elgin

being

the

lowest

at

0.89%.

The

average

population

growth

for

these

areas

showed

a

flat

trend

and

total

negative

outflows.

Only

the

two

metro

areas

of

Dallas-‐Fort

Worth-‐Arlington

and

Houston-‐The

Woodlands-‐Sugar

Land

have

positive

population

growth

trends

since

2010.

This

data

shows

that

the

population

growth

that

large

metro

areas

were

once

seeing

is

slowing

down

and

in

some

cases

non-‐existent.

Given

the

slow

and

flat

population

growth

in

metro

areas,

there

are

some

bright

spots

in

the

less

populated

metro

areas.

The

top

five

metro

areas

that

have

seen

the

highest

growth

since

2010

have

been

The

Villages,

FL;

Midland,

TX;

Austin-‐Round

Rock,

TX;

Odessa,

TX

and

Myrtle

Beach-‐Conway-‐North

Myrtle

Beach,

SC-‐NC.

They

averaged

population

growth

of

14%

since

2010

and

have

had

both

an

average

and

total

population

inflow

trend.

The

trend

of

a

metro

areas

population

is

the

best

indication

of

future

metro

area

migration

as

population

projections

are

not

released

by

the

government.

The

top

five

metro

areas

who

have

shown

strong

positive

growth

trends

since

2010

are

Punta

Gorda,

FL;

Panama

City,

FL;

Jacksonville,

NC;

Hilton

Head

Island-‐Bluffton-‐Beaufort,

SC

and

Bend-‐Redmond,

OR.

These

metro

areas

although

smaller

in

population,

have

experienced

a

positive

growth

trend

and

have

had

population

growth

of

about

6%

since

2010.

Most

of

the

metro

areas

with

strong

population

growth

trends

are

concentrated

in

Florida,

North

Carolina

and

South

Carolina.

These

areas

have

attracted

migration

primary

from

retirees

looking

for

a

lower

tax

structure

and

cost

of

living,

but

also

because

they

are

seen

as

more

attractive

areas

for

the

younger

population.

On

the

contrary,

there

are

also

some

less

populated

metro

areas

that

have

seen

tremendous

population

outflows.

These

metro

areas

consist

of Columbus,

GA-‐AL,

Manhattan,

KS,

Yuma,

AZ,

Kennewick-‐

Richland,

WA

and

Hinesville,

GA.

Although

these

areas

have

had

average

population

growth

of

5.5%

since

2010,

they

are

seeing

the

growth

decline.

With

a

large

negative

growth

trend,

these

areas

have

the

largest

population

outflows.

For

more

metro

area

population

data,

please

see

Appendix

A1.

7.

7

Tax,

Income

and

Debt

Metrics

States

that

have

high

state

and

local

tax

burdens

seem

to

also

have

high

per

capita

income

as

indicated

on

the

two

charts

to

the

right.

As

we

saw

from

the

state

population

growth

charts

before,

states

like

Connecticut

and

Rhode

Island,

where

population

growth

has

been

slow

could

be

because

of

high

state

and

local

tax

burdens.

Net

Tax-‐

Supported

Debt

Per

Capita

(NTSD)

is

a

good

indication

of

a

state’s

debt

outstanding.

A

similar

trend

is

revealed

here

from

the

charts

above

as

we

see

states

like

CT,

MA,

NY

and

NJ

in

the

top

ranks.

When

taxes

are

tied

up

in

debt,

it

sometimes

can

limit

the

state’s

ability

to

use

it

for

growth

and

expansion

projects.

As

this

may

be

the

case

on

certain

occasions,

low

NTSD

does

not

necessarily

mean

more

spending

to

come

in

the

future.

States

have

been

conservative

when

issuing

debt

even

given

the

low

interest

rate

environment.

Their

debt

issuance

has

been

targeted

toward

refinancing

as

they

would

like

to

spend

more

on

education

and

healthcare

in

the

future.

Another

metric

similar

to

NTSD

is

total

debt

per

capita,

which

brings

together

the

NTSD

debt

as

well

as

any

other

debt

outstanding.

Puerto

Rico

and

Washington,

D.C.,

the

two

municipalities

that

that

have

the

highest

NTSD

also

have

the

highest

total

debt

outstanding.

Puerto

Rico

leads

the

pack

with

$27,934

per

capita.

States

like

Connecticut,

Hawaii,

Illinois

and

Rhode

Island

who

are

seen

as

economically

troubled

states

also

have

very

high

total

debt

per

capita.

Some

states

with

low

debt

per

capita

include

South

Dakota,

Tennessee,

North

Carolina

and

Nebraska.

Florida

and

Texas

also

have

relatively

low

total

debt

per

capita

and

could

be

poised

for

strong

economic

growth

in

the

future.

State 2011 2010 Change

U.S. Average $ 4,217 $ 4,112 2.6%

Connecticut $ 7,150 $ 6,984 2.4%

New Jersey $ 6,675 $ 6,689 -0.2%

Dist. Of Columbia $ 6,641 $ 5,991 10.8%

New York $ 6,622 $ 6,375 3.9%

Maryland $ 5,598 $ 5,234 7.0%

Massachusetts $ 5,586 $ 5,422 3.0%

California $ 5,136 $ 4,934 4.1%

Minnesota $ 4,858 $ 4,727 2.8%

Rhode Island $ 4,676 $ 4,627 1.1%

Illinois $ 4,658 $ 4,512 3.2%

Total State- Local

Taxes Per Capita

State 2011 2010

Change

U.S. Average 42,473$ 41,146$ 3.2%

Dist. Of Columbia 68,795$ 64,756$ 6.2%

Connecticut 60,287$ 56,914$ 5.9%

New Jersey 54,422$ 53,869$ 1.0%

Massachusetts 54,321$ 51,991$ 4.5%

Maryland 52,805$ 51,329$ 2.9%

New York 52,417$ 49,935$ 5.0%

Wyoming 50,805$ 47,900$ 6.1%

Virginia 48,498$ 46,872$ 3.5%

Alaska 47,354$ 46,098$ 2.7%

New Hampshire 47,349$ 45,864$ 3.2%

Per Capita Income

8.

8

Think-‐‑Tank

Analysis

Brookings

Institute

William

Frey

from

the

Brooking

Institute

is

an

expert

on

U.S.

Census

data,

migration

and

urban

and

metropolitan

demographics

as

well

as

many

other

areas.

In

a

recent

study

regarding

America’s

Young

Adults,

Frey

voiced

his

opinion

on

where

the

millennial

generation

is

migrating.

Frey

refers

to

the

young/millennial

generation

as

those

from

25-‐29

years

old

and

his

belief

is

that

this

age

group

is

moving

long

distance

rather

than

short

distance.

The

question

is

where

are

they

going?

Technology

has

been

the

trend

over

the

past

couple

of

years

and

millennials

are

moving

to

knowledge

base

areas

and

high

tech

area’s

because

it

offers

them

more

of

a

youthful

appeal.

Areas

that

have

these

types

of

characteristics

are

Washington,

D.C.,

Houston,

Denver

and

Austin.

The

main

reason

that

they

are

moving

to

these

areas

is

for

jobs.

In

addition

to

this,

the

reason

that

they

can

afford

to

make

long

distance

moves

is

because

they

do

not

have

any

“baggage”

as

Frey

calls

it.

Essentially,

they

have

no

reason

to

stay

where

they

currently

are

and

therefore

have

the

ability

to

relocate.

Young

adults

are

seen

as

a

leading

indicator

as

to

where

the

population

shift

will

be

in

the

future.

Two

of

the

places

that

he

believes

will

see

the

most

population

inflows

will

be

Charlotte,

NC

and

Atlanta,

GA

because

of

their

younger

population

and

growing

economies.

ALEC

Laffer

Report

–

2015

The

ALEC

Laffer

report

is

a

study

done

by

three

economists

who

analyze

and

project

current

and

future

state

performance

based

on

15

policy

variables

and

3

performance

variables.

Their

theory

is

that

states

that

spend

less

and

tax

less

experience

more

economic

growth

than

those

who

spend

and

tax

more.

Once

the

states

are

ranked

based

on

the

15

policy

objectives,

they

are

weighted

for

state

gross

domestic

product,

absolute

domestic

migration

and

non-‐farm

payroll.

On

the

next

page,

you

will

find

two

sets

of

charts

representing

current

state

economic

performance

as

well

as

projected

state

economic

performance.

Many

of

the

states

with

the

highest

economic

outlook

are

states

that

we

believe

will

have

future

economic

success

too.

9.

9

Economic

Performance

and

Outlook

Rankings

The

three

variables

for

measuring

state

performance

were

GDP

growth,

migration,

and

non-‐farm

payroll

growth.

The

Top

10

states

showed

average

GDP

growth

of

about

79%,

compared

to

about

34%

for

the

Bottom

10,

migration

inflows

of

185,209

compared

to

outflows

of

178,748

and

non-‐farm

payroll

growth

of

about

16%

compared

to

0.08%.

The

major

variables

that

separate

the

Top

10

from

the

Bottom

10

are:

lower

taxes,

no

progressive

personal

income

tax,

low

top

marginal

and

corporate

tax

rates,

high

sales

tax

burden,

but

a

low

property

tax

burden

and

are

right

to

work

states.

The

economic

outlook

ranking

given

by

ALEC

Laffer

is

out

of

50

and

the

Top

10

have

an

average

of

16.5

while

to

Bottom

10

have

an

average

of

33.4.

For

more

data

on

specific

states,

please

see

Appendix

A2.

Rank State

Rank State

1 Texas 41 Mississippi

2 North

Dakota 42 Missouri

3 Utah 43 Wisconson

4 Oklahoma 44 Maine

5 Wyoming 45 Connecticut

6 Washington 46 Illinois

7 Oregon 47 Rhode

Island

8 Montana 48 New

Jersey

9 Colorado 49 Ohio

10 North

Carolina 50 Michigan

Top

10

Economic

Performance

Rankings Bottom

10

Economic

Performance

Rankings

Rank State

Rank State

1 Utah 41 Pennsylvania

2 North

Dakota 42 Maine

3 Indiana 43 Montana

4 North

Carolina 44 California

5 Arizona 45 Oregon

6 Idaho 46 New

Jersey

7 Georgia 47 Connecticut

8 Wyoming 48 Minnesota

9 South

Dakota 49 Vermont

10 Nevada 50 New

York

Top

10

Economic

Outlook

Rankings Bottom

10

Economic

Outlook

Rankings

10.

10

Conclusion

From

2002

to

the

present

day,

the

states

who

are

big

players

in

the

mining

industry

have

seen

extraordinary

economic

growth.

Texas

and

North

Dakota

are

two

examples

of

this.

Texas

has

grown

about

21%

since

2011

and

North

Dakota

has

grown

about

36%

since

2011.

The

extraordinary

growth

these

states

saw

also

drove

their

respective

regions

to

be

strong

growth

regions

as

well.

When

taking

a

look

at

the

states

that

represent

a

large

portion

of

the

U.S.

economy,

California,

Texas

and

New

York

lead

the

pack.

Together

they

represent

a

little

bit

over

30%

of

the

U.S.

economy,

but

besides

Texas,

they

have

been

growing

at

rates

similar

to

the

U.S.

economy

as

a

whole.

The

main

reason

that

this

is

the

case

is

because

of

the

high

tax

environment

the

states

operate

in.

Population

growth

in

populated

metro

areas

has

been

slowing

down.

One

factor

behind

this

is

the

increasing

older

population

is

seeking

a

living

environment

where

they

can

enjoy

their

retirement

and

their

cost

of

living

is

low.

This

means

that

high

income

and

high

tax

states

such

as

Connecticut,

New

Jersey,

New

York

and

Massachusetts

have

seen

population

outflows

mainly

due

to

high

tax

burdens

and

costs

of

living.

Meanwhile,

states

like

North

Dakota

and

Texas

who

have

low

tax

burdens

and

somewhat

diversified

economies

have

seen

increasing

economic

growth.

Although

oil

has

been

the

driver

of

some

economies

over

the

past

couple

of

years,

economies

have

also

seen

strong

GDP

growth

in

the

finance

and

healthcare

industries.

As

one

of

the

most

advanced

economies,

the

U.S.

is

moving

toward

an

economy

focused

on

capital

markets

and

health.

The

Bureau

of

Labor

Statistics

believes

that

the

finance

and

healthcare

industry

is

poised

to

enter

a

takeoff

period

where

employment

growth

could

increase

20%

for

both

industries.

Areas

such

as

Boston,

MA;

Denver,

CO

and

Fargo,

ND

could

benefit

greatly

from

the

expected

growth

in

healthcare.

Given

all

of

the

economic

data

discussed,

we

believe

that

there

are

a

handful

of

states

to

watch

as

they

may

struggle

from

the

path

the

U.S.

economy

is

headed.

Michigan

is

the

auto

manufacturing

hub

and

could

either

benefit

from

the

growing

economy

or

struggle

from

the

declining

manufacturing

industry.

Tennessee

was

just

voted

the

best

place

to

manufacture

automobiles

and

is

seen

as

an

attractive

contender

to

Michigan

with

its

low

tax

environment.

Connecticut,

New

Jersey

and

New

York

are

also

on

the

watch

list

as

they

operate

in

an

extremely

high

tax

rate

environment.

The

millennial

generation

is

in

the

search

for

areas

with

youthful

population

and

technological

innovation

and

the

older

population

is

in

search

for

areas

with

low

taxes

and

low

costs

of

living.

So,

the

final

question

to

ask

is

what

states

are

going

to

benefit

from

future

economic

growth:

Texas,

particularly

Houston

and

Dallas

are

two

areas

that

have

experienced

strong

economic

growth,

as

well

as

population

growth

and

the

trends

seem

to

be

in

their

favor.

South

Carolina

and

North

Carolina

are

two

states

that

have

low

debt

outstanding,

strong

migration

trends

and

a

large

financial

activity

industry.

Florida

has

always

had

strong

population

growth

and

is

a

pro-‐business

state.

Georgia

was

most

recently

voted

the

best

state

to

do

business

and

a

growing

economy

with

a

youthful

appeal.

Lastly,

even

though

North

Dakota

saw

strong

economic

growth

in

recent

years,

it

is

still

in

a

goof

position

to

grow

with

large

healthcare,

financial

activity

and

mining

industries

and

strong

migration

trends.

11.

11

Appendix

A1

State 2014 Growth since 2010 Trend

The Villages, FL Metro Area 114,350 21.3% 0.84%

Midland, TX Metro Area 161,290 13.7% 0.32%

Austin-Round Rock, TX Metro Area 1,943,299 12.5% -0.10%

Odessa, TX Metro Area 153,904 12.3% 1.04%

Myrtle Beach-Conway-North Myrtle Beach, SC-NC Metro Area 417,668 10.3% 1.32%

Bismarck, ND Metro Area 126,597 9.9% 0.23%

St. George, UT Metro Area 151,948 9.8% 0.63%

Auburn-Opelika, AL Metro Area 154,255 9.6% -0.70%

Cape Coral-Fort Myers, FL Metro Area 679,513 9.5% 0.99%

Crestview-Fort Walton Beach-Destin, FL Metro Area 258,042 9.3% 0.62%

Metropolitan Area 2014 Growth since 2010 Trend

New York-Newark-Jersey City, NY-NJ-PA Metro Area 20,092,883 2.52% -0.3%

Los Angeles-Long Beach-Anaheim, CA Metro Area 13,262,220 3.25% -0.2%

Chicago-Naperville-Elgin, IL-IN-WI Metro Area 9,554,598 0.89% -0.1%

Dallas-Fort Worth-Arlington, TX Metro Area 6,954,330 7.77% 0.0%

Houston-The Woodlands-Sugar Land, TX Metro Area 6,490,180 9.10% 0.6%

Philadelphia-Camden-Wilmington, PA-NJ-DE-MD Metro Area 6,051,170 1.34% -0.2%

Washington-Arlington-Alexandria, DC-VA-MD-WV Metro Area 6,033,737 6.49% -0.9%

Miami-Fort Lauderdale-West Palm Beach, FL Metro Area 5,929,819 6.15% -1.0%

Atlanta-Sandy Springs-Roswell, GA Metro Area 5,614,323 5.8% 0.3%

Boston-Cambridge-Newton, MA-NH Metro Area 4,732,161 3.67% -0.2%

Metropolitan Area 2014 Growth since 2010 Trend

The Villages, FL Metro Area 114,350 21.3% 0.8%

Midland, TX Metro Area 161,290 13.7% 0.3%

Austin-Round Rock, TX Metro Area 1,943,299 12.5% -0.1%

Odessa, TX Metro Area 153,904 12.3% 1.0%

Myrtle Beach-Conway-North Myrtle Beach, SC-NC Metro Area 417,668 10.3% 1.3%

Bismarck, ND Metro Area 126,597 9.9% 0.2%

St. George, UT Metro Area 151,948 9.8% 0.6%

Auburn-Opelika, AL Metro Area 154,255 9.6% -0.7%

Cape Coral-Fort Myers, FL Metro Area 679,513 9.5% 1.0%

Crestview-Fort Walton Beach-Destin, FL Metro Area 258,042 9.3% 0.6%

Metropolitan Area 2014 Growth since 2010 Trend

Punta Gorda, FL Metro Area 168,474 5.34% 2.33%

Panama City, FL Metro Area 194,929 5.30% 2.04%

Jacksonville, NC Metro Area 187,589 4.47% 1.96%

Hilton Head Island-Bluffton-Beaufort, SC Metro Area 203,022 8.05% 1.53%

Bend-Redmond, OR Metro Area 170,388 7.96% 1.43%

North Port-Sarasota-Bradenton, FL Metro Area 748,708 6.43% 1.41%

Sebastian-Vero Beach, FL Metro Area 144,755 4.72% 1.39%

Myrtle Beach-Conway-North Myrtle Beach, SC-NC Metro Area 417,668 10.31% 1.32%

Prescott, AZ Metro Area 218,844 3.96% 1.29%

Deltona-Daytona Beach-Ormond Beach, FL Metro Area 609,939 3.26% 1.28%

Metropolitan Area 2014 Growth since 2010 Trend

Columbus, GA-AL Metro Area 314,005 5.92% -3.03%

Manhattan, KS Metro Area 98,091 5.09% -2.72%

Yuma, AZ Metro Area 203,247 3.12% -2.20%

Kennewick-Richland, WA Metro Area 274,295 7.32% -1.96%

Hinesville, GA Metro Area 82,311 6.39% -1.87%

Watertown-Fort Drum, NY Metro Area 119,103 2.15% -1.80%

El Paso, TX Metro Area 836,698 3.67% -1.74%

Fayetteville, NC Metro Area 377,939 2.78% -1.44%

Valdosta, GA Metro Area 143,317 2.29% -1.31%

Fairbanks, AK Metro Area 99,357 1.21% -1.29%

Top 10 Metropolitan Area's by Population

Top 10 Metropolitan Area's by Growth

Top 10 Metropolitan Area's by Growth Trend

Bottom 10 Metropolitan Area's by Growth Trend

12.

12

A2

State

Gross

Domestics

Product

Growth Absolute

Domestic

Migration Non-‐Farm

Payroll

Texas 81.70% 1229173 20.50%

North

Dakota 149.40% 32185 35.00%

Utah 76.10% 78474 24.00%

Oklahoma 71.00% 97612 11.70%

Wyoming 111.35% 31416 15.80%

Washington 57.30% 275864 11.00%

Oregon 71.40% 174782 7.10%

Montana 69.40% 48162 11.70%

Colorado 51.30% 272722 11.60%

North

Carolina 50.50% 655663 8.30%

State

Gross

Domestics

Product

Growth Absolute

Domestic

Migration Non-‐Farm

Payroll

Mississippi 41.80% -‐41744 0.00%

Missouri 34.00% -‐6229 2.50%

Wisconson 37.70% -‐56632 2.30%

Maine 30.00% -‐1063 -‐1.00%

Connecticut

45.20% 584103 9.10%

Illinois 35.60% -‐646867 0.50%

Rhode

Island 31.60% -‐69187 -‐2.80%

New

Jersey 34.60% -‐524205 -‐1.10%

Ohio 32.60% -‐397184 -‐2.30%

Michigan 14.40% -‐628472 -‐6.40%

Top

10

Economic

Performance

Rankings,

2003-‐2013

Bottom

10

Economic

Performance

Rankings,

2003-‐2013

UT ND ID NC AZ IH GA WY SD NV

Top

Marginal

Personal

Income

Tax

Rate 5.00% 3.22% 5.07% 5.75% 4.54% 7.40% 6.00% 0.00% 0.00% 0.00%

Top

Marginal

Corporate

Income

Tax

Rate 5.00% 4.53% 7.00% 5.00% 6.00% 7.40% 6.00% 0.00% 0.00% 0.00%

Personal

Income

Tax

Progressivity 0 9.12 0.68 5.75 10.62 13.4 6.53 0 0 0

Property

Tax

Burden 26.98 22.01 26.68 24.49 29.21 25.57 28.56 45.43 26.81 27.2

Sales

Tax

Burden 25.17 35.62 27.33 21.54 36.74 22.48 25.25 41.38 30.46 35.96

Remaining

Tax

Burden 15.59 19.68 18.54 16.89 12.58 15.18 11.18 12.2 17.76 35.54

Estate/Inheritance

Tax

Levied? No No No No No No No No No No

Recently

Legislated

Tax

Changes 0.17 -‐3.78 -‐0.37 -‐0.43 -‐0.24 -‐0.34 -‐0.3 2.34 0 0

Debt

Service

as

a

Share

of

Tax

Revenue 7.80% 2.70% 8.60% 7.50% 9.80% 5.40% 7.50% 2.50% 7.00% 10.70%

Public

Employees

Per

10,000 488.8 625.1 486.3 558 427.8 496 512.6 865.5 548.3 367.6

State

Liability

System

Survey 69.7 69.8 69 65.8 66.8 70.5 64 72.6 69.5 57

State

Minimum

Wage 7.25 7.25 7.25 7.25 8.05 7.25 7.25 7.25 8.5 8.25

Average

Workers’

Compensation

Costs 1.31 0.88 1.06 1.85 1.6 2.01 1.75 1.76 1.86 1.26

Right-‐to-‐Work

State? Yes Yes Yes Yes Yes Yes Yes Yes Yes Yes

Number

of

Tax

Expenditure

Limits 1 0 1 1 2 1 0 0 1 2

PA ME MO CA OE NJ CT MN VM NY

Top

Marginal

Personal

Income

Tax

Rate 6.99% 7.95% 6.90% 13.30% 10.62% 9.97% 6.70% 9.85% 8.95% 12.70%

Top

Marginal

Corporate

Income

Tax

Rate 17.03% 8.93% 6.75% 88.40% 11.25% 9.00% 9.00% 9.80% 8.50% 17.16%

Personal

Income

Tax

Progressivity 0 19.47 18.02 38.34 15.54 24.81 7.67 18.42 28.69 12.66

Property

Tax

Burden 29.98 45.5 36.26 29.72 33.69 54.07 44.8 31.75 50.32 46.19

Sales

Tax

Burden 17.25 20.38 0 23.6 0 16.92 17.98 20.44 12.83 24.21

Remaining

Tax

Burden 24.04 19.59 23.77 16.21 22.87 14.22 17.83 24.58 28.85 20.59

Estate/Inheritance

Tax

Levied? Yea Yes No No Yes Yes Yes Yes Yes Yes

Recently

Legislated

Tax

Changes 1.82 -‐0.17 -‐0.13 -‐0.47 0.88 -‐0.39 1.66 2.36 2.6 -‐1.48

Debt

Service

as

a

Share

of

Tax

Revenue 8.60% 6.00% 5.80% 10.50% 8.90% 6.60% 7.80% 7.50% 5.30% 9.40%

Public

Employees

Per

10,000 444.9 548 562 446.3 482.8 531.2 516.9 509.7 632.2 596.4

State

Liability

System

Survey 56.3 69.2 52.2 50.6 62.6 60.1 63.8 71.4 67.1 66.4

State

Minimum

Wage 7.25 7.5 8.05 9 9.25 8.38 9.15 8 9.15 8.75

Average

Workers’

Compensation

Costs 2 2.15 2.21 3.48 1.37 2.82 2.87 1.99 2.33 2.75

Right-‐to-‐Work

State? No No No No No No No No No No

Number

of

Tax

Expenditure

Limits 0 1 0 2 2 1 1 0 0 0

Top

10

States

for

Economic

Outlook

Rnakings

Bottom

10

States

for

Economic

Outlook

Rnakings