Download as PDF, PPTX

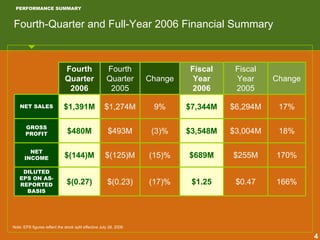

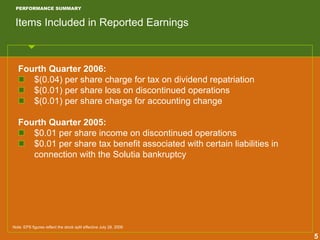

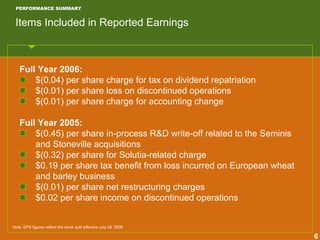

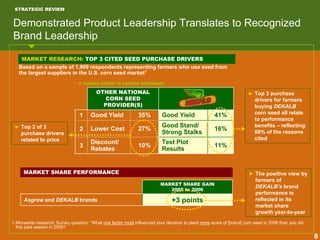

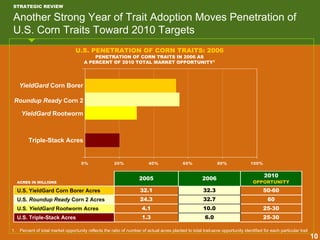

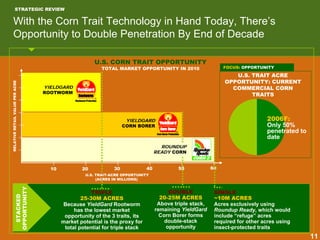

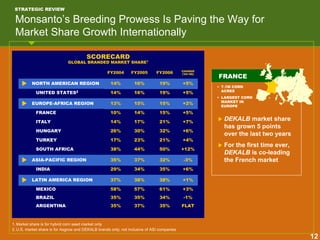

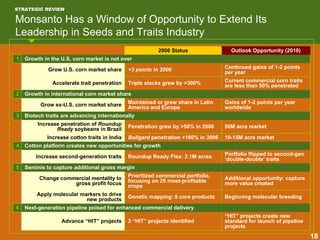

This document provides a financial summary and strategic review for Monsanto for the fourth quarter and full year of 2006. Some key points: - Net sales for Q4 2006 were $1.39 billion, up 9% from Q4 2005. Full year 2006 net sales were $7.34 billion, up 17% from 2005. - Reported EPS for Q4 2006 was $-0.27 per share, down 17% from Q4 2005. Full year 2006 reported EPS was $1.25 per share, up 166% from 2005. - The company achieved market share gains in key crops like US corn and soybeans as well as international markets like France and Italy. - Opportunities for continued