Recommended

More Related Content

More from finance28

More from finance28 (20)

Recently uploaded

Recently uploaded (20)

monsanto 05-05-06

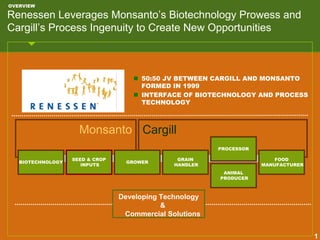

- 1. OVERVIEW Renessen Leverages Monsanto’s Biotechnology Prowess and Cargill’s Process Ingenuity to Create New Opportunities 50:50 JV BETWEEN CARGILL AND MONSANTO FORMED IN 1999 INTERFACE OF BIOTECHNOLOGY AND PROCESS TECHNOLOGY Monsanto Cargill PROCESSOR SEED & CROP GRAIN FOOD BIOTECHNOLOGY GROWER INPUTS HANDLER MANUFACTURER ANIMAL PRODUCER Developing Technology & Commercial Solutions 1

- 2. OVERVIEW Increased Ethanol Demand Will Set The Stage for Domestic Competition Between Feed and Fuel MARKET DISTRIBUTION FOR U.S. CORN U.S. ETHANOL MARKET OUTLOOK A NEAR DOUBLING IN THE DEMAND FOR CORN USED IN ETHANOL IN THE NEXT 12 5 FIVE YEARS WILL 4.5 SQUEEZE CURRENT CORN 10 BILLIONS OF GALLONS BILLIONS OF BUSHELS 4 SUPPLIES 3.5 8 3 2006 2012 6 2.5 2 48% 51% FEED 4 1.5 FUEL 1 20% 31% 2 ALCOHOL 0.5 0 0 18% 9% EXPORTS 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 ETHANOL PRODUCED CORN USED FOR ETHANOL ENDING 16% 6% STOCK OTHER 3% 3% INCLUDING FOOD Source: Proexporter Network and Renessen Estimates 2

- 3. OVERVIEW Corn Is Distributed To Four Major Downstream Markets CORN DISTRIBUTION BY MAJOR MARKET FOCUS: CONVENTIONAL DRY MILL PROCESS Yellow #2 Hammer Yellow #2 Hammer Distillation Ethanol Distillation Ethanol Elevator Fermentation Elevator Fermentation Corn Mill Corn Mill Drying Drying Exports Wet Mill Feed Mill Exports Wet Mill Feed Mill DDGs DDGs Swine Poultry Cattle Swine Poultry Cattle Cattle Cattle 3 DDG = DISTILLERS DRIED GRAIN

- 4. OVERVIEW Market Discontinuities Create Opportunity For Value Creation FOCUS: IOWA OVERVIEW ETHANOL PLANTS ARE BEGINNING TO BE PLACED IN AREAS WHERE CORN PRODUCTION HAS TRADITIONALLY BEEN USED AS FEED IN HOG PRODUCTION DUBUQUE THE DRAW ON CORN FROM THE ETHANOL- SIOUX ANIMAL FEED DYNAMIC WILL CITY CEDAR CREATE “MICRO RAPIDS COMPETITIVE MARKETS” DRIVING IOWA COMPETITION FOR CITY AMES LOCAL CORN DAVENPORT OPPORTUNITY ETHANOL DES PRODUCTION THAT MOINES ALSO CREATES A VALUABLE FEED STREAM FOR HOGS BURLINGTON CAN BRIDGE THE LOCALIZED DEMAND SHORTAGES FOR CORN AND CREATE NEW VALUE ETHANOL PLANTS UNDER ETHANOL PLANTS IN WET MILL CONSTRUCTION PRODUCTION MOST LEAST INTENSITY OF HOG PRODUCTION: INTENSE INTENSE Source: USDA and Renessen Estimates 4

- 5. TECHNOLOGICAL LEADERSHIP Nutrient Rich Corn Is the Precursor to Value in Renessen’s New Corn Processing Technology KEY NUTRIENT COMPOSITION Tryptophan Protein Oil Lysine Launch %Wt % Wt % Wt Date % Wt COMMODITY 3.5 .25 .056 8.0 CORN MAVERATM HIGH 6.5 .40 .070 8.5 2007 VALUE CORN WITH LYSINE First crop based biotech product for animal feed Recently deregulated in the US Coupled with Renessen’s corn processing technology brings unique value 5

- 6. TECHNOLOGICAL LEADERSHIP Renessen Is Developing New Fractionation Technology Increasing Refinery Yield and Co-Product Values RENESSEN FRACTIONATION CONVENTIONAL DRY MILL PROCESS PROCESS NUTRIENT NUTRIENT Hammer Hammer THE RENESSEN DENSE Distillation Ethanol DENSE Elevator Fermentation Distillation Ethanol Elevator Fermentation FRACTIONATION TECHNOLOGY Mill CORN Mill CORN BOLTS ON TO A CONVENTIONAL DRY MILL PROCESS Drying Drying STEP 1: RENESSEN FRACTIONATION AND EXTRACTION PROCESS START WITH A NUTRITIONALLY DENSE CORN DEVELOPED THROUGH HIGHLY HIGHLY HIGH PROTEIN D BIOTECH AND ADVANCED C FERMENTABLE FERMENTABLE Fractionation LOW OIL DDGs Fractionation BREEDING TECHNOLOGIES FRACTION FRACTION STEP 2: High Oil High Oil FRACTIONATE IT THROUGH A Fraction Fraction NOVEL PROCESS TECHNOLOGY Oil Oil Nutrient-Rich STEP 3: Nutrient-Rich Extraction Extraction Meal Meal DELIVER FOUR HIGH VALUE REVENUE STREAMS A: CORN OIL AND / OR BIODIESEL Corn Oil Corn Oil B: HIGH VALUE SWINE AND POULTRY FEED C: HIGHLY FERMENTABLE STARCH D: HIGH PROTEIN, LOW OIL DDGs HIGH VALUE SWINE A B CORN OIL FOR AND POULTRY FEED FOOD AND / OR BIODIESEL 6