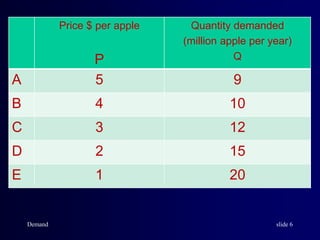

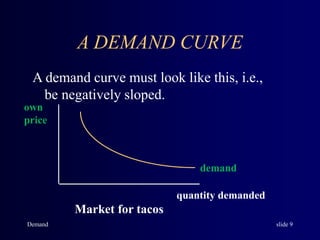

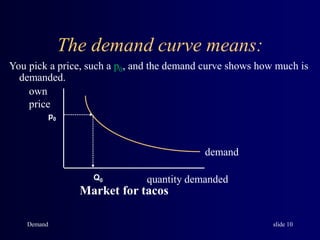

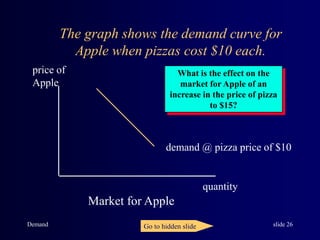

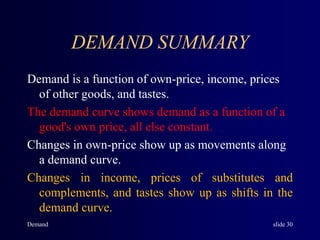

The document discusses the standard model of demand. Demand is defined as the quantity of a good that consumers are willing and able to purchase at various prices over a given period of time. A demand curve graphs the relationship between the price of a good and the quantity demanded while holding all other factors that influence demand constant. The demand curve will slope downward, as higher prices are associated with lower quantities demanded according to the law of demand. Shifts in factors like income, prices of related goods, and preferences can shift the demand curve and thereby change the quantity demanded at each price level.