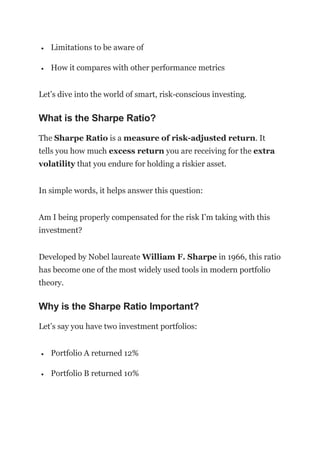

Investing isn’t just about making the most returns — it’s about how much risk you’re taking to earn those returns. This is where the Sharpe Ratio comes into play. Whether you’re a beginner investor, a financial analyst, or a portfolio manager, understanding and using the Sharpe Ratio can help you make better, risk-adjusted investment decisions.