This document provides an overview of national office market metrics for the 4th quarter of 2014. Some key findings include:

- Manhattan had the highest average asking rent of $69.32/sf, followed by San Francisco at $56/sf.

- San Francisco and Silicon Valley saw the largest year-over-year increases in asking rents at 12.9% and 11.8% respectively.

- In terms of construction pipelines, Silicon Valley had the highest pre-leased rate at 89.2%, while Los Angeles had the lowest at 29.5%.

- Washington D.C. saw the largest year-over-year increase in leasing at 115.9%, while Atlanta saw the largest decline at

Managing Investment Return Experiences and Expectations - Greg Woods and PanelBPAS

Moderator:

Greg Woods

VP, BPAS Fiduciary Services

Panelists:

- Ralph Acampora, Director of Technical Analysis Studies, New York Institute of Finance

- Michael T. DiMarsico, SVP, National Manager, Manager Resource Consulting, Federated

- Harry Rakovski, Director - RIA & Consultant Division Northeast, Prudential Investments Management, LLC

Shift Share and Location Quotients: An Industry Sector AnalysisAndy Carswell

This presentation was given to the Valdosta/Lowndes County, GA Chamber of Commerce in Spring 2012. The presentation tracked industry growth by specific employment sectors and compared them against similar measures from more than a dozen "sister counties" throughout the Southeast U.S.

Managing Investment Return Experiences and Expectations - Greg Woods and PanelBPAS

Moderator:

Greg Woods

VP, BPAS Fiduciary Services

Panelists:

- Ralph Acampora, Director of Technical Analysis Studies, New York Institute of Finance

- Michael T. DiMarsico, SVP, National Manager, Manager Resource Consulting, Federated

- Harry Rakovski, Director - RIA & Consultant Division Northeast, Prudential Investments Management, LLC

Shift Share and Location Quotients: An Industry Sector AnalysisAndy Carswell

This presentation was given to the Valdosta/Lowndes County, GA Chamber of Commerce in Spring 2012. The presentation tracked industry growth by specific employment sectors and compared them against similar measures from more than a dozen "sister counties" throughout the Southeast U.S.

We released this 3 weeks ago and February's Report will be available soon. This delinquency report is segmented by market and property type. Page 2 contains a 6-month delinquency trend graph for each market.

net lease research report q1 2018 | The Boulder GroupThe Boulder Group

The Boulder Group’s Research Department has released a new research report providing comprehensive numbers and analysis of the 1st quarter activity in the National Net Lease Market.

Annie Williams Real Estate Report Aug-Sept 2016Jon Weaver

The major problem with all automated home estimate sites is they are limited to the data on hand. Typically, that includes only square footage, number of beds and baths, recent sales prices and assessor tax values.

What is not included are location nuances such as is the property on a quiet street or next to a main thoroughfare. Did the owners remove that cheap carpeting and replace it with hardwood floors? Were the appliances replaced with high-end

hardware? Granite countertops or tile?

Partners Trust La Cañada Grand Opening: 2014-2015 California Economic Outlook...Audie Chamberlain

Leslie Appleton-Young, Chief Economist for the CALIFORNIA ASSOCIATION OF REALTORS® (C.A.R.) 2014-2015 California Economic & Market Outlook presentation to kick off Partners Trust La Cañada Grand Opening on November, 20th 2014.

We released this 3 weeks ago and February's Report will be available soon. This delinquency report is segmented by market and property type. Page 2 contains a 6-month delinquency trend graph for each market.

net lease research report q1 2018 | The Boulder GroupThe Boulder Group

The Boulder Group’s Research Department has released a new research report providing comprehensive numbers and analysis of the 1st quarter activity in the National Net Lease Market.

Annie Williams Real Estate Report Aug-Sept 2016Jon Weaver

The major problem with all automated home estimate sites is they are limited to the data on hand. Typically, that includes only square footage, number of beds and baths, recent sales prices and assessor tax values.

What is not included are location nuances such as is the property on a quiet street or next to a main thoroughfare. Did the owners remove that cheap carpeting and replace it with hardwood floors? Were the appliances replaced with high-end

hardware? Granite countertops or tile?

Partners Trust La Cañada Grand Opening: 2014-2015 California Economic Outlook...Audie Chamberlain

Leslie Appleton-Young, Chief Economist for the CALIFORNIA ASSOCIATION OF REALTORS® (C.A.R.) 2014-2015 California Economic & Market Outlook presentation to kick off Partners Trust La Cañada Grand Opening on November, 20th 2014.

In case you missed our live broadcast of this webinar with STR, catch the presentation to help you prepare your marketing plans for 2015 with a heightened understanding of the trends and market forces impacting hotel occupancy in the year ahead.

Presenter: Brittany Baldwin, Director of Business Development, Destinations with STR

Zillow Sued Over Zestimates - June/July Real Estate ReportAMSI, San Francisco

The Robb Fleischer’s Real Estate Report – Local Market Trends San Francisco includes monthly updates regarding mortgage rates, market statistics, sales momentum, pricing momentum, trends at a glance, foreclosure statistics and more.

Strong Sales & Price Growth in August

The MLS® Home Price Index (HPI) Composite Benchmark for August 2016 was up by 17.2 per cent on a year-over-year basis. Similarly, the average selling price for all home types combined

was up by 17.7 per cent on an annual basis to $710,410. Both the MLS® HPI benchmarks and average prices for low-rise home types were up by double digits percentage-wise.

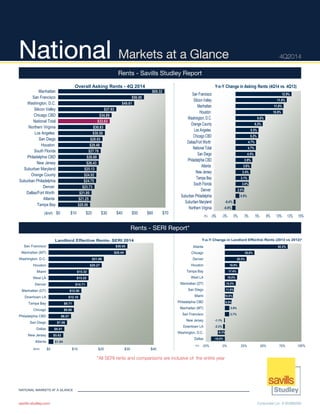

1. NATIONAL MARKETS AT A GLANCE

Corporate Lic. # 00388260savills-studley.com

National Markets at a Glance 4Q2014

Rents - Savills Studley Report

*All SERI rents and comparisons are inclusive of the entire year

$69.32

$56.00

$49.61

$37.93

$34.89

$33.63

$30.83

$30.50

$28.93

$28.48

$27.78

$26.60

$26.43

$25.13

$24.92

$24.75

$23.73

$21.80

$21.25

$20.86

$0 $10 $20 $30 $40 $50 $60 $70

Manhattan

San Francisco

Washington, D.C.

Silicon Valley

Chicago CBD

National Total

Northern Virginia

Los Angeles

San Diego

Houston

South Florida

Philadelphia CBD

New Jersey

Suburban Maryland

Orange County

Suburban Philadelphia

Denver

Dallas/Fort Worth

Atlanta

Tampa Bay

($/sf)

Overall Asking Rents - 4Q 2014

12.9%

11.8%

11.0%

10.9%

6.8%

6.2%

5.3%

5.2%

4.7%

4.7%

4.5%

3.9%

3.6%

3.4%

3.1%

3.0%

2.0%

0.9%

-0.4%

-0.8%

-5% -3% 0% 3% 5% 8% 10% 13% 15%

San Francisco

Silicon Valley

Manhattan

Houston

Washington, D.C.

Orange County

Los Angeles

Chicago CBD

Dallas/Fort Worth

National Total

San Diego

Philadelphia CBD

Atlanta

New Jersey

Tampa Bay

South Florida

Denver

Suburban Philadelphia

Suburban Maryland

Northern Virginia

Y-o-Y Change in Asking Rents (4Q14 vs. 4Q13)

(%)

$30.05

$29.44

$21.06

$20.27

$15.32

$15.22

$14.71

$12.50

$12.10

$9.71

$9.66

$8.57

$7.06

$6.01

$5.62

$1.84

$0 $10 $20 $30 $40

San Francisco

Manhattan (MT)

Washington, D.C.

Houston

Miami

West LA

Denver

Manhattan (DT)

Downtown LA

Tampa Bay

Chicago

Philadelphia CBD

San Diego

Dallas

New Jersey

Atlanta

($/sf)

Landlord Effective Rents- SERI 2014

82.2%

38.8%

28.5%

18.9%

17.4%

16.0%

14.4%

11.9%

10.6%

8.9%

5.9%

5.7%

-1.1%

-2.3%

-9.3%

-18.0%

-25% 0% 25% 50% 75% 100%

Atlanta

Chicago

Denver

Houston

Tampa Bay

West LA

Manhattan (DT)

San Diego

Miami

Philadelphia CBD

Manhattan (MT)

San Francisco

New Jersey

Downtown LA

Washington, D.C.

Dallas

(%)

Y-o-Y Change in Landlord Effective Rents (2013 vs 2012)*

Rents - SERI Report*

2. NATIONAL MARKETS AT A GLANCE

Corporate Lic. # 00388260savills-studley.com

Building Sales - Cap Rates, Sales Volume, Distress & $/PSF*

$9.20

$7.90

$6.18

$4.23

$3.47

$2.95

$2.83

$2.60

$2.45

$2.43

$2.13

$1.98

$1.94

$1.85

$1.83

$1.82

$1.69

$1.06

$0.73

$0.72

Boston

Los Angeles

Chicago

Washington, D.C.

Dallas/Fort Worth

Silicon Valley

Houston

Atlanta

Northern Virginia

Denver

Seattle

Philadelphia

New Jersey

San Diego

Orange County

Phoenix

Miami

Tampa Bay

Raleigh/Durham

Suburban Maryland

$ Billions

Office Sales Volume - 2014*

$1,318

$979

$928

$819

$816

$804

$389

$356

$321

$320

$316

$309

$291

$249

$246

$240

$235

$186

$159

$15

Chicago

Los Angeles

Northern Virginia

Boston

New Jersey

Atlanta

Orange County

Philadelphia CBD

Manhattan

San Francisco

Dallas/Fort Worth

San Diego

Miami

Houston

Broward County

Seattle

Silicon Valley

Tampa Bay

Denver

Washington, D.C.

$Millions

Value of Distressed Properties

$576

$488

$367

$336

$293

$272

$258

$223

$217

$211

$210

$202

$192

$165

$155

$149

$147

$145

$142

$138

$135

$0 $100 $200 $300 $400 $500 $600

Washington, D.C.

San Francisco

Silicon Valley

Boston

Northern Virginia

Los Angeles

Seattle

San Diego

Chicago

Houston

Orange County

Miami

Philadelphia

Denver

Phoenix

Raleigh/Durham

Tampa Bay

Atlanta

Suburban Maryland

New Jersey

Dallas/Fort Worth

Average Price Per Square Foot - Last Four Quarters*

($)

* Source: Real Capital Analytics

4.4%

5.1%

5.6%

5.7%

5.8%

5.9%

6.0%

6.0%

6.5%

6.7%

6.8%

6.8%

6.8%

6.9%

6.9%

7.0%

7.1%

Manhattan

San Francisco

Silicon Valley

Washington, D.C.

Seattle

Miami

Boston

Los Angeles

Orange County

San Diego

Atlanta

Northern Virginia

Philadelphia

New Jersey

Raleigh/Durham

Chicago

Tampa Bay

(%)

Average Cap Rate - Last Four Quarters

* Manhattan ($21.6 billion), San Francisco ($21.3 billion)

* Manhattan: $716

3. NATIONAL MARKETS AT A GLANCE

Corporate Lic. # 00388260savills-studley.com

Availability & Leasing

-3.2

-2.7

-2.4

-2.0

-1.8

-1.7

-1.5

-1.4

-1.4

-1.3

-1.2

-1.1

-1.0

-0.9

-0.5

0.1

0.5

0.7

0.9

0.9

-3.5 -2.5 -1.5 -0.5 0.5 1.5 2.5

Tampa Bay

San Francisco

San Diego

South Florida

Chicago CBD

Suburban Philadelphia

Manhattan

Silicon Valley

Denver

Atlanta

New Jersey

Los Angeles

National Total

Orange County

Houston

Washington, D.C.

Philadelphia CBD

Northern Virginia

Dallas/Fort Worth

Suburban Maryland

Availability Rate PP Change (Y-O-Y)

8.1%

10.5%

10.8%

14.1%

14.3%

14.6%

15.5%

16.2%

16.9%

17.5%

17.5%

17.8%

17.9%

18.5%

18.7%

18.9%

21.4%

21.7%

21.9%

27.7%

0% 10% 20% 30%

San Francisco

Silicon Valley

Manhattan

Washington, D.C.

Philadelphia CBD

Orange County

Chicago CBD

Denver

National Total

Tampa Bay

San Diego

Houston

Los Angeles

South Florida

Suburban Maryland

Suburban Philadelphia

Atlanta

Dallas/Fort Worth

Northern Virginia

New Jersey

Availability Rate Comparison

(%)

23.5%

20.9%

14.2%

10.9%

6.6%

4.5%

2.5%

1.9%

1.5%

1.0%

-2.9%

-3.1%

-8.4%

-11.4%

-13.0%

-16.2%

-21.2%

-30% -10% 10% 30%

Denver

Silicon Valley

Orange County

San Diego

Houston

Chicago

Los Angeles

Boston

Dallas/Fort Worth

Washington, D.C.

Atlanta

San Francisco

Philadelphia CBD

South Florida

Manhattan

Tampa Bay

Seattle

Y-o-Y Change in Avail. Sublet

(%)

7.8

6.3

6.2

4.7

3.5

3.4

3.4

3.1

3.0

3.0

2.9

2.7

2.7

2.7

1.7

1.5

1.1

1.1

0 4 8

Houston

Manhattan

Dallas/Fort Worth

Atlanta

New Jersey

San Francisco

Boston

Denver

Los Angeles

Orange County

Phoenix

Chicago

Seattle

Silicon Valley

Tampa Bay

San Diego

Philadelphia

Miami/Dade-County

(MSF)

Net Absorption- YTD

52.7%

12.4%

11.1%

4.9%

3.0%

2.0%

-2.1%

-4.8%

-5.3%

-6.9%

-7.9%

-16.7%

-19.5%

-22.7%

-23.7%

-24.7%

-25.8%

-27.8%

-32.3%

-40.7%

-60%-40%-20% 0% 20% 40% 60%

Washington, D.C.

Orange County

Los Angeles

Manhattan

Chicago CBD

San Francisco

South Florida

Tampa Bay

Dallas/Fort Worth

National Total

Houston

Suburban Philadelphia

Suburban Maryland

San Diego

New Jersey

Virginia

Silicon Valley

Denver

Atlanta

Philadelphia

(%)

Leasing in Last 12 Months -

Y-o-Y Change

115.9%

113.5%

113.4%

113.3%

109.8%

107.6%

106.9%

106.3%

100.3%

98.6%

98.1%

90.8%

83.6%

80.0%

79.3%

78.2%

77.9%

74.4%

74.3%

72.8%

0% 30% 60% 90% 120% 150%

Washington, D.C.

San Francisco

Los Angeles

Dallas/Fort Worth

Manhattan

Houston

South Florida

Tampa Bay

Orange County

Chicago CBD

National Total

Philadelphia

Northern Virginia

Atlanta

Denver

San Diego

Suburban Philadelphia

New Jersey

Suburban Maryland

Silicon Valley

Leasing in Last 12 Months as % of

Market's Five-Year Leasing Average

(%)

4. NATIONAL MARKETS AT A GLANCE

Corporate Lic. # 00388260savills-studley.com

Construction Pipeline*

89.2%

84.5%

75.8%

74.0%

73.1%

69.9%

67.1%

65.7%

64.4%

60.3%

59.7%

55.7%

49.6%

40.5%

39.9%

38.5%

29.5%

0% 20% 40% 60% 80% 100%

Silicon Valley

New Jersey

Philadelphia Region

Chicago

Atlanta

Boston

San Francisco

Dallas/Fort Worth

Houston

Phoenix

Raleigh/Durham

Manhattan

Washington, D.C.

Seattle

Denver

San Diego

Los Angeles

(%)

Pre-Leased Rate

6.0%

5.8%

5.9%

5.3%

5.1%

5.6%

6.3%

5.8%

6.0%

6.3%

7.0%

6.9%

6.7%

6.3%

8.7%

7.2%

7.5%

7.3%

7.1%

9.2%

3.8%

4.6%

4.6%

4.6%

4.6%

4.6%

4.9%

4.9%

4.9%

5.1%

5.4%

5.6%

5.6%

5.7%

6.1%

6.2%

6.4%

6.7%

6.7%

7.9%

0% 3% 5% 8% 10%

Denver

Houston

Dallas/Fort Worth

Seattle

Washington, D.C.

Raleigh

Boston

Orange County

San Francisco

Silicon Valley

Philadelphia

San Diego

U.S.

Tampa Bay

Chicago

New Jersey

Manhattan City

Miami

Atlanta

Los Angeles

(%)

Unemployment Rate

Year-End

2013

Year-End

2014

4.7%

5.3%

2.2%

4.6%

0.5%

1.8%

4.3%

4.3%

3.0%

2.9%

2.4%

1.7%

2.2%

2.8%

1.6%

0.6%

3.4%

0.3%

1.9%

-0.1%

-0.6%

7.6%

7.5%

6.1%

5.7%

5.1%

4.1%

4.1%

3.5%

3.2%

3.2%

3.0%

2.6%

2.5%

2.3%

2.3%

2.3%

2.1%

1.5%

1.3%

1.1%

0.3%

-2% -1% 0% 1% 2% 3% 4% 5% 6% 7% 8%

Silicon Valley

Raleigh/Durham

Dallas/Fort Worth

San Francisco

San Diego

Houston

Phoenix

South Florida

Atlanta

Seattle

U.S.

Los Angeles

Boston

Denver

Manhattan

Orange County

Tampa Bay

Philadelphia

Chicago

New Jersey

Washington, D.C.

Change in Office-Using Employment (December 2014 - December 2013)

2013 2014

(%)

17.9

7.8

7.6

6.9

6.1

6.1

6.0

5.8

5.6

3.0

2.9

2.9

2.7

2.0

1.9

1.1

0.0 3.0 6.0 9.0 12.0 15.0 18.0

Houston

Dallas/Fort Worth

Silicon Valley

Washington, D.C.

Manhattan

Chicago

Seattle

Boston

San Francisco

Philadelphia Region

Denver

Phoenix

Los Angeles

Raleigh/Durham

Atlanta

New Jersey

(MSF)

Under Construction

*Source: CoStar. Includes all actively marketed properties that have commenced work on building foundation

Employment Data*

*Source: Bureau Labor Statistics

5. NATIONAL MARKETS AT A GLANCE

Corporate Lic. # 00388260savills-studley.com

Projected Annual Growth Rates (2011-2015)*

6.9%

6.8%

6.7%

4.6%

4.5%

4.4%

4.3%

3.8%

3.3%

3.0%

3.0%

2.9%

2.6%

2.5%

2.1%

1.9%

1.1%

0% 2% 4% 6% 8%

Chicago

Tampa Bay

Atlanta

San Francisco

Silicon Valley

San Diego

Philadelphia

Average

Miami

New Jersey

Los Angeles

Houston

Manhattan

Orange County

Dallas

Denver

Washington DC

Existing Home Prices

(%)

3.1%

3.1%

2.8%

2.6%

2.6%

2.5%

2.5%

2.3%

2.3%

2.2%

2.2%

2.0%

1.9%

1.9%

1.7%

1.6%

1.5%

0.0% 1.0% 2.0% 3.0% 4.0%

Houston

Dallas

San Francisco

Silicon Valley

Atlanta

San Diego

Orange County

Los Angeles

Average

Denver

Manhattan

Philadelphia

Tampa Bay

New Jersey

Chicago

Washington DC

Miami

Overall Employment

(%)

5.1%

5.1%

5.1%

5.0%

4.3%

4.2%

4.2%

4.1%

4.0%

3.9%

3.9%

3.4%

3.1%

3.0%

2.9%

2.7%

2.5%

0% 1% 2% 3% 4% 5% 6%

San Francisco

Dallas

Houston

Silicon Valley

Atlanta

Manhattan

Los Angeles

Denver

San Diego

Average

Orange County

Chicago

New Jersey

Washington DC

Tampa Bay

Miami

Philadelphia

Metro Gross City Product

(%)

2.1%

2.0%

1.7%

1.5%

1.3%

1.2%

1.2%

1.1%

1.0%

1.0%

1.0%

0.8%

0.8%

0.5%

0.4%

0.3%

0.2%

0.0% 0.5% 1.0% 1.5% 2.0% 2.5%

Dallas

Houston

Atlanta

San Diego

Tampa Bay

Washington DC

Denver

Average

Orange County

Miami

Los Angeles

Silicon Valley

San Francisco

Chicago

New Jersey

Philadelphia

Manhattan

Population

(%)

*Source: Moody’s Economy.com Data

Projected Annual Growth Rates (2011-2015)*