Downloaded 18 times

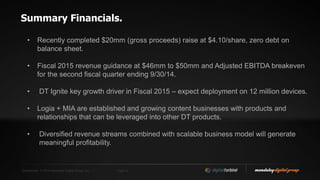

This document provides an overview of Mandalay Digital Group, Inc. and its end-to-end mobile content solution for carriers and OEMs. It discusses Mandalay's history of strategic acquisitions to build its business, its products including Ignite, IQ, and content management, and its customers which provide access to over 1 billion subscribers globally. Financial information is also presented on Mandalay's market capitalization and revenue guidance of $46-50 million for FY2015, representing 80-100% growth over the prior year.