a. Identify anddescribe the

elements of SCI for a

Service Business and

merchandising

b. Prepare an SCI for a

service business using

single step approach

OBJECTIV

ES

3.

LESSON 1

IDENTIFY ANDDESCRIBE THE

ELEMENTS OF SCI FOR A SERVICE

AND MERCHANDISING BUSINESS

AND PREPARATION USING

SINGLE

STEP APPROACH FOR SERVICE

BUSINESS

5.

STATEMENT OF COMPREHENSIVE

INCOME(INCOME STATEMENT)

The Statement of Comprehensive Income informs

the reader about the “performance” and activities

of the company for a certain period (e.g., for the

period ended December 31, 2019). It contains the

revenues and expenses incurred by an entity for a

specific period. It is also compared to a running

video because it presents an entity’s activities form

the start to the end of a period.

6.

STATEMENT OF COMPREHENSIVE

INCOME(INCOME STATEMENT)

Another meaning is it “contains the results

of the company’s operations for a specific

period of time which is called net income if

it is a net positive result while a net loss if it

is a net negative result. This can be

prepared for a month, a quarter or a year”.

(Haddock, Price, & Farina, 2012)

7.

TEMPORARY ACCOUNTS

Temporary accountsare also known as nominal

accounts are the accounts found under the SCI.

They are called such because at the end of the

accounting period balances under these accounts

are transferred to the capital account, thus having

only temporary amounts and resulting to zero

beginning balances at the beginning of the

following year. (Haddock, Price, & Farina, 2012)

8.

TEMPORARY ACCOUNTS

Examples oftemporary accounts

include revenues, sales, utilities

expense, supplies, expense, salaries

expense, depreciation expense,

interest expense among others.

9.

ELEMENTS OF THESCI

1. The Title

The Statement of Comprehensive Income is

a financial report therefore it must be

properly identified and dated. The title or

the heading includes the name of the

entity, the title of the report (i.e.,

Statement of Comprehensive Income and

the period it covers.

10.

ELEMENTS OF THESCI

2. Revenue

“Revenues arise in the course of the

ordinary activities of an entity and is

referred to by a variety of different

names including sales, fees, interest,

dividend, royalties, rent”. (The Conceptual

Framework for Financial Reporting by the

International Accounting Board 2010)

11.

ELEMENTS OF THESCI

2. Revenue

Revenues are the first line item in the Statement of

Comprehensive Income. They vary depending to the

nature of the entity. A small retail store has sales as its

main revenue. Revenues may also come from interest

from time deposits and dividends earned from shares

of stocks. Royalties from individuals who would like to

use their established brand and technology. Owners of

fixed properties (e.g. land and building) may charge

third parties with rent.

12.

ELEMENTS OF THESCI

2. Revenue

Entities engage in service business use service income

as revenue account.

Smaller and less complex entities may have one or two

sources of revenues while larger and more complex

entities have multiple sources of revenues, recorded

when

earned.

13.

ELEMENTS OF THESCI

3. Expenses

“Expenses arise in the course of the ordinary

activities of the entity include, for example, cost

of sales, wages, and depreciation. They usually

take the form of an outflow or depletion of asset

such as cash and cash equivalent, inventory,

property, plant, and equipment.” (The Conceptual

Framework for Financial Reporting by the

International Accounting Board 2010)

14.

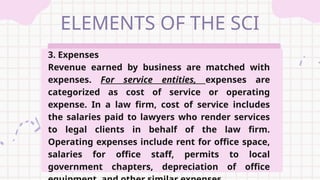

ELEMENTS OF THESCI

3. Expenses

Revenue earned by business are matched with

expenses. For service entities, expenses are

categorized as cost of service or operating

expense. In a law firm, cost of service includes

the salaries paid to lawyers who render services

to legal clients in behalf of the law firm.

Operating expenses include rent for office space,

salaries for office staff, permits to local

government chapters, depreciation of office

15.

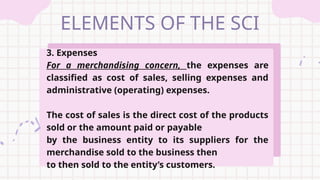

ELEMENTS OF THESCI

3. Expenses

For a merchandising concern, the expenses are

classified as cost of sales, selling expenses and

administrative (operating) expenses.

The cost of sales is the direct cost of the products

sold or the amount paid or payable

by the business entity to its suppliers for the

merchandise sold to the business then

to then sold to the entity’s customers.

16.

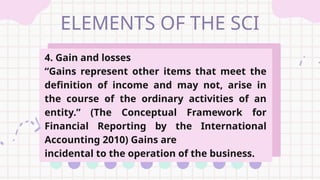

ELEMENTS OF THESCI

4. Gain and losses

“Gains represent other items that meet the

definition of income and may not, arise in

the course of the ordinary activities of an

entity.” (The Conceptual Framework for

Financial Reporting by the International

Accounting 2010) Gains are

incidental to the operation of the business.

17.

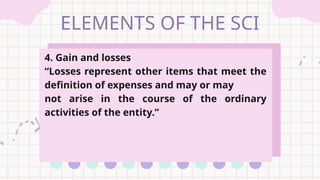

ELEMENTS OF THESCI

4. Gain and losses

“Losses represent other items that meet the

definition of expenses and may or may

not arise in the course of the ordinary

activities of the entity.”

18.

ELEMENTS OF THESCI

5. Other Items

Other items included in the computation of

the total comprehensive income are income

taxes and items of other comprehensive

income.

Income tax is the sum of money payable to

the government. Items of other

comprehensive income are increases or

decreases in economic benefit for a period.

19.

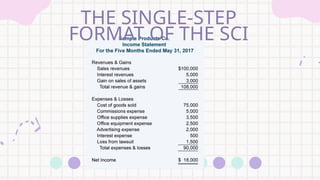

THE TWO TYPESOF

STATEMENT OF

COMPREHENSIVE

INCOME:

1. The Single-step Format of the SCI

It is called single-step because all revenues

are listed down in one section while all

expenses are listed in another. Net income is

computed using a “single-step” which is Total

Revenues minus Total Expenses. (Haddock,

Price, & Farina, 2012). This

format of SCI is more commonly used by

service companies.

THE TWO TYPESOF

STATEMENT OF

COMPREHENSIVE

INCOME:

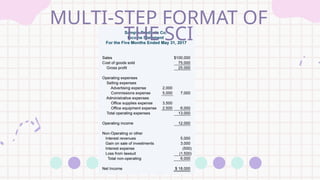

2. Multi-step format of the SCI

It is called multi-step because there are

several steps needed in order to arrive at the

company’s net income. (Haddock, Price, &

Farina, 2012) This format is more

commonly used by merchandising

companies

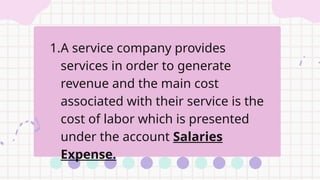

1.A service companyprovides

services in order to generate

revenue and the main cost

associated with their service is the

cost of labor which is presented

under the account Salaries

Expense.

25.

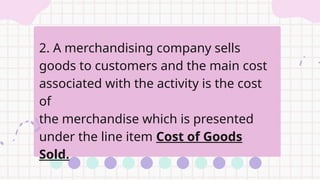

2. A merchandisingcompany sells

goods to customers and the main cost

associated with the activity is the cost

of

the merchandise which is presented

under the line item Cost of Goods

Sold.

26.

PREPARATION OF THESTATEMENT

OF COMPREHENSIVE INCOME

USING THE

SIGNLE-STEP APPROACH

27.

ABC COMPANY STATEMENTOF COMPREHENSIVE

INCOME FOR THE MONTH OF JUNE 2023

Cost of Goods Sold: ₱300,000

Sales: ₱500,000

Salaries: ₱50,000

Rent Expense: ₱20,000

Interest Income: ₱10,000

Utilities: ₱10,000

28.

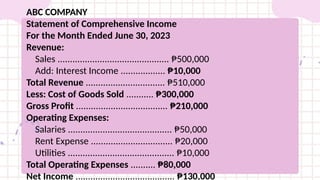

ABC COMPANY

Statement ofComprehensive Income

For the Month Ended June 30, 2023

Revenue:

Sales ............................................. ₱500,000

Add: Interest Income .................. ₱10,000

Total Revenue ................................ ₱510,000

Less: Cost of Goods Sold ........... ₱300,000

Gross Profit ..................................... ₱210,000

Operating Expenses:

Salaries .......................................... ₱50,000

Rent Expense ................................. ₱20,000

Utilities ........................................... ₱10,000

Total Operating Expenses .......... ₱80,000

Net Income ........................................ ₱130,000

29.

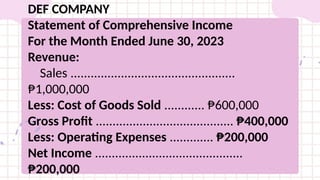

DEF COMPANY STATEMENTOF

COMPREHENSIVE INCOME FOR THE

MONTH OF JUNE 2023

Cost of Goods Sold: ₱600,000

Sales: ₱1,000,000

OPERATING expenses: 200,000

30.

DEF COMPANY

Statement ofComprehensive Income

For the Month Ended June 30, 2023

Revenue:

Sales .................................................

₱1,000,000

Less: Cost of Goods Sold ............ ₱600,000

Gross Profit ......................................... ₱400,000

Less: Operating Expenses ............. ₱200,000

Net Income ............................................

₱200,000

31.

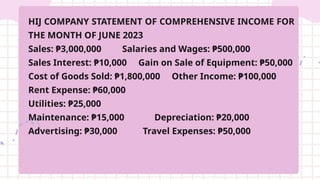

HIJ COMPANY STATEMENTOF COMPREHENSIVE INCOME FOR

THE MONTH OF JUNE 2023

Sales: ₱3,000,000 Salaries and Wages: ₱500,000

Sales Interest: ₱10,000 Gain on Sale of Equipment: ₱50,000

Cost of Goods Sold: ₱1,800,000 Other Income: ₱100,000

Rent Expense: ₱60,000

Utilities: ₱25,000

Maintenance: ₱15,000 Depreciation: ₱20,000

Advertising: ₱30,000 Travel Expenses: ₱50,000

32.

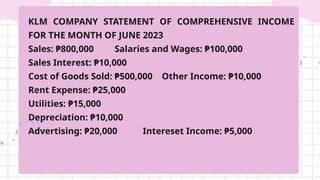

KLM COMPANY STATEMENTOF COMPREHENSIVE INCOME

FOR THE MONTH OF JUNE 2023

Sales: ₱800,000 Salaries and Wages: ₱100,000

Sales Interest: ₱10,000

Cost of Goods Sold: ₱500,000 Other Income: ₱10,000

Rent Expense: ₱25,000

Utilities: ₱15,000

Depreciation: ₱10,000

Advertising: ₱20,000 Intereset Income: ₱5,000

33.

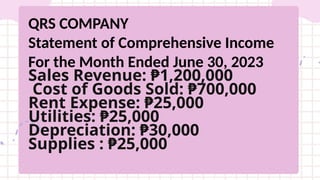

QRS COMPANY

Statement ofComprehensive Income

For the Month Ended June 30, 2023

Sales Revenue: ₱1,200,000

Cost of Goods Sold: ₱700,000

Rent Expense: ₱25,000

Utilities: ₱25,000

Depreciation: ₱30,000

Supplies : ₱25,000

34.

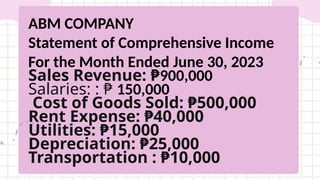

ABM COMPANY

Statement ofComprehensive Income

For the Month Ended June 30, 2023

Sales Revenue: ₱900,000

Salaries: : ₱ 150,000

Cost of Goods Sold: ₱500,000

Rent Expense: ₱40,000

Utilities: ₱15,000

Depreciation: ₱25,000

Transportation : ₱10,000

35.

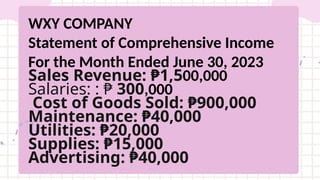

WXY COMPANY

Statement ofComprehensive Income

For the Month Ended June 30, 2023

Sales Revenue: ₱1,500,000

Salaries: : ₱ 300,000

Cost of Goods Sold: ₱900,000

Maintenance: ₱40,000

Utilities: ₱20,000

Supplies: ₱15,000

Advertising: ₱40,000

36.

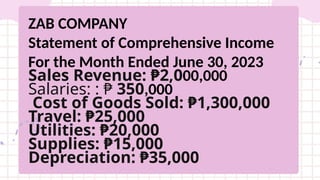

ZAB COMPANY

Statement ofComprehensive Income

For the Month Ended June 30, 2023

Sales Revenue: ₱2,000,000

Salaries: : ₱ 350,000

Cost of Goods Sold: ₱1,300,000

Travel: ₱25,000

Utilities: ₱20,000

Supplies: ₱15,000

Depreciation: ₱35,000

#5 Ang Statement of Comprehensive Income ay isang financial statement na nagpapakita ng kabuuang kita (total income) ng isang negosyo sa loob ng isang partikular na panahon (halimbawa: isang taon).

Mga Nilalaman ng Statement of Comprehensive Income:

Revenue (Kita)

➤ Halimbawa: Sales, Service Income

Less: Expenses (Gastos)

➤ Halimbawa: Rent, Salaries, Utilities

Net Income / Net Loss (Kita o Pagkalugi)

➤ Kita kung mas mataas ang revenue kaysa gastos

➤ Pagkalugi kung mas mataas ang gastos kaysa kita

Other Comprehensive Income

➤ Halimbawa: Revaluation gain, Unrealized gain/loss sa investments

Total Comprehensive Income

➤ Net Income + Other Comprehensive Income

#7 Ang Temporary Accounts, na kilala rin bilang Nominal Accounts, ay mga account na matatagpuan sa Statement of Comprehensive Income (SCI) o Pahayag ng Kabuuang Kita.

Kasama rito ang mga sumusunod:

Kita (Revenue)

Gastos (Expenses)

Mga kita mula sa ibang pinagkukunan (Gains)

Pagkalugi (Losses)

📝 Bakit tinatawag na "Temporary"?

Tinatawag silang temporary o pansamantala dahil:

Sa katapusan ng accounting period (hal. taon), ang balanse ng mga account na ito ay isinasara o inililipat sa capital account (hal. Owner’s Equity).

Dahil dito, ang mga account na ito ay nagsisimula sa zero (0) sa simula ng susunod na taon.

➡️ Ibig sabihin, pang-isang panahon lang ang laman ng mga account na ito. Hindi ito dinadala sa susunod na taon

#10 Ang revenue o kita ay nagmumula sa normal o karaniwang operasyon ng isang negosyo. Ibig sabihin, ito ang pera o halaga na kinikita sa pang-araw-araw na gawain ng kumpanya.

Ang tawag sa revenue ay maaaring iba-iba depende sa uri ng negosyo o transaksyon. Narito ang ilang halimbawa:

Sales – kung ikaw ay nagbebenta ng produkto (hal. grocery store, clothing business)

Fees – kung ikaw ay nagbibigay ng serbisyo at may bayad (hal. tuition fees, service fees)

Interest – kita mula sa bangko o pautang

Dividends – kita mula sa investment sa shares of stock

Royalties – bayad sa paggamit ng iyong brand, libro, o teknolohiya

Rent – kita mula sa pagpapaupa ng lupa, bahay, o gusali

💡 Summary:

Revenue is any income earned during the normal course of business—whether through selling, renting, investing, or providing services.

#11 English:

Revenues are the first line item in the Statement of Comprehensive Income. They vary depending on the nature of the entity. A small retail store has sales as its main revenue. Revenues may also come from interest from time deposits and dividends earned from shares of stocks. Royalties from individuals who would like to use their established brand and technology. Owners of fixed properties (e.g. land and building) may charge third parties with rent.

Taglish Version:

Revenue (o Kita sa Filipino) ay ang pera o halagang kinikita ng isang negosyo mula sa mga aktibidad nito. Ito ang unang bahagi ng Statement of Comprehensive Income dahil ito ang pinagmumulan ng income bago ibawas ang mga gastos.

📌 Paliwanag:

Depende ito sa nature ng negosyo.

Iba-iba ang source ng revenue depende sa uri ng entity.

Halimbawa:

Kung ikaw ay may sari-sari store, ang revenue mo ay galing sa benta ng paninda.

Iba pang pinagkukunan ng revenue:

Interest: Kapag may pera kang naka-time deposit sa bangko, kikita ito ng interest.

Dividends: Kung may investment ka sa stocks (shares ng company), pwede kang kumita ng dividend.

Royalties: Kapag may tao o kumpanya na gustong gamitin ang brand o technology mo, babayaran ka nila ng royalties.

Rent: Kung may ari-arian ka tulad ng lupa o building, pwede mong paupahan at kikita ka mula sa renta.

#12 Service Businesses (negosyong nagbibigay ng serbisyo) tulad ng salon, repair shop, o tutorial center ay gumagamit ng Service Income bilang kanilang revenue account.

👉 Halimbawa: Kapag ang isang tutor ay binayaran para sa session, ito ay itinatala bilang Service Income.

✔️ Maliliit at simpleng negosyo ay kadalasang may isa o dalawang pinagkukunan ng kita lang.

👉 Halimbawa: Isang sari-sari store na ang kita ay galing lang sa paninda.

✔️ Samantalang ang malalaki at mas komplikadong negosyo ay may maraming sources of revenue tulad ng:

Sales

Rental income

Dividends

Royalties

Service income

📌 Ang lahat ng revenue ay nire-record lamang kapag ito ay earned o nakuha na ng negosyo ang karapatang bayaran.

✅ Summary:

Ang Service Income ay karaniwang revenue ng mga service-based businesses.

Maliliit na negosyo = kaunting sources of revenue

Malalaking negosyo = maraming pinagkukunan ng kita

Lahat ng revenue ay kinikilala kapag earned na ito.

#13 Ang Expenses (Gastos) ay ang mga bayarin o pagkawala ng yaman ng negosyo na nangyayari habang isinasagawa ang mga normal na operasyon nito.

📌 Halimbawa ng mga karaniwang gastos:

Cost of Sales – halaga ng produkto na ibinenta

Wages – sweldo ng mga empleyado

Depreciation – unti-unting pagbawas ng halaga ng mga ari-ariang gamit ng negosyo tulad ng sasakyan, makina, o computer

👉 Karaniwan, ang gastos ay lumalabas bilang:

Paglabas ng pera (cash outflow), tulad ng pagbabayad ng bills

Pagbawas ng assets, gaya ng:

Cash at cash equivalents

Inventory (mga paninda)

Property, Plant, and Equipment (mga gamit ng negosyo)

✅ Summary:

Ang expenses ay bahagi ng normal na operasyon ng negosyo. Ito ang mga bayarin o pagkawala ng yaman (cash o asset) na ginagamit para makapag-operate ang negosyo.

#14 Sa accounting, kailangan i-match o itapat ang kinita ng negosyo (revenue) sa gastos (expenses) para makita kung talagang kumita o nalugi ang negosyo sa isang accounting period. Ito ang tinatawag na "matching principle."

✅ Sa mga Service Business tulad ng law firm, clinic, o salon, may dalawang klase ng gastos:

1. Cost of Service

Ito ang gastos na direktang may kinalaman sa mismong serbisyo na ibinibigay sa kliyente.

📌 Halimbawa:

Sa law firm, ito ang sweldo ng mga abogado na nagbibigay ng legal advice sa mga kliyente.

Sa salon, ito ang bayad sa hairstylist o hair products na ginamit.

Bakit kasama ito sa cost of service?

Kasi ito ang gastos para maibigay mismo ang serbisyo.

2. Operating Expenses

Ito naman ang mga indirect na gastos — hindi direkta sa serbisyo, pero kailangan para tumakbo ang negosyo.

📌 Halimbawa sa law firm:

Upa sa opisina

Sweldo ng secretary o admin staff

Bayad sa business permits

Depreciation o pagkaluma ng office equipment (printer, computer, etc.)

Bakit operating expense?

Kasi hindi ito para sa mismong serbisyo, pero mahalaga para sa daily operations.

#15 Sa isang merchandising business (negosyong bumibili at nagbebenta ng produkto, tulad ng tindahan o grocery), ang mga gastos (expenses) ay hinahati sa tatlong klase:

✅ 1. Cost of Sales (Halaga ng Nabentang Paninda)

Ito ang direct cost o direktang gastos sa mga produkto na ibinenta sa mga customer.

📌 Ibig sabihin:

Ito ang halaga na binayad ng negosyo sa supplier para sa mga panindang ibinenta.

Halimbawa, kung bumili ang tindahan ng sabon sa halagang ₱50 bawat isa at ibinenta ito ng ₱70, ang ₱50 ay cost of sales.

📌 Formula (simplified):

✅ 2. Selling Expenses

Ito ang mga gastos na may kinalaman sa pagbebenta ng produkto.

📌 Halimbawa:

Suweldo ng sales staff

Advertising at promotion

Delivery expenses

Commission sa sales agents

✅ 3. Administrative or Operating Expenses

Ito ang mga general expenses ng negosyo na hindi directly related sa sales pero kailangan sa operation.

📌 Halimbawa:

Upa ng opisina

Suweldo ng admin staff o manager

Utilities (kuryente, tubig)

Office supplies

Depreciation ng equipment

#16 Ang gains ay mga karagdagang kita na pasok sa definition ng income, pero hindi galing sa regular o pangkaraniwang gawain ng negosyo.

📌 Ibig sabihin:

Ang gains ay hindi nangyayari araw-araw tulad ng regular na kita (sales or service income).

Sila ay “extra income” na hindi bahagi ng pangunahing operasyon ng negosyo.

🔍 Halimbawa ng Gains:

Kita mula sa pagbenta ng lumang equipment na mas mataas sa book value

Foreign exchange gain – kapag kumita ang negosyo sa pagbabago ng halaga ng currency

Gain on investment – kapag tumaas ang halaga ng shares of stock na pag-aari ng negosyo at ibinenta ito

✅ Summary:

Gains = Extra o di-inaasahang kita

✔️ Hindi galing sa normal na sales o service

✔️ Nangyayari minsan lang o incidental

✔️ Kasama pa rin sa income, pero hiwalay sa regular revenue

#17 Ang losses (pagkalugi) ay mga bagay na pasok sa kahulugan ng expenses (gastos), pero hindi palaging nangyayari sa regular na operasyon ng negosyo.

📌 Ibig sabihin:

Ang losses ay karagdagang gastos o bawas sa yaman ng negosyo, pero hindi katulad ng normal na expenses tulad ng suweldo, renta, o kuryente.

Maaaring:

Parte ng normal na operasyon (hal. spoiled goods sa grocery)

O hindi normal o aksidente lang (hal. sunog, baha, o pagkasira ng asset)

🔍 Mga Halimbawa ng Losses:

Loss from fire or theft – nasunog o nanakaw ang inventory

Foreign exchange loss – pagkalugi dahil sa pagbaba ng value ng currency

Loss on sale of equipment – kung ibinenta ang gamit ng negosyo ng mas mababa sa book value

Obsolete inventory – panindang hindi na mabenta dahil paso na o lipas na sa uso

✅ Summary:

Losses = Hindi inaasahang gastusin o bawas sa yaman ng negosyo.

✔️ Maaaring normal o hindi normal

✔️ Kasama sa financial reporting para ipakita ang totoong financial performance ng negosyo

#18 Other items included in the computation of the Total Comprehensive Income are:

Income Tax

Items of Other Comprehensive Income

💬 Taglish Explanation:

Bukod sa Revenue (Kita) at Expenses (Gastos), may iba pang items na isinasaalang-alang sa pagkuwenta ng kabuuang kita ng negosyo o Total Comprehensive Income:

✅ 1. Income Tax (Buwis)

Ito ay ang halagang ibinabayad sa gobyerno batay sa kinita ng negosyo.

Isa ito sa pinakamalaking obligasyon ng isang negosyo tuwing katapusan ng taon.

📌 Halimbawa: Kung ang negosyo ay kumita ng ₱100,000, at ang tax rate ay 30%, kailangang magbayad ng ₱30,000 na income tax.

✅ 2. Other Comprehensive Income

Ito ay mga pagtaas o pagbaba sa economic benefit ng negosyo sa loob ng isang panahon, na hindi bahagi ng regular na operasyon.

Hindi ito pumapasok sa net income pero isinusulat pa rin sa Statement of Comprehensive Income.

📌 Halimbawa ng Other Comprehensive Income:

Revaluation surplus – pagtaas ng halaga ng property

Unrealized gains/losses on investments

Foreign currency translation adjustments

✅ Summary:

Ang Other Items sa Statement of Comprehensive Income ay binubuo ng:

🔸 Income Tax – bayad sa gobyerno

🔸 Other Comprehensive Income – dagdag/kaltas na kita na hindi galing sa pang-araw-araw na operasyon, pero mahalagang ipakita sa financial report

#19 Ang Single-Step Format ay isang uri ng Statement of Comprehensive Income na simple at diretso ang pagkakagawa.

📌 Bakit tinawag na Single-Step?

✔️ Tinawag itong single-step dahil:

Lahat ng Revenue (kita) ay inilalagay sa isang bahagi

Lahat ng Expenses (gastos) ay inilalagay sa kabilang bahagi

Pagkatapos, ang Net Income (Kita) ay kinukuwenta sa isang simpleng hakbang lang:

🧮 Net Income = Total Revenues – Total Expenses

📌 Saan ito kadalasang ginagamit?

✅ Ang format na ito ay karaniwang ginagamit ng service businesses tulad ng:

Law firm

Accounting office

Clinics

Tutorial centers

Salon

Summary:

The Single-Step SCI is a simple way to compute net income:

Total Kita – Total Gastos = Kita ng Negosyo

#21 ng Multi-Step Format ay isang paraan ng paggawa ng Statement of Comprehensive Income kung saan may iba’t ibang hakbang o section bago makuha ang Net Income.

📌 Bakit tinawag na Multi-Step?

✔️ Tinatawag itong multi-step dahil:

Hindi lang isang simpleng “Revenue – Expenses = Net Income”

May maraming bahagi tulad ng:

Gross Profit

Operating Income

Other Income and Expenses

Income Before Tax

Net Income

🛒 Kanino karaniwang ginagamit?

✅ Madalas itong ginagamit ng merchandising companies, o mga negosyong bumibili at nagbebenta ng produkto, tulad ng:

Grocery

Department store

Convenience store

Online shops

📎 Summary:

The Multi-Step SCI is more detailed and shows different levels of profit (gross, operating, and net).

📌 Commonly used by merchandising businesses.

#24 Ang service company ay isang negosyo na nagbibigay ng serbisyo kapalit ng bayad, at doon sila kumikita o nakakakuha ng revenue (kita).

📌 Halimbawa ng service business:

Salon

Law firm

Tutorial center

Accounting firm

Sa mga ganitong negosyo, walang produkto na binebenta — serbisyo ang produkto nila.

🔍 Ano ang pangunahing gastos ng service business?

Ang pinakamalaking gastos ng service company ay ang pasahod o labor cost, dahil tao (empleyado) ang nagbibigay ng serbisyo.

👉 Ito ay nakatala sa accounting bilang:

Salaries Expense

📌 Halimbawa:

Kung ang isang law firm ay may mga abogado na binabayaran ng ₱30,000 kada buwan, ang halaga ng suweldo nila ay itatala sa accounting books bilang Salaries Expense.

✅ Summary:

Sa mga service company, ang pangunahing kita ay galing sa serbisyo, at ang pangunahing gastos ay ang suweldo ng empleyado, na tinatawag na Salaries Expense sa accounting.

#25 Ang merchandising company ay isang uri ng negosyo na bumibili ng produkto at pagkatapos ay ibinebenta ito sa mga customer para kumita.

📌 Halimbawa ng merchandising business:

Grocery store

Department store

Sari-sari store

Online shop (na nagre-resell ng items)

🔍 Ano ang pangunahing gastos ng merchandising business?

Ang pinakamalaking gastos nila ay ang halaga ng mga panindang ibinenta.

Sa accounting, ito ay tinatawag na:

Cost of Goods Sold (COGS)

o sa Tagalog: Halaga ng Nabentang Paninda

📌 Ibig sabihin ng COGS:

Ito ang presyo ng produkto noong binili ito ng negosyo mula sa supplier — hindi ang presyo na ipinagbenta sa customer.

✅ Halimbawa:

Bumili si Ana ng t-shirt sa halagang ₱100 bawat isa.

Ibinenta niya ito sa halagang ₱150.

➡️ Ang ₱100 ay tatawaging Cost of Goods Sold

➡️ Ang ₱50 na sobra ay bahagi ng gross profit

📎 Summary:

Sa merchandising business, ang pangunahing kita ay galing sa benta ng produkto,

at ang pangunahing gastos ay ang halaga ng panindang binili — tinatawag na Cost of Goods Sold.