Downloaded 34 times

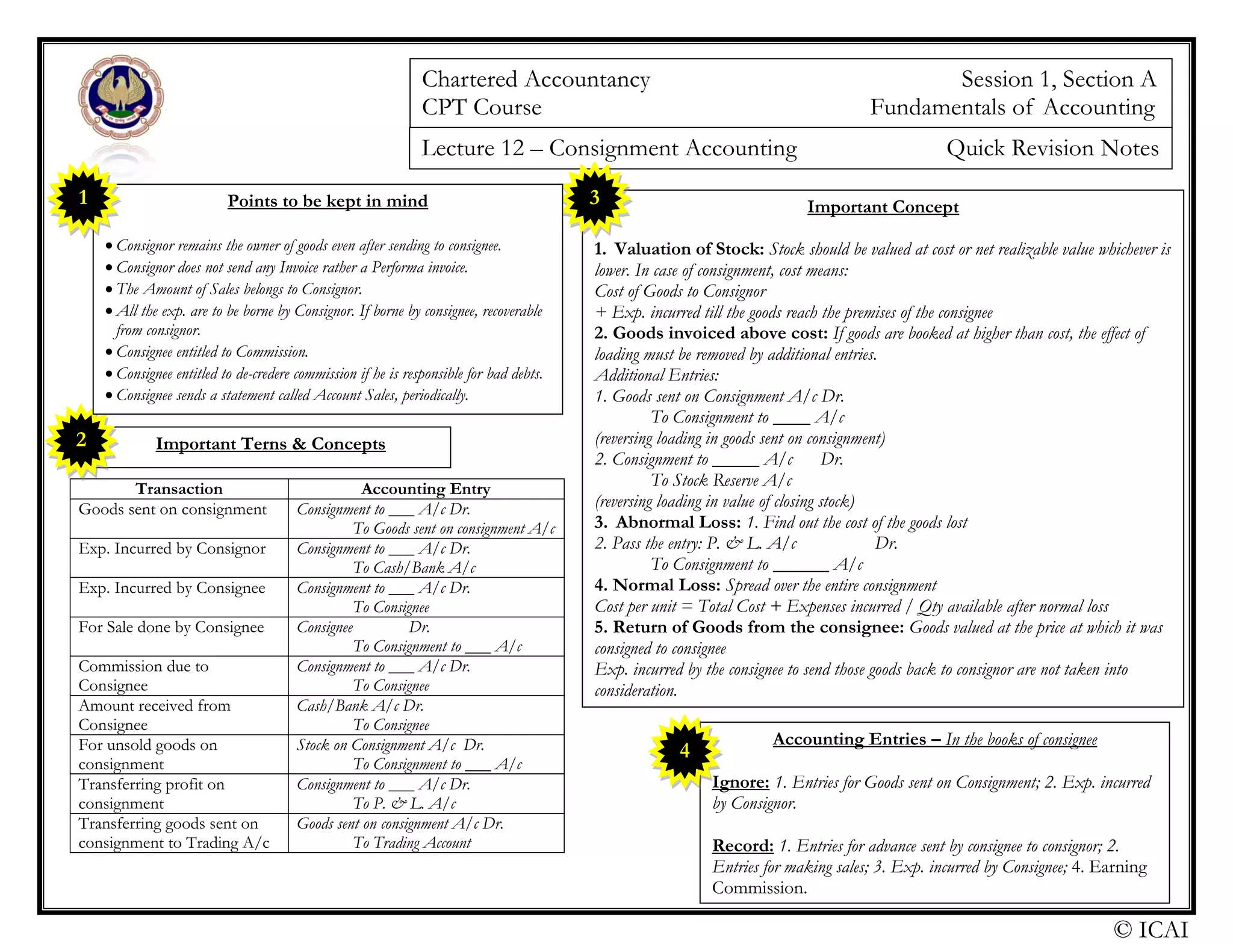

This document provides a quick revision of key concepts in consignment accounting. It outlines that in a consignment, the consignor remains the owner of goods sent to the consignee. The consignee sells the goods on behalf of the consignor and is entitled to commission. Important accounts include goods sent on consignment, consignment to (consignee name), and stock on consignment. Key accounting entries are described for transactions such as goods sent on consignment, sales made by the consignee, expenses incurred by both parties, and transferring the unsold goods or profit back to the consignor.