Recommended

Recommended

More Related Content

Similar to Lec 3 Debit Credit Rules General Journal.pptx

Similar to Lec 3 Debit Credit Rules General Journal.pptx (20)

More from pal83111

More from pal83111 (16)

Recently uploaded

Recently uploaded (20)

Lec 3 Debit Credit Rules General Journal.pptx

- 1. Lec 3 BASIC FINANCIAL STATEMENTS Debit Credit Rules General Journal Lec 3: Financial Accouting 1

- 2. Introduction to Financial Statements Lec 3: Financial Accouting 2 Companies prepare interim financial statements and annual financial statements. 2000 X

- 3. What are financial statements? • Financial statements refer to the record of a business’s finances that are recorded over a period of time. • They contain essential financial information such as details of assets, liabilities, income, expenses, etc. • Financial statements, in essence, are a formal, historical record of the business’ finances that business owners and finance executives can use to evaluate business health and performance. • Financial data is presented in four fundamental sets collectively known as financial statements for evaluation. • This can help you organize and categorize your financial statements to make data-driven decisions to drive financial growth. Lec 3: Financial Accouting 3

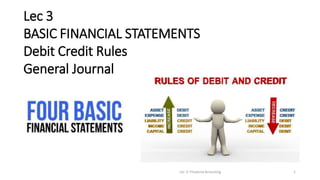

- 4. What are financial statements? • 4 Basic Financial Statements 1. The balance sheet or statement of the financial position 2. The profit & loss account or an income statement 3. The cash flow statement or formerly the flow of funds statement 4. The statement of retained earnings or the statement of changes in comprehensive income Lec 3: Financial Accouting 4

- 5. 1. Balance sheet – provides a snapshot of a firm’s financial position at one point in time. 2. Income statement – summarizes a firm’s revenues and expenses over a given period of time. 3. Statement of retained earnings – shows how much of the firm’s earnings were retained, rather than paid out as dividends. 4. Statement of cash flows – reports the impact of a firm’s activities on cash flows over a given period of time. The Annual Report Lec 3: Financial Accouting 5

- 6. Introduction to Financial Statements Lec 3: Financial Accouting 6 Describes where the enterprise stands at a specific date. Income Statement Balance Sheet Statement of Cash Flows

- 7. Introduction to Financial Statements Lec 3: Financial Accouting 7 Depicts the revenue and expenses for a designated period of time. Income Statement Balance Sheet Statement of Cash Flows

- 8. Introduction to Financial Statements Lec 3: Financial Accouting 8 Revenues result in positive cash flow. Expenses result in negative cash flow. Either in the past, present, or future.

- 9. Introduction to Financial Statements Lec 3: Financial Accouting 9 Net income (or net loss) is simply the difference between revenues and expenses. Income Statement Balance Sheet Statement of Cash Flows

- 10. Introduction to Financial Statements Lec 3: Financial Accouting 10 Depicts the ways cash has changed during a designated period of time. Balance Sheet Income Statement Statement of Cash Flows

- 11. Vagabond Travel Agency Balance Sheet December 31, 2002 Assets Cash Notes receivable Accounts receivable Supplies $ 22,500 10,000 60,500 2,000 Liabilities & Owners' Equity Liabilities: Notes payable $ 41,000 Accounts payable 36,000 Salaries payable 3,000 Land 100,000 Total liabilities $ 80,000 Building 90,000 Owners' Equity: Office equipment 15,000 Capital stock 150,000 Retained earnings 70,000 Total $300,000 Total $300,000 A Starting Point: Statement of Financial Position Lec 3: Financial Accouting 11

- 12. A Starting Point: Statement of Financial Position Lec 3: Financial Accouting 12

- 13. Liabilities Lec 3: Financial Accouting 13

- 14. Owners’ Equity Lec 3: Financial Accouting 14

- 15. The Accounting Equation Lec 3: Financial Accouting 15

- 16. • Sol: a. 578000=342000- X X = 578000 – 3420000 X = 236000 Lec 3: Financial Accouting 16

- 17. Lec 3: Financial Accouting 17

- 18. Sol: Lec 3: Financial Accouting 18

- 19. Debit & Credit Rules • Whenever an accounting transaction happens, a minimum of two accounts is always impacted, with a debit entry being recorded against one account and a credit entry being recorded against another account. • A debit is an accounting entry that either increases an asset or expense account. Or decreases a liability or equity account. It is positioned on the left in an accounting entry. • A credit is an accounting entry that increases either a liability or equity account. Or decreases an asset or expense account. It is positioned on the right in an accounting entry. Lec 3: Financial Accouting 19

- 20. Debit & Credit Rules Lec 3: Financial Accouting 20

- 21. Lec 3: Financial Accouting 21

- 22. Sol: Lec 3: Financial Accouting 22

- 23. General Journal • A journal is a diary of business activities. • There are different types of accounting journals. • Transactions are entered in the journal in chronological order. Recording a Business Transaction 1. Analyze the financial event. • Identify the accounts affected. • Classify the accounts affected. • Determine the amount of increase or decrease for each account affected. 2. Apply the rules of debit and credit. • Which account is debited? For what amount? • Which account is credited? For what amount? 3. Make the entry in T-account form. 4. Record the complete entry in general journal form. Lec 3: Financial Accouting 23

- 24. General Journal Transaction: On November 6, Trayton Eli withdrew $100,000 from personal savings and deposited it in a new business checking account for Eli’s Consulting Services. Lec 3: Financial Accouting 24

- 25. General Journal Transaction: On November 6, Trayton Eli withdrew $100,000 from personal savings and deposited it in a new business checking account for Eli’s Consulting Services. Lec 3: Financial Accouting 25

- 26. Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 4-26 Cash Purchase of Equipment On November 7, Eli’s Consulting Services issued Check 1001 for $5,000 to purchase a computer and other equipment.

- 27. Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 4-27 Purchase of Equipment on Credit On November 10, Eli’s Consulting Services purchased office equipment on account for $6,000.

- 28. Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 4-28 Cash Purchase of Supplies On November 28, Eli’s Consulting Services purchased supplies for $1,500, Check 1002.

- 29. Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 4-29 Payment to a Creditor On November 30, Eli’s Consulting Services paid Office Plus $2,500 in partial payment of Invoice 2223, Check 1003. • Remember, in the general journal, always enter debits before credits!

- 30. Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 4-30 Recording a Prepayment of Rent On November 30, Eli’s Consulting Services wrote Check 1004 for $8,000 to prepay rent for December and January.

- 31. Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 4-31 Services Performed for Cash Eli’s Consulting performed services for $36,000 in cash.

- 32. Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 4-32 Performed Services on Account Eli’s Consulting performed services on account for $11,000.

- 33. Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 4-33 Received Cash From Credit Clients Received $6,000 in cash from a credit client on account.

- 34. Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 4-34 Paid Salaries Paid $8,000 for salaries.

- 35. Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 4-35 Paid Utility Bill Eli’s Consulting paid $650 in cash for a utility bill.

- 36. Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 4-36 Owner’s Withdrawal The owner, Trayton Eli, withdrew $5,000 from the company.

- 37. Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 4-37 Preparing Compound Entries (1 of 2) Some transactions require a compound entry—a journal entry that contains more than one debit or credit. BUSINESS TRANSACTION: On November 7, the firm purchased equipment for $5,000, issued Check 1001 for $2,500, and agreed to pay the balance in 30 days. Remember: No matter how many accounts are affected by a transaction, total debits must equal total credits.

Editor's Notes

- Section 1, Objective 4-1: On November 7, Eli’s Consulting Services issued Check 1001 for $5,000 to purchase a computer and other equipment. Equipment needs to be debited for $5,000 and Cash needs to be credited for $5,000. Here is the general journal.

- Section 1, Objective 4-1: Remember when we previously analyzed this transaction, we decided that we would debit Equipment for $6,000 and credit Accounts Payable for the same amount. Here is the journal entry. Remember to include all important information in the explanation. This improves the audit trail.

- Section 1, Objective 4-1: Next, Eli’s Consulting Services purchased supplies for $1,500 cash, so we need to debit Supplies for $1,500 and credit Cash for the same amount. Here is the general journal entry for the transaction.

- Section 1, Objective 4-1: Now let’s look at a partial payment on account to a supplier. On November 30, Eli’s Consulting Services paid Office Plus $2,500 in partial payment of Invoice 2223, Check 1003. When the business pays part of its bill for the equipment purchased earlier, it would debit Accounts Payable and credit Cash for $2,500. Remember, in the general journal, always enter debits before credits!

- Section 1, Objective 4-1: On November 30, Eli’s Consulting Services wrote Check 1004 for $8,000 to prepay rent for December and January. When the business pays for two months rent in advance, it debits Prepaid Rent for $8,000 and credits Cash for $8,000. Note that both accounts affected are assets. Here is the general journal entry.

- Section 1, Objective 4-1: Let’s take a look at how transactions affecting revenues and expenses will be recorded in the journal. Let’s look a transaction where the business performed services for $36,000 in cash. When the business performs consulting services and gets paid immediately, Eli’s Consulting will debit Cash for $36,000 and credit Fees Income for the same amount. Here is the general journal entry.

- Section 1, Objective 4-1: Next, let’s assume that the firm performed services for $11,000 on account. Remember that we record the revenue as earned even though we haven’t yet received the cash. When the firm performs services for credit clients, it will debit Accounts Receivable and credit Fees Income for $11,000. Here is the general journal entry on the 31st.

- Section 1, Objective 4-1: Now let’s see how we would record the collection of cash for an amount previously billed. When the firm collects $6,000 from credit customers, it needs to debit Cash and credit Accounts Receivable. Here is the general journal entry.

- Section 1, Objective 4-1: It’s time to review how we would record transactions involving expenses. Our focus will be on journalizing the transaction. When the business pays $8,000 in salaries to its employees, they would debit Salaries Expense for $8,000 and credit Cash for the same amount. Here is the general journal entry.

- Section 1, Objective 4-1: When the business pays a utility bill of $650, it will debit Utilities Expense and credit Cash for the $650 as shown in the general journal entry.

- Section 1, Objective 4-1: When the owner withdraws $5,000 for personal use, the accountant will debit the Trayton Eli, Drawing account and credit the Cash account for the $5,000 withdrawal as shown. Remember that the drawing account is an equity account; not an expense.

- Section 1, Objective 4-2: PREPARING COMPOUND ENTRIES So far, each journal entry consists of one debit and one credit. Some transactions require a compound entry—a journal entry that contains more than one debit or credit. In a compound entry, record all debits first, followed by the credits. On November 7, the firm purchased equipment for $5,000, issued Check 1001 for $2,500, and agreed to pay the balance in 30 days. Remember: No matter how many accounts are affected by a transaction, total debits must equal total credits.