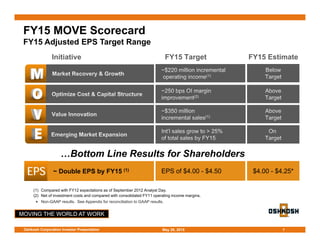

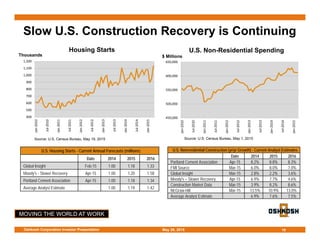

Oshkosh Corporation provides a presentation at the KeyBanc Capital Markets Industrial, Automotive & Transportation Conference on May 28, 2015. The presentation summarizes Oshkosh's business segments, financial performance in FY14 and Q2 FY15, and outlook for FY15. It highlights growth in non-defense segments, cost reduction initiatives, new product launches, and an adjusted EPS target range of $4.00-$4.25 for FY15. The presentation also discusses opportunities and challenges for each business segment and Oshkosh's focus on executing its MOVE strategy to drive margin expansion and total shareholder returns.