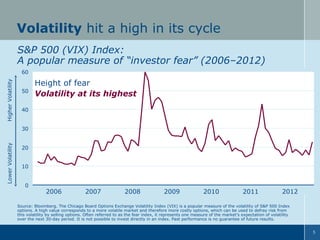

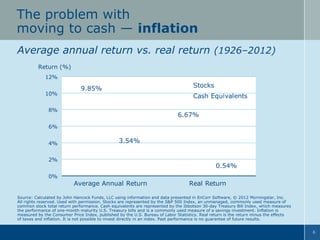

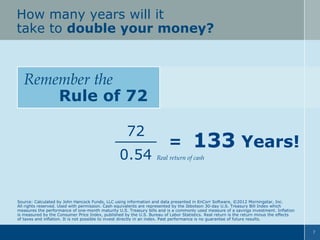

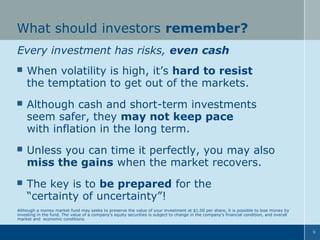

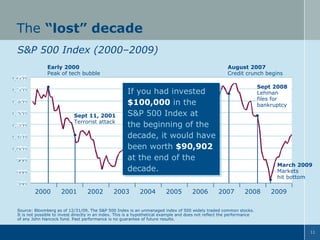

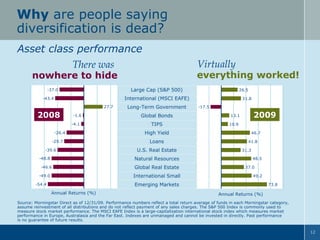

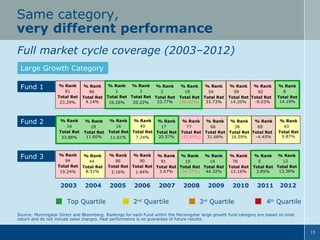

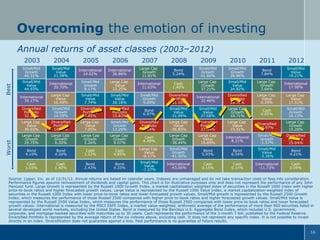

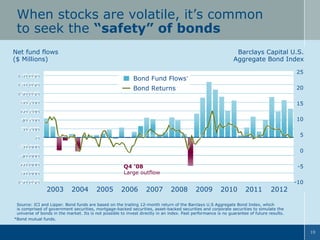

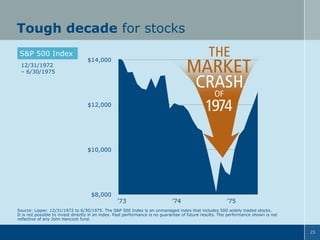

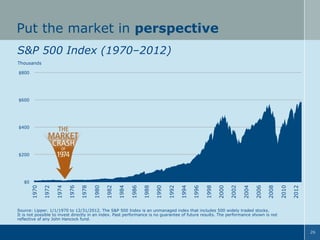

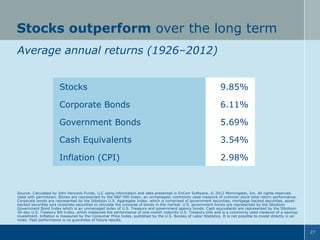

The document provides 5 investing principles based on a presentation about lessons learned. Principle 1 discusses that every investment has risks, even cash, as investors flocked to cash during volatile periods but it provided little return over the long run after accounting for inflation. Principle 2 notes that while most asset classes declined in 2008, a diversified portfolio still worked over the full market cycle from 2000-2009. Principle 3 explains that not all bonds or bond funds perform the same way. Principle 4 asserts that stocks have generally outperformed over the long run. Principle 5 advocates for including international stocks rather than avoiding foreign markets.

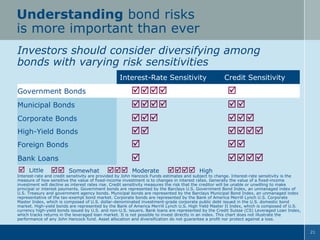

![[EN] To be or not to be invested - Fixed-Income Market Intelligence](https://cdn.slidesharecdn.com/ss_thumbnails/voorbeeldcolumn02-150825102850-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)