Jindal Steel & Power Limited is an Indian steel and energy company with production facilities located in India and abroad. Over the past three fiscal years (2008-2009 to 2010-2011), the company's total income has increased from Rs. 7,799 crores to Rs. 9,678 crores while net profit has risen from Rs. 1,537 crores to Rs. 2,064 crores. The company's subsidiaries include Jindal Power Limited, which generated a profit of Rs. 2,002 crores on revenues of Rs. 3,564 crores in fiscal year 2010-2011. The directors have recommended a dividend of 150% (Rs. 1.50 per share) for the latest fiscal

amrapali complaints official builders amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews. amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official r

amrapali complaints official builders amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews. amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official reviews amrapali group said that amrapali movie complaints was wrong. amrapali movie not horror full amrapali group waves are true but amrapali it raids got made wrong amrapali reviews.amrapali builders official r

Buzz on Corporate Laws: eNewsletter: June 2014 issuePrakash Pandya

Buzz on Corporate Laws, an eNewsletter of P. K. Pandya & Co.: June 2014 issue - covers legal updates. To subscribe http://newsletter.pkpandya.com/?p=subscribe&id=1

Buzz on Corporate Laws, an eNewsletter of P. K. Pandya & Co.: July 2014 Part 1 issue - covers legal updates. To subscribe http://newsletter.pkpandya.com/?p=subscribe&id=1

Latest Companies (Accounts) Amendment Rules, 2016

Greatest relief to Unlisted companies and its auditors - No need to prepare consolidated financial statements. Please refer notification below

Buzz on Corporate Laws: eNewsletter: June 2014 issuePrakash Pandya

Buzz on Corporate Laws, an eNewsletter of P. K. Pandya & Co.: June 2014 issue - covers legal updates. To subscribe http://newsletter.pkpandya.com/?p=subscribe&id=1

Buzz on Corporate Laws, an eNewsletter of P. K. Pandya & Co.: July 2014 Part 1 issue - covers legal updates. To subscribe http://newsletter.pkpandya.com/?p=subscribe&id=1

Latest Companies (Accounts) Amendment Rules, 2016

Greatest relief to Unlisted companies and its auditors - No need to prepare consolidated financial statements. Please refer notification below

Indian company profile analysis- Adani, Kotak Mahindra, ICICI SecuritiesAditya Deshpande

Done at basic level for interest

Content

Introduction and history of the company

SWOT analysis

Financial analysis (2015-16, 2014-15, 2013-14)

Sales / revenue analysis (2015-16, 2014-15, 2013-14)

Comparison with one competing company

Mergers and acquisition of the company (if any)

Feel free to contact @ deshadi805@gmail.com

This snapshot has been compiled to give an overview of the FPO of Shikhar Insurance Company Limited (SICL) to interested investors willing to apply in the upcoming Further Public Offerings of the ordinary shares by the SICL.

What is the banking industry? The banking industry includes systems of financial institutions called banks that help people store and use their money. Banks offer clients the opportunity to open accounts for different purposes, like saving or investing their money.

Munjal auto Industries is among the best manufacturers of Exhaust System, 2 wheelers and 4 wheelers accessories like wheel rim, Fuel tank, seat structure, side step assembly and many more.

RMD24 | Debunking the non-endemic revenue myth Marvin Vacquier Droop | First ...BBPMedia1

Marvin neemt je in deze presentatie mee in de voordelen van non-endemic advertising op retail media netwerken. Hij brengt ook de uitdagingen in beeld die de markt op dit moment heeft op het gebied van retail media voor niet-leveranciers.

Retail media wordt gezien als het nieuwe advertising-medium en ook mediabureaus richten massaal retail media-afdelingen op. Merken die niet in de betreffende winkel liggen staan ook nog niet in de rij om op de retail media netwerken te adverteren. Marvin belicht de uitdagingen die er zijn om echt aansluiting te vinden op die markt van non-endemic advertising.

Putting the SPARK into Virtual Training.pptxCynthia Clay

This 60-minute webinar, sponsored by Adobe, was delivered for the Training Mag Network. It explored the five elements of SPARK: Storytelling, Purpose, Action, Relationships, and Kudos. Knowing how to tell a well-structured story is key to building long-term memory. Stating a clear purpose that doesn't take away from the discovery learning process is critical. Ensuring that people move from theory to practical application is imperative. Creating strong social learning is the key to commitment and engagement. Validating and affirming participants' comments is the way to create a positive learning environment.

What are the main advantages of using HR recruiter services.pdfHumanResourceDimensi1

HR recruiter services offer top talents to companies according to their specific needs. They handle all recruitment tasks from job posting to onboarding and help companies concentrate on their business growth. With their expertise and years of experience, they streamline the hiring process and save time and resources for the company.

Taurus Zodiac Sign_ Personality Traits and Sign Dates.pptxmy Pandit

Explore the world of the Taurus zodiac sign. Learn about their stability, determination, and appreciation for beauty. Discover how Taureans' grounded nature and hardworking mindset define their unique personality.

"𝑩𝑬𝑮𝑼𝑵 𝑾𝑰𝑻𝑯 𝑻𝑱 𝑰𝑺 𝑯𝑨𝑳𝑭 𝑫𝑶𝑵𝑬"

𝐓𝐉 𝐂𝐨𝐦𝐬 (𝐓𝐉 𝐂𝐨𝐦𝐦𝐮𝐧𝐢𝐜𝐚𝐭𝐢𝐨𝐧𝐬) is a professional event agency that includes experts in the event-organizing market in Vietnam, Korea, and ASEAN countries. We provide unlimited types of events from Music concerts, Fan meetings, and Culture festivals to Corporate events, Internal company events, Golf tournaments, MICE events, and Exhibitions.

𝐓𝐉 𝐂𝐨𝐦𝐬 provides unlimited package services including such as Event organizing, Event planning, Event production, Manpower, PR marketing, Design 2D/3D, VIP protocols, Interpreter agency, etc.

Sports events - Golf competitions/billiards competitions/company sports events: dynamic and challenging

⭐ 𝐅𝐞𝐚𝐭𝐮𝐫𝐞𝐝 𝐩𝐫𝐨𝐣𝐞𝐜𝐭𝐬:

➢ 2024 BAEKHYUN [Lonsdaleite] IN HO CHI MINH

➢ SUPER JUNIOR-L.S.S. THE SHOW : Th3ee Guys in HO CHI MINH

➢FreenBecky 1st Fan Meeting in Vietnam

➢CHILDREN ART EXHIBITION 2024: BEYOND BARRIERS

➢ WOW K-Music Festival 2023

➢ Winner [CROSS] Tour in HCM

➢ Super Show 9 in HCM with Super Junior

➢ HCMC - Gyeongsangbuk-do Culture and Tourism Festival

➢ Korean Vietnam Partnership - Fair with LG

➢ Korean President visits Samsung Electronics R&D Center

➢ Vietnam Food Expo with Lotte Wellfood

"𝐄𝐯𝐞𝐫𝐲 𝐞𝐯𝐞𝐧𝐭 𝐢𝐬 𝐚 𝐬𝐭𝐨𝐫𝐲, 𝐚 𝐬𝐩𝐞𝐜𝐢𝐚𝐥 𝐣𝐨𝐮𝐫𝐧𝐞𝐲. 𝐖𝐞 𝐚𝐥𝐰𝐚𝐲𝐬 𝐛𝐞𝐥𝐢𝐞𝐯𝐞 𝐭𝐡𝐚𝐭 𝐬𝐡𝐨𝐫𝐭𝐥𝐲 𝐲𝐨𝐮 𝐰𝐢𝐥𝐥 𝐛𝐞 𝐚 𝐩𝐚𝐫𝐭 𝐨𝐟 𝐨𝐮𝐫 𝐬𝐭𝐨𝐫𝐢𝐞𝐬."

Memorandum Of Association Constitution of Company.pptseri bangash

www.seribangash.com

A Memorandum of Association (MOA) is a legal document that outlines the fundamental principles and objectives upon which a company operates. It serves as the company's charter or constitution and defines the scope of its activities. Here's a detailed note on the MOA:

Contents of Memorandum of Association:

Name Clause: This clause states the name of the company, which should end with words like "Limited" or "Ltd." for a public limited company and "Private Limited" or "Pvt. Ltd." for a private limited company.

https://seribangash.com/article-of-association-is-legal-doc-of-company/

Registered Office Clause: It specifies the location where the company's registered office is situated. This office is where all official communications and notices are sent.

Objective Clause: This clause delineates the main objectives for which the company is formed. It's important to define these objectives clearly, as the company cannot undertake activities beyond those mentioned in this clause.

www.seribangash.com

Liability Clause: It outlines the extent of liability of the company's members. In the case of companies limited by shares, the liability of members is limited to the amount unpaid on their shares. For companies limited by guarantee, members' liability is limited to the amount they undertake to contribute if the company is wound up.

https://seribangash.com/promotors-is-person-conceived-formation-company/

Capital Clause: This clause specifies the authorized capital of the company, i.e., the maximum amount of share capital the company is authorized to issue. It also mentions the division of this capital into shares and their respective nominal value.

Association Clause: It simply states that the subscribers wish to form a company and agree to become members of it, in accordance with the terms of the MOA.

Importance of Memorandum of Association:

Legal Requirement: The MOA is a legal requirement for the formation of a company. It must be filed with the Registrar of Companies during the incorporation process.

Constitutional Document: It serves as the company's constitutional document, defining its scope, powers, and limitations.

Protection of Members: It protects the interests of the company's members by clearly defining the objectives and limiting their liability.

External Communication: It provides clarity to external parties, such as investors, creditors, and regulatory authorities, regarding the company's objectives and powers.

https://seribangash.com/difference-public-and-private-company-law/

Binding Authority: The company and its members are bound by the provisions of the MOA. Any action taken beyond its scope may be considered ultra vires (beyond the powers) of the company and therefore void.

Amendment of MOA:

While the MOA lays down the company's fundamental principles, it is not entirely immutable. It can be amended, but only under specific circumstances and in compliance with legal procedures. Amendments typically require shareholder

Cracking the Workplace Discipline Code Main.pptxWorkforce Group

Cultivating and maintaining discipline within teams is a critical differentiator for successful organisations.

Forward-thinking leaders and business managers understand the impact that discipline has on organisational success. A disciplined workforce operates with clarity, focus, and a shared understanding of expectations, ultimately driving better results, optimising productivity, and facilitating seamless collaboration.

Although discipline is not a one-size-fits-all approach, it can help create a work environment that encourages personal growth and accountability rather than solely relying on punitive measures.

In this deck, you will learn the significance of workplace discipline for organisational success. You’ll also learn

• Four (4) workplace discipline methods you should consider

• The best and most practical approach to implementing workplace discipline.

• Three (3) key tips to maintain a disciplined workplace.

Affordable Stationery Printing Services in Jaipur | Navpack n PrintNavpack & Print

Looking for professional printing services in Jaipur? Navpack n Print offers high-quality and affordable stationery printing for all your business needs. Stand out with custom stationery designs and fast turnaround times. Contact us today for a quote!

Explore our most comprehensive guide on lookback analysis at SafePaaS, covering access governance and how it can transform modern ERP audits. Browse now!

Buy Verified PayPal Account | Buy Google 5 Star Reviewsusawebmarket

Buy Verified PayPal Account

Looking to buy verified PayPal accounts? Discover 7 expert tips for safely purchasing a verified PayPal account in 2024. Ensure security and reliability for your transactions.

PayPal Services Features-

🟢 Email Access

🟢 Bank Added

🟢 Card Verified

🟢 Full SSN Provided

🟢 Phone Number Access

🟢 Driving License Copy

🟢 Fasted Delivery

Client Satisfaction is Our First priority. Our services is very appropriate to buy. We assume that the first-rate way to purchase our offerings is to order on the website. If you have any worry in our cooperation usually You can order us on Skype or Telegram.

24/7 Hours Reply/Please Contact

usawebmarketEmail: support@usawebmarket.com

Skype: usawebmarket

Telegram: @usawebmarket

WhatsApp: +1(218) 203-5951

USA WEB MARKET is the Best Verified PayPal, Payoneer, Cash App, Skrill, Neteller, Stripe Account and SEO, SMM Service provider.100%Satisfection granted.100% replacement Granted.

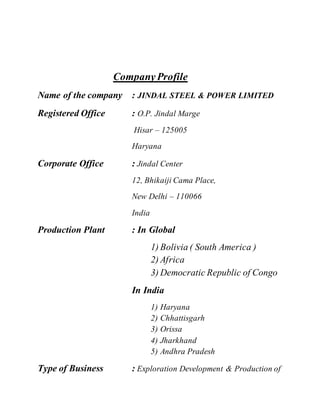

1. CompanyProfile

Name of the company : JINDAL STEEL & POWER LIMITED

Registered Office : O.P. Jindal Marge

Hisar – 125005

Haryana

Corporate Office : Jindal Center

12, Bhikaiji Cama Place,

New Delhi – 110066

India

Production Plant : In Global

1) Bolivia ( South America )

2) Africa

3) Democratic Republic of Congo

In India

1) Haryana

2) Chhattisgarh

3) Orissa

4) Jharkhand

5) Andhra Pradesh

Type of Business : Exploration Development & Production of

2. Steel, Petroleum and Cement

Network of company : Jindal Steel & Power ltd.

Jindal Petroleum ltd.

Jindal Cement ltd.

Jindal Power Trading company ltd.

Jindal Power ltd.

Mission statement : “TAKING INDIA AHEAD”

Web Site : www.jindalsteelpower.com

3. Historyof Company

1998

- The name of the Company has been changed from Orbit Strips Ltd. to

Jindal Steel & Power Ltd. on 12th June.

1999

- Shri O.P. Jindal, Shri Ratan Jindal and Shri M.L. Gupta were

Appointed as Additional Directors of the Company in terms of Section

260 of the Companies Act, 1956 and Article 117 of Articles of

Association of the Company.

- Shri M.L. Gupta, appointed as Whole time Director of the Company

w.e.f. 1st May for a period of five years.

- The Company has joined the Depository System and its securities

Can be dematerialized.

- The Raigarh and Raipur Divisions of Jindal Strips Limited have been

hived off to JINDAL STEEL & POWER LIMITED pursuant to the

Scheme of Arrangement approved by Hon'ble High Court of Punjab and

Haryana.

- The Company has issued 14% 60, 00,000 Cumulative Redeemable

Preference Shares of Rs. 100/- each aggregating to Rs. 60 crores on

private placement basis.

- The Steel Melting Shop of the Company, was shut down in May'98

due to the explosion. It was commissioned in Oct '99.

4. 2007

-Jindal Steel & Power Ltd has appointed Shri A K Purwar, former

Chairman, State Bank of India as an Independent Director on the Board

of the Company with immediate effect.

- Jindal Steel & Power Ltd has informed that the Board of Directors of

the Company has (by circulation) appointed Shri. Ram Vinay Shahi as

Additional Director (Independent) and member of the Audit Committee

of Directors with effect from October 15, 2007.

-Jindal Steel & Power Ltd has appointed Shri. Arun Kumar Mukherji as

an Additional Director and Wholetime Director of the Company with

effect from April 01, 2008

2008

- The Company has splits its face value from Rs5/- to Rs1/-.

-Jindal Steel & Power Ltd has informed that Jindal Power Ltd (JPL),

subsidiary of the Company, on September 05, 2008 has commissioned

fourth power generating unit of 250 MW. With this, the subsidiary

Company has completed the 1000 MW power project and has now the

capacity to generate 1000 MW power from this plant.

5. 2009

- Jindal Steel & Power Ltd has informed BSE that the Board of

Directors has, vide resolution passed through circulation on January

14, 2009, appointed Shri. Ashok K Mohapatra, Shri. Haigreve Khaitan,

Shri Hardip Singh Wirk and Shri Rahul Mehra as independent directors

of the Company with effect from January 14, 2009

- Jindal Steel & Power Ltd has appointed Shri Arun Kumar as

independent directors of the Company w.e.f September 16, 2009

- Jindal Steel & Power Ltd has appointed Shri. Arun Kumar as an

Additional Director (Independent) from September 16, 2009, to hold

office up to the date of next Annual General Meeting of the Company

6. Index

Sr.No. Particular Page No.

1 Organization Structure

2 Company Information

3 Financial result at Glance for 3 years

4 Abstract of Balance sheet for 3 years

5 Abstract of Profit & Loss Account for 3 years

6 Accounting Policies

7 Director’s Report

8 Auditor’s Report

9 Market Value of Equity

10 Meaning & Utility of Ratio Analysis

11 Ratio with detailed interpretation

12 Limitation of Ratio Analysis

13 Common size Balance sheet

14 Common size Profit & Loss Account

15 Cash flow statement for 3 years

16 Leverage analysis & amount of trade on equity

17 Stock market price in comparison with BSE & NSE

18 Social Responsibility of Company

19 Product of Company

20 Conclusion

21 Bibliography

22 Declaration

9. Company Information

Name of Company : Jindal Steel & Power Limited

Board of Directors :

1) Smt. Savitri Jindal, Chairperson Emeritus

2) Shri Naveen Jindal, Chairman & Managing Director

3) Shri Ratan Jindal, Director

4) Shri Vikrant Gujral, Group Vice Chairman & Head

Global Ventures

5) Shri Anand Goel, Jt. Managing Director

6) Shri Sushil Maroo, Director

7) Shri N A Ansar, Wholetime Director

8) Shri S. Ananthakrishnan, Nominee Director-IDBI

Bank Limited, Independent

9) Shri R. V. Shahi, Director, Independent

10) Shri Arun K. Purwar, Director, Independent

11) Shri Arun Kumar, Director, Independent

12) Shri Haigreve Khaitan, Director, Independent

13) Shri Hardip Singh Wirk, Director, Independent

14) Shri Rahul Mehra, Director, Independent

Deputy Company Secretary : Mr. T.K. Sadhu

10. Name of Bankers : 1) State Bank of India

2) Punjab Bank of India

3) IDBI Bank Limited

Statutory Auditors : M/S Lodha & Co.

12/ Bhagat Singh Marg,

New Delhi – 110001

India.

11. Financial Result of Company At Glance For Last 3 Years

Particular 2008-‘09 2009-‘10 2010-‘11

Net Sales 7,365.19 7,367.59 9,534.89

Other Income 146.24 117.31 143.71

Total Income 7,799.43 7,484.90 9,678.60

Total Expense 5,160.52 4,825.20 5,744.39

PBIT 2,638.91 2,659.61 3,790.50

Interest 204.00 239.95 355.02

Depreciation 433.03 512.15 687.77

PBEI 2,001.88 1,907.51 2,753.36

Other none ope. Exp. - - -

PBT 2,001.88 1,907.51 2,753.36

Provision for Tax 465.40 427.82 689.24

Net Profit 1,536.98 1,479.69 2,064.12

13. -Liabilities 2,446.20 2,898.40 2,810.61

-Provision 985.81 1,343.71 1,896.34

Total(B) (3,432.01) (4,242.11) (4,706.95)

Net Current Assets 1,677.41 1,634.79 3,390.85

Miscellaneous Expenditure 3.02 3.02 3.19

Total 10,977.74 15,844.26 21,682.34

14. Profit & Loss Account

Particular 31-03-2009 31-03-2010 31-03-2011

Sales & Operational Income 8,953.77 8,595.67 12,158.73

-Less: Inter Division Transfer (519.96) (700.09) (1,698.30)

-Less: Excise Duty (780.62) (527.99) (886.80)

Net Sale & Operational Income 7,653.19 7,367.59 9,573.63

Other Income 146.24 117.31 143.71

Total 7,799.43 7,484.90 9,717.34

Expenditure

-Material, Manufacturing &

Other

4,219.19 4,062.16 4,827.92

-Personal 177.53 212.75 277.78

-Administration & selling 798.69 597.86 885.50

-Interest 168.91 192.47 285.01

-Miscellaneous Expenditure

writ. Off

0.20 - -

-Depreciation 433.03 512.16 687.77

Total (5,797.55) (5,577.40) (6,963.98)

Profit before Taxation 2,001.88 1,907.50 2,753.36

Less: Provision for Taxation

-Income tax (355.93) (312.48) (525.12)

-Deferred tax (105.10) (115.23) (163.33)

-Wealth tax (0.19) (0.07) (0.42)

-Fringe Benefits tax (4.18) (0.04) (0.37)

Profit After Tax 1,536.48 1,479.68 2,064.12

Add: Surplus Brought forward

from previous Year

3,047.80 4,318.95 5,478.83

Balance of Profit Brought

Forward

4,584.28 5,798.63 7,542.95

15. Basic Accounting Policies

Basis of Preparation of Financial Statements:

The financial statements are prepared under the historical

cost convention, ongoing concern basis and in term of the

Accounting standards issued by the Institute of Charterd

Accountants of India and in compliance with section 211(3c) of

companies Act, 1956

The Company follows the mercantile system of accounting

and recognizes income and expenditure on accrual basis to the

extent measurable and where there is a certainty of ultimate

realization in respect of incomes.

Fixed Assets:

Fixed Assets acquired by the company pursuant to a scheme

of arrangement are stated at their transfer values.

Intangible Assets:

Intangible assets are recognized on the basis of recognized

criteria as set out in accounting standard (AS-26)”Intangible

Assets”.

Depreciation:

Depreciation on fixed assets is provided on straight-line

method (SLM) at the rates and in the manner specified in schedule

XIV to the companies Act, 1956

Certain Plant & Machinery have been considered as

continuous process plant on the basis of technical assessment and

depreciation on the same provided for accordingly.

16. Investment:

Long term Investments are carried at the cost provision

is made when in the opinion of the management diminution in the

value of investment is other than temporary in nature. Current

investments are carried at the lower of cost or market fair value.

Taxes on Income:

Provision for current tax is made considering various

allowances and benefits available to the company under the

provisions of the Income Tax Act, 1961

17. Director’s Report

Financial Result:

(Rs. in crores)

Particular 31-03-2010 31-03-2011

Sales & other income 7,484.90 9,717.34

Profit before interest and depreciation 2,612.13 3,726.14

Profit before tax 1,907.50 2,753.36

Profit after tax 1,479.68 2,064.12

Appropriations:

Interim dividend - -

Final dividend 116.52 140.19

Corporate tax on dividend 4.28 3.75

General reserve 150.00 210.00

Subsidiary Company:

Jindal Power Limited has closed financial

year 2010-11 with total income of Rs.3,564.35 crores and earned a

profit after tax Rs.2,001.60 crores.

Dividend:

Your Directors recommend a dividend of 150%

i.e. Rs. 1.50 per equity share of Re. 1/- each. Stock Options under Series

III (Part III) will vest in the employees on 27th April, 2011 and shares

will be allotted against these Options in due course. These shares will

rank pari-passu with the existing shares in all respects. Accordingly,

provision for payment of dividend for the financial year 2010-11 has

also been made in respect of 7,40,625 equity shares being the maximum

number of shares that may be allotted on exercise of these Options.

18. Corporate Governance:

The company has implanted the conditions of corporate

Governance as contained in Clause 49 of listing agreement. Separate

reports on Corporate Governance and Management Discussion and

Analysis along with necessary certificates are given elsewhere in this

Annual Report.

Future Issue of Capital:

The Company has allotted 30,23,507 equity shares of Re.1/-

each on various dates against options granted under the Company’s

Employee Stock Option Scheme- 2005 during the period under report.

19. Auditor’s Report

We have audited the attached balance sheet of Jindal

Steel & Power Limited, as at 31st March, 2011, the profit & loss

Account and the Cash flow statement for the year ended on that

date annexed there at these financial statements are the

responsibility of the company’s managements. Our responsibility is

to express on opinion these financial statements based on our

audit.

As required by the companies (Auditor’s Report) Order,

2003 as amended by the companies Auditor’s report amendment

order, 2004 (together the ‘order’) issued by the Central

Government of India in terms of sub section (4A) of section 227 of

the Annexure, a statements on the matters specified in paragraphs

4 & 5 of the said order.

Annexure to Auditor’s Report:

The company has maintained proper recodes showing fall

particulars including quantitative detail and situation of fixed

assets.

Fixed assets disposed of during the year were not

substantial.

The company has not taken any loans, Secured or

Unsecured from companies, firm or other parties listed in

the register maintained under section 301 of the companies

Act, 1956

In our opinion the company has an internal audit system

commensurate with the size and nature if it’s business.

21. Meaning and Importance of Ratio

Meaning:

“Ratio analysis is process comparison of one

figure against another and the interpretation of ratio to known the

strengths and weaknesses of firm and its position”.

Importance:

1. Profitability:

Useful information about the trend of

profitability is available from ratio. The Gross profit ratio, Net

profit ratio, And ratio of return on investment give a good idea

of profitability of business.

2. Liquidity:

In fact, the use of ratio was made initially to

ascertain the liquidity of business. The current ratio, liquid

ratio, & acid test ratio will tell whether the business will be

able to meats its current liabilities as and when they mature.

3. Efficiency:

The turnover ratio are excellent guides to

measures the efficiency of manager. For example, the stock

turnover ratio will indicates how efficient the sale is being made

& assets turnover shows the efficiency with which the assets are

used in business.

22. 4. Inter-Firm Comparison:

The absolute ratios of a firm are not much use,

unless they are compared with similar ratios of the other firm

belonging to the same industry.

5. Useful for budgetary Control:

Regularly budgetary reports are prepared in

business where the system of budgetary control is in use.

6. Useful for Decision Making:

Ratios guide the management in making some

of the importance decisions. Supposed, the liquidity ratio shows

unsatisfactory positions, the management may decide to get

additionalliquid funds.

23. Ratio Analysis

Gross Profit Ratio:

It is the basic measure of Profitability of business. It

expresses relationship between gross profits earned to net sales.

Formula:

Gross Profit × 100

Net sales

Gross Profit: Sales- Cost of Goods Sales

Particular 2009 2010 2011

Net Sales 7,653.19 7,367.59 9,573.63

Gross Profit 2,638.91 2,659.61 3,934.21

Ratio (%) 34.48% 36.1% 41.09%

Interpretation:

In the first year Gross Profit Ratio of the company

was 34.48 %. It is good in Second year when it increase and become

36.1 % in the third year it increases and become 41.09 % which is

satisfactory for company.

0.00

2,000.00

4,000.00

6,000.00

8,000.00

10,000.00

12,000.00

2009 2010 2011

Gross Profit

Net Sales

24. Net Profit Ratio:

The net profit is obtained after charging operating

Expenses, interest, depreciation and taxes to gross profit.

Formula: Net Profit × 100

Net Sales

Net Profit: Profit after Tax

Particular 2009 2010 2011

Net Sales 7,653.19 7,367.59 9,573.63

Net Profit 1,581.93 1,479.68 2,064.12

Ratio (%) 20.60% 20.08% 21.56%

Interpretation:

The Net Profit Ratio of first year and second

year was 20.60 % and 20.08 % in which it is decreasing but in

the third year it was 21.56 % which has been increasing. The

profitability ratio of the company is satisfactory

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

2009 2010 2011

Net Sales

Net Profit

25. Operating Ratio:

It is a ratio showing relationship cost of good

sold plus operating expenses & net sales. It shows the efficiency

of the management. The higher the ratio, the less will be the

margin available to proprietors. This ratio is also usually

expressed as a percentage.

Formula:

Cost of goods Sales+ Operating Expenses × 100

Net Sales

Particular 2009 2010 2011

Net Sales 7,653.19 7,367.59 9,573.63

COGS 5014.28 4707.98 5639.42

Operating Ex. 143.71 - -

Ratio (%) 67.39% 63.90% 58.90%

Interpretation:

With the increases in Sales, COGS and Operating

Exp. in second year comparing to first year, but at same time the

operating ratio decreases from 67.39% to 63.90% and in third year

it decreases to 58.90%.

0

5000

10000

2009 2010 2011

Net Sales

COGS

Operarting EX.

26. Return on Investment:

It is an index of profitability of business

& is obtained by comparing Profit before Interest & Taxes with

Capital Employed. The ratio is normally expressed in

percentage.

Formula:

Profit before Interest & Taxes × 100

Capital Employed

Particular 2009 2010 2011

PBIT 2,638.91 2659.61 3790.50

Capital Employed 10,374.89 15,103.90 20,799.03

Ratio (%) 26.43% 27.61% 18.22%

Interpretation:

This ratio shows how many capitals used in

this ratio. It was 26.43% in 2009, 27.61% in 2010 & 18.22% in

2011.

0

5000

10000

15000

20000

25000

2009 2010 2011

PBIT

Capital Employed

27. Return on Shareholder’s Fund:

Profit is earned in business for owners

and so they are naturally interested in return they get on their

money invested in company’s business.

Formula:

Net Profit × 100

Owner’s Fund

Particular 2009 2010 2011

Owner’s fund 5,388.13 6,723.66 8,687.55

Net Profit 1,581.93 1,479.68 2,064.12

Ratio (%) 29.35% 22.00% 23.76%

Interpretation:

Profit of company decrease in second year but it

is increases in third year which may be because of high stock

turnover ratio in third year. As a result the company can get

higher return on capital provider.

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2009 2010 2011

Owner's fund

Net Profit

28. Return on Equity Shareholder’s Funds:

It shows what percentage of profit is earned on

the capital invested by ordinary shareholders. The ratio is

obtained by dividing net profit after deduction of preference

dividend by equity shareholders fund.

Formula: Net Profit-Preference Dividend × 100

Equity Shareholder’s Fund

Particular 2009 2010 2011

Net Profit 1,581.93 1,479.68 2,064.12

Equity Share 16.47 93.12 93.43

Ratio (%) 96.04% 15.89% 22.09%

Interpretation:

Here, at glance of last 3 year amount available

for dividend purpose is decreasing every year.

0

500

1000

1500

2000

2500

2009 2010 2011

Net Profit

Equty Share

29. Return on Total Assets:

The return on total assets implies how the funds

supplied by both owners & creditors are utilized in business.

Formula: Net Profit × 100

Total Assets

Particular 2009 2010 2011

Net Profit 1,581.93 1,479.68 2,064.12

Total Assets 7,619.73 10,377.97 15,129.26

Ratio (%) 20.76% 14.26% 13.64%

Interpretation:

Here, as company is getting experienced its

utilization of funds for enterprise is also improving which is good.

0

5000

10000

15000

20000

2009 2010 2011

Net Profit

Total Assets

30. Earnings Per Share:

The ratio is obtained by dividing net profit after

deduction of preference dividend by number of Equity share.

Formula: Net Profit- Preferences Dividend ×100

No. of Equity Share

Particular 2009 2010 2011

Net Profit 1,581.93 1,479.68 2,064.12

No. of Equity 16.47 93.12 93.43

Ratio (Rs.) 96.04 15.89 22.09

Interpretation:

This ratio is very useful to the investors to know

their earnings per share in the year. Higher the ratio it will be

good for the companies prestige.

0

500

1000

1500

2000

2009 2010 2011

Net Profit

No of Equity

31. Dividend per Share:

It shows the dividend per share which

shareholders of the company get return on their investment by the

company declaration.

Formula: Purpose Dividend × 100

No of share

Particular 2009 2010 2011

Dividend 85.33 116.52 140.19

No of Share 16.47 93.12 93.43

Ratio (Rs.) 5.52 1.25 1.50

Interpretation:

This ratio shows the dividend per share. It was

5.52 Rs. in 2009, 1.25 Rs. in 2010 & 1.50 Rs in 2011.

0

50

100

150

2009 2010 2011

Dividend

No of Share

32. Debt-Equity Ratio:

This ratio shows proportion of funds

provided by long term creditors & that provides by shareholders.

Formula: Long term liability ×100

Shareholder’s fund

Particular 2009 2010 2011

Long term liability 4,962.65 8,383.26 12,114.64

Share H/D’s fund 5,388.13 6,723.66 8,687.55

Ratio (%) 9.21% 12.43% 13.95%

Interpretation:

Here, proportions of funds provided by long term

creditors & that to shareholder’s are increases therefore it’s not

good for company.

Dividend Payout Ratio:

0

5000

10000

15000

Category 1 Category 2 Category 3

Long term Liability

Share H/D's Fund

33. It is the proportion of actual dividend

received to the earning per share.

Formula: Dividend Per Share × 100

Earnings Per Share

Particular 2009 2010 2011

DPS 5.52 1.25 1.50

EPS 96.04 15.89 22.09

Ratio (%) 5.5% 7.8% 6.8%

Interpretation:

Here, at glace last three year in 2010, it was

highest & it’s good from shareholder’s point of view as proportion

of actual dividend received to earning per share is increasing

every year.

0

50

100

2009 2010 2011

DPS

EPS

34. Capital Gearing Ratio:

This ratio indicates the ratio between those

capital where interest & dividend pay is compulsory with those

capital where dividend payment is not compulsory.

Formula: Fixed Interest bearing Capital

Equity share Capital

Particular 2009 2010 2011

Fixed Interest bearing Capital 4,962.65 8,383.26 12,114.64

Equity share capital 15.47 93.12 93.43

Ratio 32.08 9.02 12.97

Interpretation:

Capital gearing ratio is continuously decreasing

in given years. It shows that the fixed interest bearing capital is

more used compared to the ordinary capital.

0

2000

4000

6000

8000

10000

12000

14000

2009 2010 2011

Fixed Interest bearing Capital

Equity Share Capital

35. Proprietary Ratio:

The ratio shows the proportion of proprietary

fund to the total assets employed in the business. The proprietors

fund or shareholders’ equity consists of share capital & reserves

and surpluses.

Formula: Proprietary’s Fund × 100

Total Assets

Particular 2009 2010 2011

Proprietary’s Fund 5,412.3 6,742.98 8,684.34

Total Assets 7,619.73 10,377.97 15,129.26

Ratio (%) 71.03% 65.91% 57.40%

Interpretation:

The higher the ratio the stronger the financial position

of the company as it signifies that the proprietors have provided larger

funds to purchases the assets.

0

2000

4000

6000

8000

10000

12000

14000

16000

2009 2010 2011

Proprietary's Fund

Total Assets

36. Long Term Fund to Fixed Assets:

The fixed assets of business must be

purchased out of fixed capital only, which includes share capital,

reserve & long term liability. This ratio shows the relationship

between fixed capital & fixed assets.

Formula: Long term Liability × 100

Fixed Assets

Particular 2009 2010 2011

Long term liability 4,942.65 8,783.26 12,114.67

Fixed Assets 6,435.64 9,300.33 18,291.49

Ratio (%) 77.11% 90.14% 66.23%

Interpretation:

Long term funds to fixed assets ratio is

continuously decreasing in the given year. It is 66.23% in 2009,

90.14% in 2010 and 77.11% in 2011.

0

5000

10000

15000

20000

2009 2010 2011

Long term Liability

Fixed Assets

37. Stock turn Over Ratio:

The number of times the average stock is turned

over during the year is known as stock turnover ratio. It is

computed by dividing the cost of goods sold by the average stock in

the business.

Formula: Cost of goods sold

Average Stock

Particular 2009 2010 2011

COGS 5014.28 4707.98 5639.42

Average Stock 1,095.36 651.72 862.42

Ratio 4.58 7.22 6.54

`

Interpretation:

The ratio is very important in judging the ability

of management with which we can move the stock. The higher the

turnover ratio, the move profitable the business would be.

0

1000

2000

3000

4000

5000

6000

2009 2010 2011

COGS

Average Stock

38. Current Ratio:

This is the most widely used ratio which shows the

proportion of Current Assets to Current Liabilities. It is also

known as Working Capital Ratio.

Formula: Current Assets

Current Liability

Particular 2009 2010 2011

Current Assets 544.05 2,013.96 2,992.8

Current Liability 156.83 2,896.40 2,810.61

Ratio 3.47:1 0.7:1 1.06:1

Interpretation:

The ideal Current Ratio is 3.47:1. In first year and

second year the ratio is less than ideal ratio but in third year it is

more. It seems that the liquid position is good and there is no

unproductive investment in current assets.

Current Assets

Current Liability

0

1000

2000

3000

2009

2010

2011

Current Assets

Current Liability

39. Debtor’s Ratio:

The debtor’s ratio shows comparison of

debtors plus bill receivable of avg. daily sales. It shows the

number of days taken to collect the dues of credit sales. Higher

ratio indicates unsatisfactory position, it suggest that the credit

& collection policy are weak.

Formula: Debtor + B/R ×365

Credit Sales

Particular 2009 2010 2011

Debtor 391.46 622.36 737.12

Credit Sales 7,677.83 7,347.44 9,543.47

Ratio (Days) 18 30 28

Interpretation:

Debtor’s ratio is stable in the given years. It is

18days in the 2009, 30days in the 2010 and 28 days in the 2011

respectively. Here company’s credit policy is good for company.

0

2000

4000

6000

8000

10000

12000

2009 2010 2011

Debtor

Credit Sales

40. Fixed Assets Turnover Ratio:

The ascertain the efficiency & profitability of

business the total fixed assets are compared to sales. The more the

sales in relation to amount invested in the fixed assets, the more

efficiency is use of fixed assets.

Formula: Net Sales

Fixed Assets

Particular 2009 2010 2011

Net Sales 7,653.19 7,367.59 9,573.63

Fixed Assets 4,322.03 13,139.34 17,078.29

Ratio 1.77 0.56 0.56

Interpretation:

The ratio shows utilization of fixed assets in the

business. The ratio is low, it indicates that investment in the fixed

assets is more than what is necessary & must be reduced.

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

2009 2010 2011

Net Sales

Fixed Assets

41. Total Assets Turnover Ratio:

This ratio measures a firm’s efficiency in

utilizing its assets. It indicates how many times the assets were

turned over a period & there by generated sales. If assets turnover

is high, the company is managing its assets efficiently. If it is low,

it means the company has more assets than it really needs for its

operation.

Formula: Net Sales

Total Sales

Particular 2009 2010 2011

Net Sales 7,653.19 7,367.59 9,573.63

Total Assets 4,866.08 15,150.3 20,071.09

Ratio 1.57 0.49 0.48

Interpretation:

The Total assets turnover ratio shows the

efficiency of managing its assets. Higher the ratio, it’s better for

the company.

0

5000

10000

15000

20000

25000

2009 2010 2011

Net Sales

Total Assets

42. Current Assets turnover Ratio:

This ratio is computed to ascertain how efficiency

working capital is utilized in business.

Formula: Net Sales

Current Assets

Particular 2009 2010 2011

Net Sales 7,653.19 7,367.59 9,573.63

Current Assets 544.05 2,010.96 2,992.8

Ratio 14.08 3.66 3.20

Interpretation:

Average industrial ratio must be 2 so, it’s around

last two years which is good & shows that working capital is being

utilized nicely.

Current Assets

Net Sales

0

2000

4000

6000

8000

10000

2009 2010

2011

Current Assets

Net Sales

43. Limitation of Ratio Analysis

1) Single year ratio have limited utility:

The utility of ratio computed from the financial

statement of one year only is obviously limited.

2) Other factor must be considered:

While comparing ratio of different firms, it must be

remember that different firms follow different accountancy

plans and policies.

3) Lack of Standard Ratio:

There is practically no standard ratio against which the

actual performance can be compared.

4) Other factors Important:

Financial result of business depend upon a number of

factor such as general economic condition and competition,

local factor and the policy adopted by management.

5) Ratio of two irrelevant Figures:

Ratio must be established between related matters. It is of

no use if ratios are found between two figures.

44. Common Size Balance Sheet

Particulars (` in crores) Common Size (`)

2009 2010 2011 2009 2010 2011

SOURCES OF

FUNDS:

Share Capital 867.70 93.12 93.43 15.76 0.62 0.46

Reserve and

Surplus

1,499.84 6,630.54 8,594.12 27.28 43.89 42.53

Long Term

Loans

Secured Loan 3,132.76 4,235.16 5,530.93 56.96 28.03 27.37

Unsecured Loan - 4,148.10 6,583.74 - 27.46 32.58

TOTAL 5,500.3 15,106.92 20,208.22 100 100 100

APPLICATION

OF FUNDS:

Fixed Assets 4,322.03 13,139.34 17,078.29 76.94 82.94 78.78

Investment 244.43 1,067.11 1,210.01 4.35 6.74 5.58

Current Assets 1,538.19 5,876.90 8,097.80 27.38 37.10 37.35

- Current

Liabilities

(487.08) (4,242.11) (4,706.95) (8.6) (26.78) (21.71)

TOTAL 5,617.57 15,841.24 21,679.15 100 100 100

45. Common size Profit & Loss Account

Particular (Rs. in Crores) (Common Size)

2009 2010 2011 2009 2010 2011

Net Sales 7,365.19 7,367.59 9,534.89 100 100 100

Other Income 146.24 117.31 143.71 1.98 1.59 1.50

Total Income 7,799.43 7,484.90 9,678.60 10.58 10.16 10.15

Total Expense 5,160.52 4,825.20 5,744.39 9.50 7.67 8.89

PBIT 2,638.91 2,659.61 3,790.50 11.5 10.45 12.34

Interest 204.00 239.95 355.02 3.4 5.2 7.8

Depreciation 433.03 512.15 687.77 1.8 2.7 2.5

PBEI 2,001.88 1,907.51 2,753.36 6.3 9.81 12.87

Other none

ope. Exp.

- - - - - -

PBT 2,001.88 1,907.51 2,753.36 6.3 9.81 12.87

Provision for

Tax

465.40 427.82 689.24 1.5 2.8 4.6

Net Profit 1,536.98 1,479.69 2,064.12 5.67 7.89 8.5

46. Cash flow Statement for the year ended

31st

March, 2011

Particular 2010 2011

NET PROFIT BEFORE TAX 1,907.50 2,753.36

A. CASH INFLOW/(OUTFLOW) FROM

OPERATING ACTIVITIES

Adjustment for:

Depreciation 512.16 687.77

Premium on Investment written off 0.19 0.07

Loss / (Profit) on Sale of Fixed Assets 2.37 0.27

Loss / (Profit) on Sale of Investments (0.44) (1.13)

Dividend Income (91.90) (117.10)

Liability / Provisions no longer required

written back

(3.09) (1.79)

Provision for doubtful debts (0.78) (0.61)

Provision for doubtful advances 0.60

Employees Compensation Expenses under

Employees Stock Option Scheme

(4.85) (4.87)

Interest Paid 192.47 285.01

Operating Profit before Working

Capital Changes

2,514.23 3,600.98

Adjustment for:

Inventories (118.54) (875.62)

Sundry Debtors (230.12) (114.08)

Other Current Assets 82.67 (212.28)

Income Tax paid (292.29) (514.78)

Other Current Liabilities 447.32 (90.18)

Net Cash Inflow/(Outflow) from

Operating Activities

2,403.27 1,794.04

B. CASH INFLOW/(OUTFLOW)

FROM INVESTMENT ACTIVITIES

Capital Expenditure (5,778.54) (4,893.93)

Sale Proceeds of Fixed Assets 146.28 354.20

Dividend received 87.56 91.09

47. Loans & Advances (447.36) (398.62)

Interest Received 40.31 49.51

(Increase) / Decrease in Investments 166.53 (141.76)

Share Application Money given (26.66) (24.85)

Net Cash Inflow/(Outflow) from

Investing Activities

(5,811.88) (4,964.36)

C. CASH INFLOW/(OUTFLOW)

FROM FINANCING ACTIVITIES

State Sales Tax Subsidy 33.33 32.23

Issue of Equity Shares 12.59 11.32

Proceeds from Long T erm Borrowings 4,385.11 5,317.19

Working Capital Borrowings from Banks 658.64 1,049.92

Repayment/Adjustment of Borrowings (1,473.27) (2,469.78)

Dividend Paid (including tax thereon) (80.78) (117.59)

Interest Paid (375.87) (661.51)

Net Cash Inflow/(Outflow) from

Financing Activities

3,159.75 3,161.78

Net Cash Inflow/(Outflow) from

Financing Activities

(248.86) (8.54)

Cash & Cash equivalents (Opening

Balance)

308.96 60.10

Cash & Cash equivalents (Closing

Balance)

60.10 51.56

49. Combined Leverage:

Operating Leverage × Financial Leverage

Particular 2010 2011

OL 1.41 1.40

FL 1.23 1.21

Combined Leverage 1.73 1.69

Earning to Equity Shareholder Per Share:

Earning to Shareholder

No. of Equity Share

Particular 2010 2011

Earning to S/H 1010.6 1407.4

No. of Equity Share 93.12 93.43

Earnings per Share 10.85 15.06

50. Stock Market Price in Comparison with

BSE & NSE

For the

year 2011

Equity Share

BSE NSE

High (Rs.) Low (Rs.) High (Rs.) Low (Rs.)

January 728.75 710.40 728.90 709.10

February 668.00 629.45 671.00 628.15

March 676.00 661.00 675.50 660.35

April 703.00 694.55 703.50 695.00

May 679.80 647.35 681.05 646.70

June 659.50 652.50 658.05 650.55

July 657.00 643.60 657.45 645.00

August 589.40 557.00 591.00 557.25

September 524.90 496.65 526.10 496.35

October 504.50 500.15 524.90 500.00

November 563.10 545.10 564.05 545.55

December 530.85 519.00 530.55 518.80

51. BSE Diagram:

NSE Diagram:

0

100

200

300

400

500

600

700

800

January

February

March

April

May

June

July

August

September

October

November

December

Low (Rs)

High (Rs)

Low (Rs)

0

200

400

600

800

January

February

March

April

May

June

July

August

September

October

November

December

Low (Rs)

High (Rs)

52. Social Responsibility of Company

Excellence at JSPL is not restricted to our business; it

encompasses community partnership and respect for the environment.

JSPL is running co-educational school at Raigarh, Tammar,

nalwa, Angul and Potrata where quality education is being imparted to

over 10,000 students.

O.P.Jindal Globle University, it is a non-profitgloble

University establish by the Haryana Private University Act, 2009

JSPL has a mobile wan and Hakeadeepa health center with

X-ray and lab facility has been operated and about 12,609 person

examined.

54. Conclusion

The company is committed to the application of best

management practices. It is these value and guldens that will

give a firm foundation for future growth of company.

56. Declaration

I, hereby declare that the Project “JindalSteel & Power Limited” is

original to the best of my knowledge and has not been published

elsewhere. This is for the purpose of partial fulfillment of Gujarat

University requirement for the award of the degree of Bachelor of

Business Administration.

Parmar Bhargav G.

Roll No.: 85

Class: SY BBA

Division: B