Download as PDF, PPTX

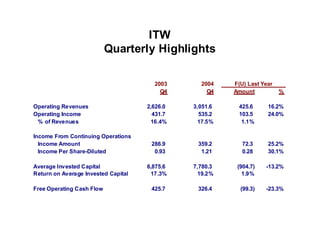

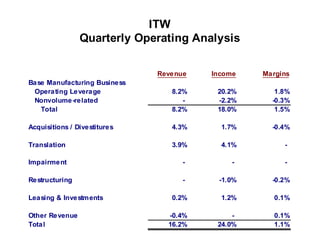

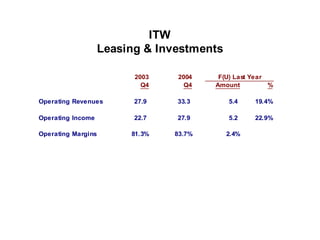

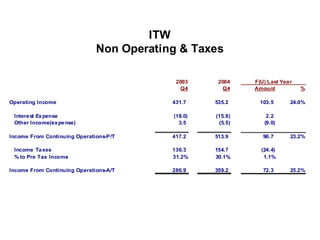

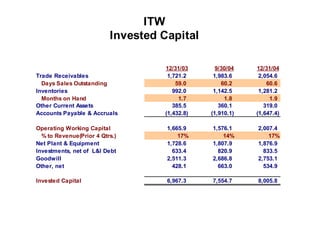

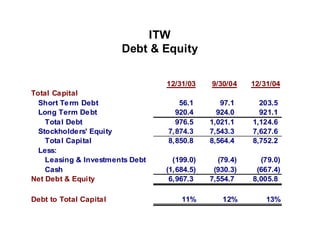

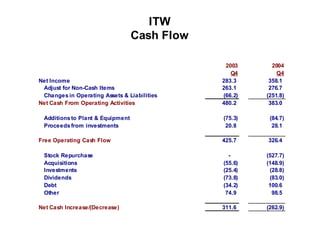

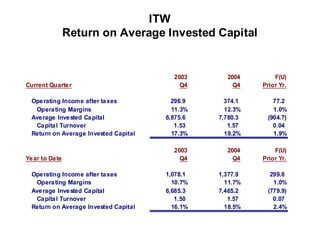

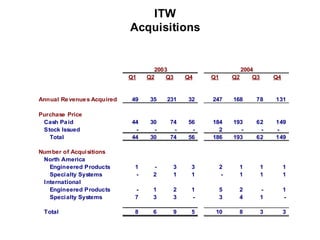

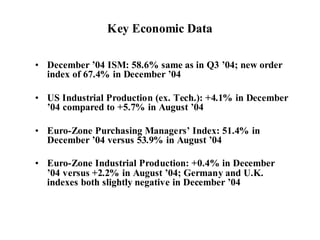

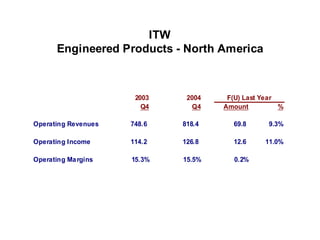

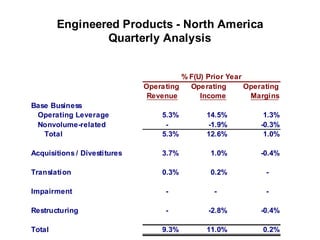

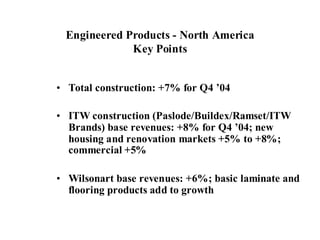

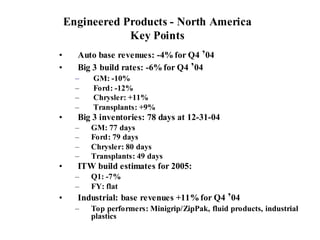

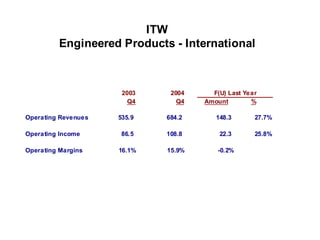

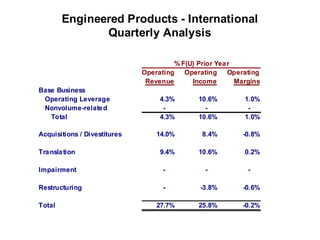

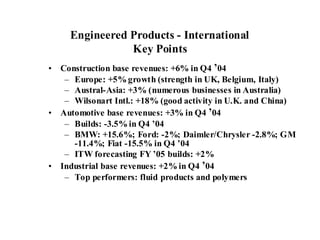

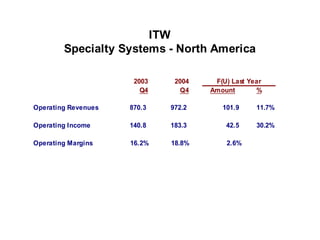

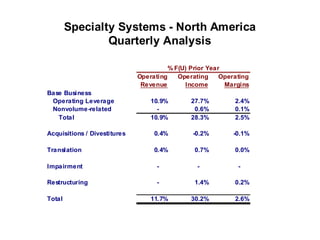

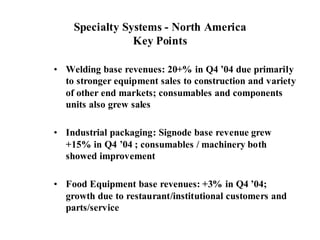

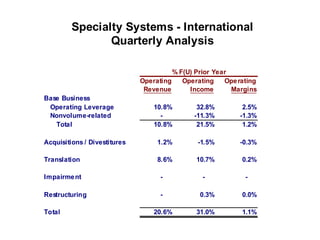

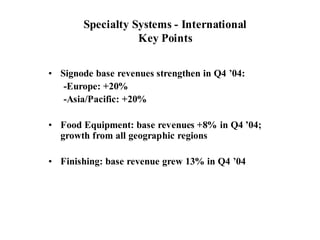

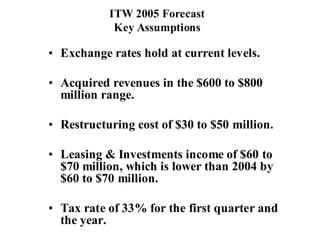

This document summarizes ITW's fourth quarter 2004 conference call. It includes an agenda for the call, forward-looking statements, highlights and analysis of financial results, segment results for engineered products in North America and internationally, and key economic data. John Brooklier and Jon Kinney will provide introductions, a financial overview, and forecast for 2005. They will also take questions from attendees.

![Awareness of digital currency[1] (1).pptx](https://cdn.slidesharecdn.com/ss_thumbnails/awarenessofdigitalcurrency11-260125155504-b1badee4-thumbnail.jpg?width=640&height=640&fit=bounds)