Download to read offline

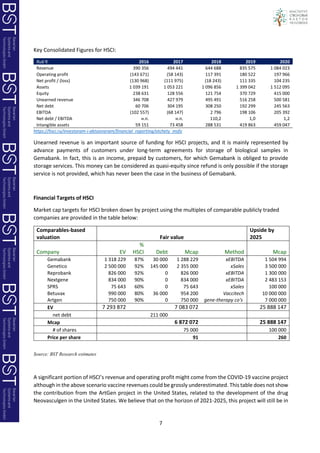

This document provides an investment analysis of Human Stem Cells Institute (HSCI) Group, a diversified healthcare business in Russia. It discusses HSCI's various business segments including stem cell banking, genetic testing, and novel gene therapies. Key points include: HSCI is developing a COVID-19 vaccine and expanding into new areas like gene therapy in the US; the analyst gives revenue and growth forecasts for HSCI's segments and initiatives; and they view HSCI as undervalued given its past growth and potential in large emerging healthcare markets.