- An investor education initiative by Birla Sun Life Mutual Fund provides information about managing money better with mutual funds.

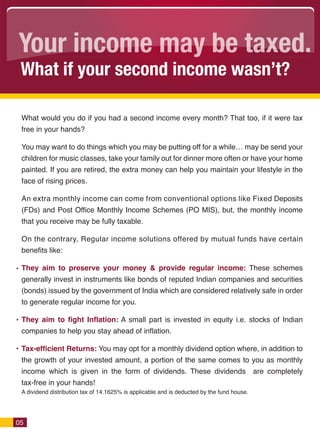

- It discusses how investing in mutual fund savings solutions can help preserve capital, provide liquidity, and earn tax-efficient returns.

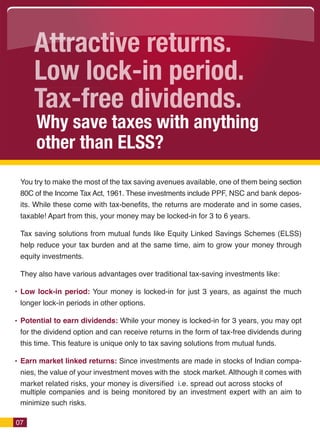

- Various savings solutions are available depending on the time period of investment, ranging from 1 day to 3 months up to 1 year or more.

![manan presentation [Autosaved]x](https://cdn.slidesharecdn.com/ss_thumbnails/13030099-120522101534-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)